FAQs: E-Filing Audit Report Replied By CA Sudhir Halakhandi

After writing few articles of the intricacies of the E-filing of Tax audit report we are receiving regular queries from various fellow professionals, out of which we have selected some of the common questions which are being answered here for the benefit of other readers and fellow professions.

Q.1:- Why we have to E-file the Balance sheet and profit and loss account. Is there any circular or notification in this respect out of which the requirement of E-filing the Balance sheet and profit and loss account has emerged.

CA SUDHIR HALAKHANDI:-

The requirement to E- file the audit report u/s 44AB is mentioned in the proviso of Rule 12(2) of the Income tax rules 1962 and if we take the case of Form 3CB or 3CA (the tax audit report u/s 44AB ) , the Form 3CB or the Form 3CA itself mentioned in its body that Profit and loss account and Balance sheet are attached with it hence there is no requirement to issue separate notification, rule or circular to make it mandatory to e-file the Balance sheet and profit and loss account. Let us see the exact language in Form 3CB:-

FORM NO. 3CB

AUDIT REPORT UNDER SECTION 44AB OF THE INCOME TAX ACT, 1961 IN THE CASE OF PERSON REFFERED TO IN CLAUSE (b) OF SUB-RULE (1) OF RULE 6G

We have examined the BALANCE SHEET AS AT 31st MARCH 2013 and the PROFIT AND LOSS ACCOUNT for the year ended on that date, attached herewith of _____________________.

Q.2:- Is it sufficient to furnish the unsigned PDF copy of the profit and loss account and Balance sheet or the scan copy of the same duly signed by the CA and assessee is required?

CA SUDHIR HALAKHANDI:

This is very common question and it has been asked by so many professionals.

In my opinion the profit and loss account and Balance sheet should be filed duly signed by the assessee and CA i.e. the singed (both by assessee and CA) Balance sheet and profit and loss account is to be scanned and the PDF copy of the same is required to be e-filed. There are reasons of my opinion which are being explained below:

(i). The 3CB/3CD can only be filed after completion of audit and in that case the Balance sheet and profit and loss account are also signed by the assessee and CA so at that time these is no existence of unsigned Balance sheet and profit and loss account. So here Balance sheet and profit and loss account means audited Balance sheet and profit and loss account and audited profit and loss account and Balance sheet can only be construed as “Singed Profit and Loss account and Balance sheet” both by CA and assessee. You have to file the signed audited Balance sheet.

(ii). The second reason is based on the fact that in most of the cases the assessee is not “practically” aware about the existence and importance of the Digital signatures and E-filing of ITR and these are handled by the CAs and even the audit reports are approved by the CAs on behalf of the assessee with the digital signatures of the assessee though in that case they are working in capacity other than auditor(Tax consultant or Tax advisor) of the assessee . So if you took the physical signatures of the assessee on the Balance sheet and profit and loss account before finally uploading it, it will be a safer practice.

Q.3:- Is it possible to file the ITR first and then e-file the audit report? What should be the exact sequence of the actions in this respect?

CA SUDHIR HALAKHANDI: -

Here see the information required to be filled the ITR and there is a column in the ITR which requires the “date of furnishing the audit report”. Hence first you have to E-file the audit report and then it has to be approved by the assessee and ITR can be filed by the assessee thereafter. This should be the exact sequence.

Q.4:- What should be treated the date of Furnishing of audit report? Is it the date on which the Tax audit report is e-filed by the CA or the date on which the audit report is approved by the assessee? What is the difference between the date of report of the audit (which is also a separate requirement of the ITR) and date of furnishing of audit report?

CA SUDHIR HALAKHANDI:-

First take the “date of report of audit” and it means the date which is mentioned on the face of the audit report i.e. the date on which the audit report is signed by the CA and there is should be confusion about the date of report of audit.

There may be some confusion about the date of “furnishing of audit report”. There may be a opinion that date of E-filing of audit report should be the date of submission of audit report and second opinion is that the process of E-filing of audit report is completed when it is approved by the assessee so the date of approval of audit report by the assessee should be taken as the date of furnishing of the audit report.

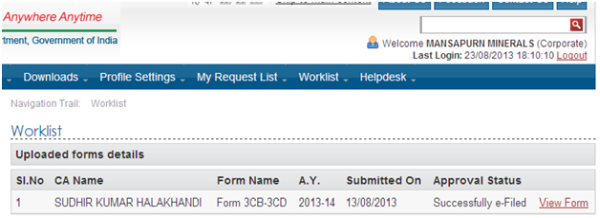

Now see, the fact is that the audit report is E-filed on a particular date and the subsequent event or date of its approval will not change “this fact” hence if the audit report is “approved” then the date of E-filing of audit report should be the date of “furnishing of audit report”. Let us try to verify this fact from one of our case:-

The audit report of one of our client was uploaded on 13/08/2013 and it was approved on 23/08/2013 and in the work list of the assessee after approval of the audit report the date of submission is mentioned as 13/08/2013.

