Debit Notes in GST is an altogether different concept from the earlier practices. Under the GST Law, the debit note or a supplementary invoice is a convenient and legal method by which the value of the goods or services in the original tax invoice can be enhanced.

Background

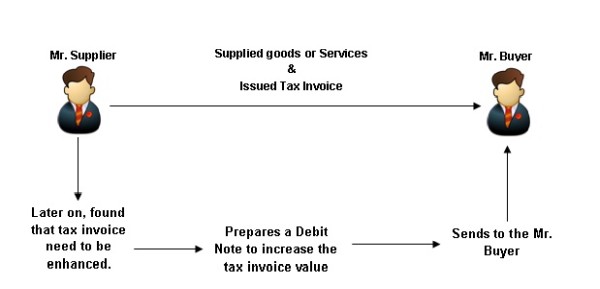

As per GST Law, a supplier of goods or services or both is mandatorily required to issue a tax invoice. Sometimes, there could be situations where the supplier want to increase or to make addition in the tax invoice by the following reasons:

a) The Supplier has declared value which is less

than the actual value of the goods or services or both provided.

b) The Supplier has declared a lower tax rate than what is applicable for the

kind of the goods or services or both supplied.

c) The quantity received by the recipient (buyer) is more than what has been

declared in the tax invoice.

d) Any other similar reasons.

In order to cover these kinds of situations the supplier is allowed to issue a Debit Note to the recipient (buyer). The debit note also includes supplementary invoice.

Note: When the movement of goods is involved, the debit note could not be issued. i.e. The debit note can not be taken as a mean of purchase returns.

Format

There is no prescribed format but debit note issued by a supplier must contain the following particulars, namely:

1. name, address and Goods and Services Tax Identification Number of the supplier;

2. nature of the document;

3. a consecutive serial number not exceeding sixteen characters, in one or multiple series, containing alphabets or numerals or special characters hyphen or dash and slash symbolised as “-” and “/” respectively, and any combination thereof, unique for a financial year;

4. date of issue;

5. name, address and Goods and Services Tax Identification Number or Unique Identity Number, if registered, of the recipient;

6. name and address of the recipient and the address of delivery, along with the name of State and its code, if such recipient is un-registered;

7. serial number and date of the corresponding tax invoice or, as the case may be, bill of supply;

8. value of taxable supply of goods or services, rate of tax and the amount of the tax debited to the recipient; and

9. signature or digital signature of the supplier or his authorized representative.

Tax Liability

When the supplier issues debit note or a supplementary invoice, it creates additional tax liability. The treatment of a debit note or a supplementary invoice would be identical to the treatment of a tax invoice as far as returns and payment are concerned.

DISCLAIMER: The views expressed in this article are strictly of the author. The contents of this article are solely for informational purpose. It does not constitute professional advice or recommendation by the author. The author does not accept any liabilities for any loss or damage of any kind arising out of any information in this article nor for any actions taken in reliance thereon.

The author can also be reached at cavrjsharma@gmail.com

CAclubindia

CAclubindia