Accounting Standards on ‘Financial instruments’ – ASs 30 and 31 respectively on Recognition and Measurement; and on Presentation remained recommendatory till date without being made effective for umpteen number of reasons, known and unknown and hence, remaining nearly dormant, subsisting on various Notifications and ICAI Guidelines including the one very recently issued on Derivatives in 2015 that is now binding for entities not coming under Ind.AS.

But, companies coming under Ind. ASs have to go to go through the full impact of the Standards on financial instruments on the financial results when once the Indian industries prescribed have perforce to go through and as a result, are very wary about. Therefore, it is high time that it was deliberated before the actual dawned.

Ind. AS 32, ‘Financial Instruments on Presentation that deals with financial instruments as financial liabilities or equity and prescribes requirements for offset of financial assets and liabilities in Balance Sheet, Ind.AS 107, ‘Financial Instruments on Disclosure’,and Ind. AS 109, ‘Financial Instruments’ on Recognition and Measurement, are the trinitiesthat deal with Classification, recognition and measurement principles and major disclosure requirements for financial instruments. In addition to the above three Standards, Ind. AS.113 has a say on ’Fair value measurement’ as well related disclosures.

The objective of the standards is to addressall aspects of accounting of financial instruments including debt from equity, netting, and recognition and de-recognition; measurement, hedge accounting and disclosures. Besides, the standards cover all kinds offinancial instruments- receivables, payables, investments in bonds and shares, borrowings and derivatives. Further, they also apply to certain contracts to buy or sell non-financial assets (such as commodities) that can be net-settled in cash or another financial instrument.

Since the ‘contents’ of the about said Ind. ASs are too voluminous to be transacted in an 'article like container’, this article mainly dwellson classification and measurement of the various financial instruments.

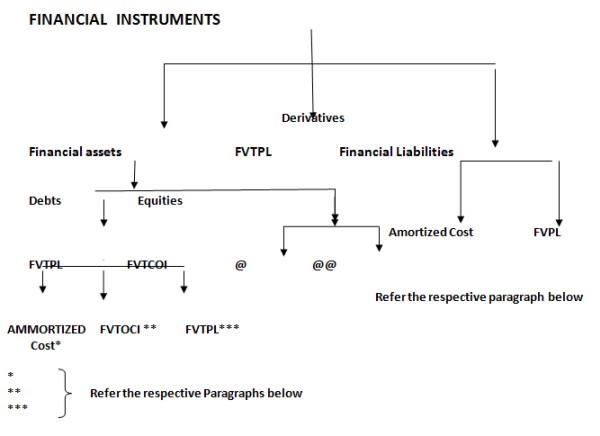

Classification and measurement of financial instruments- Assets:

Financial assets are classified into three categories as detailed hereunder:

* Amotised cost.

* Fair value through Profit and loss (FNTPL)

* Fair value through Other Comprehensive Income (FVTOCI)

Amortised cost is valid and related to Debt Instruments. But, FVTPL and FVTOCI can be deployed both for Debt and Equity Instruments as detailed hereunder.

All financial assets and liabilities are measured initially at fair value under Ind.AS 109 except where the original transaction price is not indicative of fair value of a financial instrument evidenced by a quoted price in an active market for an identical asset or liability (that is, a Level 1 input) or based on a valuation technique that uses only data from observable markets. The difference, gain or loss is recognized in the profit and loss.

The initial classification more or less determines how the instruments are subsequently measured. As focused in the chart underneath, the financial assets are mainly classified as Debt, Equity and derivative Instruments. Equity instruments are the ones that meet the definition of ‘equity’ from the issuers’ perspective under Ind. AS.32 except where it is classified as ‘equity’ using the exception rules in the Ind.AS.32. Other than equities and derivatives is Debt.