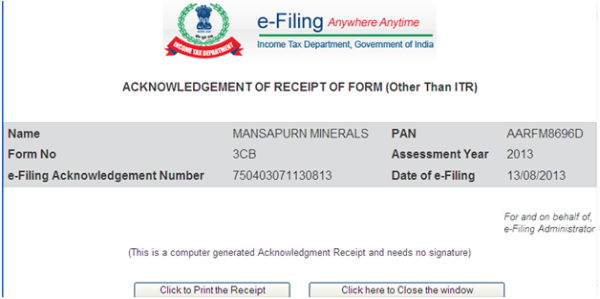

Further in the Account of CA the date of filing for the same assessee is mentioned as 13/08/2011 though the assessee has approved the audit report on 23/08/2013.

Q.5:- We have e-filed the audit report and also filed the ITR but up to that moment the audit report is not approved by the assessee. What will be the consequences of this mistake and what should be done from our side to rectify this mistake?

CA SUDHIR HALAKHANDI:-

Is it practically possible to E-file the ITR even before the approval of the audit report by the assessee? Yes and we have experienced it so it is also a shortcoming of the system since in that case the E-filing system should have given the “error signal” and in our case we E-filed the audit report and by mistake also filed the ITR on behalf of the assessee even before the approval of the audit report and it was accepted without showing any “error message” but when mistake was noticed by us we approved the audit report on behalf of the assessee .

Q.6:- How can we take the printing of Form 3CB/3CD because the utility does not provide the facility of printing the form. We have been suggested to take the print from the account of the assessee in his work list but there is a problem about his password because we are not filing the ITR on behalf of the assessee and he is taking services of some other professionals in this respect.

CA SUDHIR HALAKHANDI:-

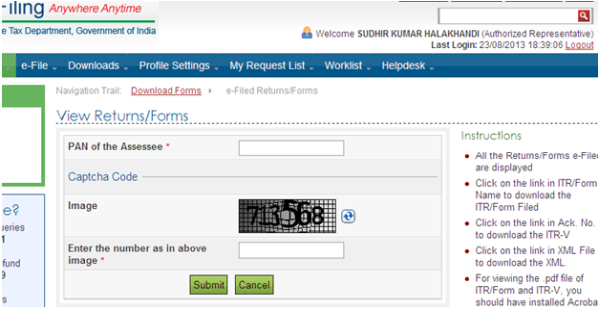

There is no need to have pass word of the assessee to get the uploaded Form 3CB/3CD because these are also available in the account of the CA also and for this purpose you need the PAN and DOB of the assessee. For this purpose you have to Login in As CA, then go to My Account→ view Forms and you will get the following screen, fill the required details and you will the required Forms in printable format.

Since at the time of opening of the Form 3CD/3CB , the PAN and DOB of the assessee will be required and by filling these two you can open and print the forms. So there is no need to have the Pass word of the assessee to take the printout of the Form 3CD/3CB.

Q.7:- We are not able to keep track of E-mails daily but wants to know how many assessees have added us as CA. Is it possible to see it at a glance?

CA SUDHIR HALAKHANDI:-

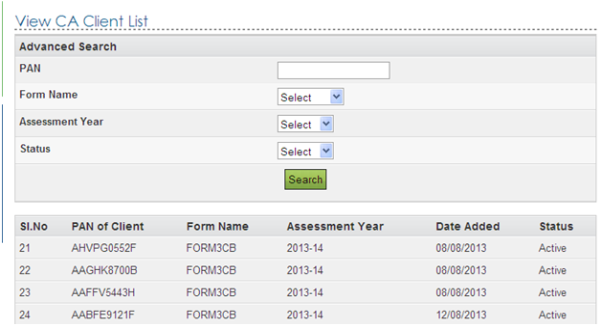

Yes you can see it in your account. Go to My Account→ view client List and then you will get the List . Please see it as under:-

Q.8:- What is the expectation and possibility of extension of date for completion of Tax audit this year considering the circumstances in which the CAs are facing difficulties in completing the task within time.

CA SUDHIR HALAKHANDI:-

Yes it is a new task for the CAs and further since the ITRs were also introduced very late and still the utility to E-file is not free from the mistakes hence it is natural for chartered accountants to have difficulties in completing this new task hence the date of completion of audit should be extended by at least 2 Months but the declaration in this respect should be made immediately instead of waiting for the last day.

(The answers of these queries are given by CA SUHDHIR HALAKHANDI with the technical assistance of CA ABHAS HALAKHANDI)

CA SUDHIR HALAKHANDI

CA ABHAS HALAKHANDI

“HALAKHANDI”

LAXMI MARKET

BEAWAR-305901(RAJ)

MAIL: sudhirhalakhandi@gmail.com and sudhir@halakhandi.com

Visit us:- www.halakhandi.com

CAclubindia

CAclubindia