What is a small company?

The concept of small companies was introduced by the companies act, 2013 for the first time. According to the Act, some companies are termed as small companies based on their capital and turnover for the purpose of providing certain relief/exemptions to these companies.

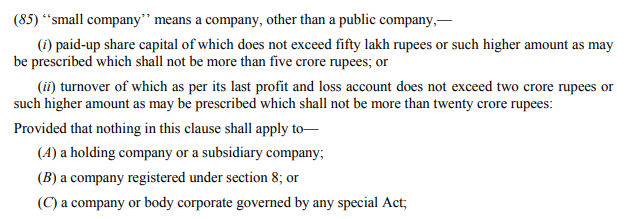

What companies can claim to be a Small Company?

According to the definition given above, the companies which fulfills the following provisions can be featured as the small company:

- Company should be Private Limited

- Paid Up capital should not be more than Rs. 50 Lakh

- Turnovers should not exceed more than Rs. 2 cr

Annual Corporate Compliances:

Below given are some of the certain annual compliances which are required to be followed by companies which fall under the definition of a small company.

Director's Interest:

Every director shall at the first meeting of the Board in which he participates as a director and thereafter at the first meeting in every financial year or whenever there is any change in the disclosures already made, then at the first Board meeting held after such change, disclose his concern or interest in other entities and in the company which shall include the shareholding.

The changes in the director's interest, if any, shall be given in forms MBP-1 in the next board meeting.

Appointment of Directors:

At least one director must be 'Resident in India'. A person who stays more than 180 days in a calendar year India is regarded as a 'Resident'

Appointment of Auditors:

Appointment of an auditor should be made in the BOD meeting within 30 days of Incorporation. Auditor shall be appointed in 1st Annual General Meeting (AGM) i.e. the 'Shareholders Meeting' for 5 years.

The company shall inform the auditor concerned of his or her appointment, and also file a notice of such appointment with the Registrar by filing mandatory form ADT-1 within 15 days of the meeting in which the auditor is appointed.

Annual General Meeting:

The small Company should hold a general meeting (meeting of Shareholders) at the Registered Office each year as AGM.

Notice of Annual General Meeting shall be sent to all the Directors, Members, Auditors, legal representative of any deceased member and the assignee of an insolvent member. Notice shall be sent by hand or by ordinary post or by speed post or by registered post or by courier or by facsimile or by email or by any other electronic means.

Board meetings:

The Board shall hold its first meeting within 30 days of the date of incorporation of the company.

Every Small Company shall hold at least two meetings of the Board of Directors (BOD) in a financial year (April-March). That is to say 1 meeting of BOD in each half of the calendar and the gap between two meetings shall not be less than 90 days.

Directors can participate in BOD in person or through video conferencing or another audiovisual mode which can be recorded.

Audit of Accounts:

The Company shall Coordinate with their auditors to prepare and file the Tax Audit Report on the prescribed due dates.

It's a special & separate report required by the Income Tax Act in case the Annual Turnover exceeds INR 10 Million (USD 150 Thousand).

Filing of Financial Statements:

It would be mandatory to File the audited financial statements with the Registrar of Companies (ROC) together with Form AOC-4 and the consolidated financial statements, if any, with Form AOC-4 CFS.

Moreover, the Company shall send to all the members of the Company, all trustees for the debenture holders and to all persons being the persons so entitled, copy of the (approved) Financial Statements (including consolidated Financial Statements, if any, auditor's report and every other document required by law to be annexed/ attached to the financial statements) at least 21 clear days before the Annual General Meeting. Except in the case where AGM is called on shorter notice pursuant to section 101(1)

Annual Return:

Every Company shall file Its Annual Return within 60 days of holding of AGM or where no AGM is held in any year within 60 days from the date on which the AGM should have been held together with the statement specifying the reasons for not holding the AGM.

With a view to facilitating ease of doing business and for reducing the burden of Small Company, the Central Government has prescribed an abridged form of Annual Return to be annually filed by Small Companies. The Annual Return of every Small Company shall be signed by the company secretary or where there is no company secretary by the director of the company.

Apart from the above-mentioned compliance the company shall also maintain some register which are mandatory namely register of members, register of debenture holders, register of any other security holders, etc.

However, as you strive to grow your Small Company, there is one thing to keep in mind, and i.e. ensuring its compliance. If you fail to do so, you can lose your protections and accrue fees and penalties.

CAclubindia

CAclubindia