Business Model of Classification and measurement of financial Assets -Debt and equity:

|

Sr. No |

Business Model |

Measured at |

How Presented |

|

1 * |

Financialassets held:

|

Initially at fair value & subsequently at Amortised Cost (4.1.2) |

Through Effective Interest Rate(EIR) Ammortised cost is the amount at which the carrying amount is measured after reckoning principal payments plus or minus cumulative amortization. EIR takes care of bonds purchased or issued at discount/ at premium; the applicable rate of interest as compared to market rate, bonds with equity eligibility etc. |

|

2 ** |

To achieve by both collecting contractual cash flows and selling financial assets and (b) the contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding |

Initially &subsequently at fair value through other comprehensive income (FVTOCI (4.1.2A). |

Financial assets included within the FVTOCI category are initially recognized and subsequently measured at fair value. Movements in the carrying amount are recorded through OCI, except for the recognition of impairment gains or losses, interest revenue as well as foreign exchange gains and losses which are recognized in profit and loss. Where the financial asset is derecognized, the cumulative gain or loss previously recognized in OCI is reclassified from equity to profit or loss. |

|

3 *** |

unless it is measured at amortized cost in accordancewith paragraph 4.1.2 or at fair value throughother comprehensive income in accordance with paragraph 4.1.2A. To that extent, it is a residual category in the sense they do not meet the criteria of FVTOCIor amortized cost. |

at fair value through profit or loss(FVTPL) (4.1.4) |

However, an entity may make an irrevocable election at initial recognition for particular investments in equity instruments that would otherwise be measured at fair value through profit or loss to present subsequent changes in fair value in other comprehensive income see paragraphs 5.7.5–5.7.6 |

Business Model and valuation of Equityinvestments:

Investments in equity instruments are always measured at fair value.

As has been spelt out earlier, equity instruments are those that meet the definition of equity from the perspective of the issuer as defined in Ind. AS 32.

@Equity instruments that are held for trading are necessarily required to be classified as FVTPL.

@@For all other equities, management has an option to make an irrevocable election on initial recognition, on an instrument-by-instrument basis, to present changes in fair value in OCI rather than profit or loss. Therefore, it is not accounting policy. If this election is made, all fair value changes, excluding dividends that are a return on investment, will be included in OCI. There is no recycling of amounts from OCI to profit and loss (for example, on sale of an equity investment), nor are there any impairment requirements.However, the entity might transfer the cumulative gain or loss within equity.

Difference between Debt and Equity Instruments Vis-a Vis FVTOCI:

|

Sr.No. |

Differences |

Debt Instruments |

Equity Instruments |

|

1 |

Whether Amortised cost applicable. |

Applicable-refer the earlier chart-on SPPI condition |

Not applicable |

|

2 |

Whether FVTOCI –compulsory or optional |

FVTOCI is compulsory where amortization is not possible (Refer **). ‘FVTPL’- is optional in limited circumstances |

FVTOCI is optional for instruments, that are not held for trading(refer ***) |

|

3 |

Interest income, Impairment/foreign exchange -gain/loss |

Recognized in profit/loss |

Only dividend income in profit and loss; the rest directly in OCI |

|

4 |

IF Financial asset is derecognized |

The cumulative gain or loss previously recognized in OCI is reclassified from equity to profit or loss. |

There is no recycling of amounts from OCI to profit and loss (for example, on sale of an equity investment), nor are there any impairment requirements. However, the entity might transfer the cumulative gain or loss within equity. |

Classification and measurement of financial instruments-Financial Liabilities:

Unlike Financial Assets, Financial liabilities are classified either as at amortised cost or at FVTPL.

Financial liabilities are classified as AT FVTPL, whence,

- they meet the definition of held-for trading,

- they are designated so at initial recognition

- It eliminates or reduces significantly measurement or a recognition inconsistency- popularly known as- Accounting Mismatch.

- a financial liability contains one or more embedded derivatives

- is managed and evaluated on a fair value basis with documented management or investment strategy and information is internally provided to the management personnel as spelt out in Ind. AS-24 on Related Party Disclosures

However, in respect of liabilities designated at FVPL, changes in fair value linked to changes in own credit risk is shown separately in OCI. Amounts in OCI relating to own credit are not recycled to profit or loss even when the liability is derecognized and the amounts are realized. However, the standard does allow transfers within equity.

How to deal with Transaction Cost?

