Introduction

Investing and financing of funds are two crucial functions of finance manager. The investment of funds requires a number of decisions to be taken in a situation in which funds are invested and benefits are expected over a long period. The finance manager of concern has to decide about the asset composition of the firm. The assets of the firm are broadly classified into two categories viz., fixed and current. The aspect of taking the financial decision with regard to fixed assets is known as capital budgeting.

Ideally, businesses should pursue all projects and opportunities that enhance shareholder value. However, because the amount of capital available at any given time for new projects is limited, management needs to use capital budgeting techniques to determine which projects will yield the most return over an applicable period of time.

The capital budgeting decision may be thought of as a cost-benefit analysis. Am asking a very simple question: "If we purchase the fixed asset, will the benefits to the company be greater than the cost of the asset?" In essence, we are placing the cash inflows and outflows on a scale to see which is greater.

Capital budgeting decisions (CBD)

Capital budgeting (or investment appraisal) is the planning process used to determine whether an organization's long term investments such as new machinery, replacement machinery, new plants, new products, and research development projects are worth the funding of cash through the firm's capitalization structure (debt, equity or retained earnings).

It is the process of allocating resources for major capital, or investment, expenditures. One of the primary goals of capital budgeting investments is to increase the value of the firm to the shareholders.

In other words, the process of planning expenditure on assets whose cash flows are expected to extend beyond the period of one year is referred as capital budgeting.

A complicating factor is that the inflows and outflows may not be comparable: cash outflows (costs) are typically concentrated at the time of the purchase, while cash inflows (benefits) may be spread over many years. The time value of money principle states that dollars today are not the same as dollars in the future (because we would all prefer possessing dollars today to receiving the same amount of dollars in the future). Therefore, before we can place the costs and benefits on the scale, we must make sure that they are comparable. We do this by taking the present value of each, which restates all of the cash flows into "today's dollars." Once all of the cash flows are on a comparable basis, they may be placed onto the scale to see if the benefits exceed the costs.

Under CBD, we make the evaluation of long term projects i.e financial analysis of a long period proposals. Normally, the cash outflows in project/equipment, plant is at the beginning of the project. The project provides cash inflows over its life. The amount invested in project has some cost of capital. Hence the inflows arising at different point of time is converted into its present value and the present value of future inflows is compared with present value of outflows and a decision is taken. Oftentimes, a prospective project's lifetime cash inflows and outflows are assessed in order to determine whether the returns generated meet a sufficient target benchmark.

Therefore, the present value of the cash inflows (benefits) minus the present value of the cash outflows (cost).

NPV = PVB - PVC

|

If the NPV is: |

Benefits vs. Costs |

Should we expect to earn at least |

Accept the |

|

Positive (+ve) |

Benefits > Costs |

Yes, more than |

Accept |

|

Zero (0) |

Benefits = Costs |

Exactly equal to |

Accept |

|

Negative (-ve) |

Benefits < Costs |

No, less than |

Reject |

In any growing concern, capital budgeting is more or less a continuous process and it is carried out by different functional areas of management such as production, marketing, engineering, financial management etc. All the relevant functional departments play a crucial role in the capital budgeting decision process of any organization, yet for the time being, only the financial aspects of capital budgeting decisions are considered.

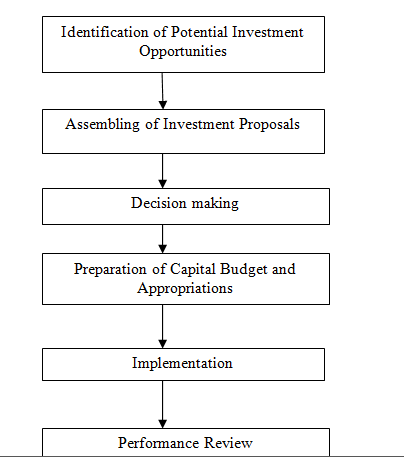

Capital Investment Process

The strategic capital investment process is discussed below :

1. Identification of Potential Investment Opportunities: The first and probably most crucial stage in the process involves the recognition of opportunities. This involves a continuous search for investment opportunities which are compatible with the firm’s objectives.It require imagination and diligence by management if they are to be detected at any early stage. The earlier opportunity is identified the greater should be the potential returns before competitors and imitators react.

· Monitor external environment regularly to scout investment opportunities.

· Formulated the well defined corporate strategy based on a thorough SWOT Analysis.

· Share corporate strategy and perspectives with persons who are involved in the process of capital budgeting.

· Motivate employees to make suggestions.

2. Assembling of Investment proposals: The purpose of routing a proposal through several persons is primarily to ensure that the proposal is viewed from different perspectives and too creates an environment of co-ordination of interrelated activities.

· Screening the Alternatives

· Analysis of Feasible Alternatives

· Evaluation of Alternatives

3. Decision Making: Once evaluation is completed then proposal will be forwarded to a higher level of management for authorisation to take up the project.

4. Preparation of Capital Budget & Appropriations: to ensure that the funds position of the firm is satisfactory at the time of implementation. Further, it provides an opportunity to review the project at the time of implementation.

5. Implementation: Translating an investment proposal into a concrete project is a complex, time-consuming and risk-fraught task. For expeditious implementation at a reasonable cost, the following should be undertaken:

· Adequate formulation of projects

· Use of Principle of Responsibility Accounting

6. Performance Review: its progress is monitored with the aid of feedback reports. These reports will include critical path analysis, capital expenditure, progress reports, performance reports comparing actual performance against plans set and post completion audits.

Click Here to view Rahul Malkan's Class on Financial Reporting

CAclubindia

CAclubindia