Transaction cost is incremental either directly attributable to acquisition or issue or disposable financial assets/liabilities. The said incremental costs would not have been incurred but for the acquisition or issue or disposable financial assets/liabilities. Transaction costs inter aliaincudes commission paid to agents, advisors, brokers and dealers, levies by regulatory authorities and regulatory agencies and transfer duties and taxes. Debt premium/discounts, finance costs, internal administrative costs and holding costs are not transaction costs.

|

Sr.No. |

Instrument model |

How measured and reflected |

|

1 |

Debt Instruments subsequently measured at amortised cost or FVTOCI |

Included in EIR- amortised in effect through P/L |

|

2 |

In Equity instruments -FVTOCI |

Not reclassified to P/L but continue to be in equity- may reclassify from one equity to the other, when investment is derecognized. |

|

3 |

Financial in instruments at FVTPL |

Immediately recognized in P/L |

Derivatives:

Derivatives (including separated embedded derivatives) are measured at fair value. All fair value gains and losses are recognised in profit or loss except where the derivatives qualify as hedging instruments in cash flow hedges or net investment hedges.

The characteristic of derivatives

- value changes as to the change in value of specified underlying assets,

- requires no small or initial net investment,

- settled at future date,

- embeddedones as detailed hereunder:

1. Hybrid contract is one that cotains both derivative and non- derivative (host contract) and where it is not possible to transfer independent of host cotract.

2. Separate host contract from derivative is one

- Where economic characteristic and risks of the embeddeded derivative are not interlinked

- A separe instument with the terms of the embeded deivatives meet the definition of derivative

- The combined instrument is not designated at FVTPL

3. Designate Hybrid as FVTPL whnce

- Unable to measure the embedded deivative separately either at ehe acquestion date or subsequntly

- Does not modify the cashflows significantly

- Notpermitted to separate the derivative from the host contracts

Ind. AS 109 specifically prohibits bifurcation of embedded derivatives for financial assets. Embedded derivatives in relation to financial liabilities, that are not ‘closely related’ to the rest of the contract, are separated and accounted for as stand-alone derivatives (that is, measured at fair value). An embedded derivative is not ‘closely related’ if its economic characteristics and risks are different from those of the rest of the contract. Ind. AS 109 sets out many examples to help determine when this test is (and is not) met.

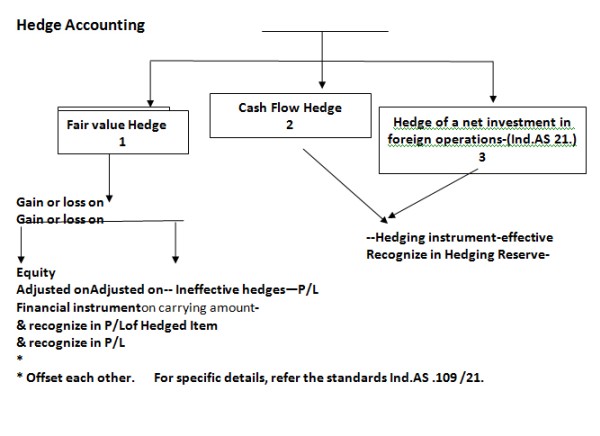

Hedging:

Hedging is a risk management activity usually and usfully resoted to by the entiies to tide over by alleviating all or some of the risk of a hedged item. Hedge accounting changes the timing of recognition of gains and losses on either the hedged item or the hedging instrument so that both are recognised in profit or loss within the same accounting period, in order to record the economic substance of the combination of the hedged item and instrument.

Hedge relationship qualifies for hedge accounting if and only if

- There is a documented policy as to designation of relationship and risk management

- Hedge is highly effective

- Effectiveness is reliably measured

- There is ongoing assessment of effectiveness throughout the reporting period

- For cashflow hedge, forecost transactions highly probable

Ind. AS 109 prohibits voluntary de-designation of hedges if risk management strategy of the company has not changed.

Reclassification of financial assets:

- Required when business model is changed for managing financial assets

- Not proper to reclassify financial assets initially classified as FVTPL.

- To be infrequent--to be determined by the companies higher level management-- when the entity ceases to perform operations that are significant.

- Normal changes do not warrant reclassifications-like temporary disappearance of particular market…

Recognition and Derecognition of Financial Assets and Liablities:

Recognition of both financial assets and liabilities is handled earlier at respective places.

Financial assets are derecognised on expiration of cotractual rights to receive cash flows from the respective financial assets. Again, on an unconditional transfer of the financial assets to an unconsolidated third party, with no risks and rewards of the assets being retained, the respective assets are derecognised

Accounting on derecognition:If the assets are derecognised entirly, the difference between the carrying amount of the respective assets and consideration received plus gain or loss recognised in equity should be recognised in profit and loss., the proportionate difference recognised in profit and loss and the rest in respective accounts.

Financial liabilities are derecognised when cotactual oblications are either discharged or cancelled or expired.

Accounting on derecogntion of liablity: The difference between the carrying amount and consideration paidplus any non cash asset transferred or liability taken over is to be recognised in profit and loss

Impairment to Financial Instruments:

Under Ind. AS 109, Impairment obligations/recognition is based on Expected Credit Loss (ECL) model. Provision based on incurred loss is a fait–accompliand therefore, it is better to visualize the credit loss much earlier than actually trapped /incurred through a well-designed mechanismthat is ECL. All Financial instruments that are not measured by FVTPL and FVTOCI model may come under the clutch of ECL model. In precise, Debtfinancial instruments coming under the grasp of amortised cost will have to go through ECL process to ascertain the impairment provisions.

There are three steps/phases to apply the ECL model.

First Phase/Step---nick namedGeneral Phase: An entity shall find out whether there has been a considerable increase in credit risk since initial recognition. If not significant increase in credit risk, 12 month ECL is used to provide for impairment. If credit risk has increased significantly, life time ECL is used. If in the coming period, credit quality improves to the extent there is no longer significant increase in credit risk, impairment loss may be provided based on 12 month ECL.

The second Phase/Step---nick named as simplifiedphase:one that does not require an entity to track changes in credit risk, but recognizes impairment loss based on life time ECLs at each reporting date. This approach is mandatory for trade receivables or contact receivables coming under the scope of Ind.AS 115, if they don’t contain a significant finance component or when the entity applies practical expedient to ignore separation of tome value of money. Besides, the entity can make accounting policy choice as to trade receivables/contract assets- maybe applied separately for trade receivable and contract assets. Similarly, policy choice separately for operating and finance leases under Ind. AS 17, though not made on individual lease basis.

The third Phase/ Step relates to financial assets that are credit impaired on purchase / origination,known as Purchased or originated credit –Impaired (POCI) financial assets approach.

Conclusion:

As has been spelt out earlier, it would be difficult to deal with all financial instruments dealt with in various Ind. ASs such as 32/107/109 apart from 113 mentioned at the start of the article. They are recognized and measured according to Ind. AS 109’s requirements that are dealt with earlier copiously. But, disclosure requirements that are to be mainly in accordance with Ind. AS 107, and for fair value disclosures under Ind. AS 113, apart from the call from other specific requirements from other standard on instruments.

Ind. AS 32 merits a separate article for the mere size and importance of the standard for simple reason that it lays down the basic principles for classification of liability and equity, apart from dealing with compound Instruments. It speaks unequivocally that a financial instrument should be classified by the issuer upon initial recognition as financial liability or equity according to the substance of the contractual arrangement rather than its legal form and their definitions as such. For example, Preference shares may show the character of liability and equity. Such instruments are component instruments. How to separate is the logical question?

i. Fair value of the liability component is first ascertained that is the initial carrying amount of liability component.

ii. Secondly, the fair value of equity instrument is ascertained by deducting fair value of the liability component from the fair value of the Instrument as whole.

Ind. AS 32 includes presentation requirements and rules for liability, equity, compound financial instruments and offsetting financial asset and financial liability.

A separate article may follow suit on Ind. AS. Let us see how for it will clear the horizon.

CAclubindia

CAclubindia