1. INTRODUCTION

In terms of Section 66B of the Act, service tax will be leviable on all services provided in the taxable territory by a person to another for a consideration other than the services specified in the negative list. Due to Section 66B, the regime of service tax from taxable 119 services to 17 services under negative list. Meaning thereby that except these 17 Services, all Services will be taxable under Service tax. In all, there are seventeen heads of services that have been specified in the negative list.

2. The scope and ambit of these is explained in paras below

3. Services provided by Government or local authority

Services by Government or a local authority excluding the following services to the extent they are not covered elsewhere-

(i)Services by the Department of Posts by way of speed post, express parcel post, life insurance and agency services provided to a person other than Government;

(ii)Services in relation to an aircraft or a vessel, inside or outside the precincts of a port or an airport;

(iii)Transport of goods or passengers; or

(iv)Support services, other than services covered under clauses (i) to (iii) above, provided to business entities;

Analysis

a)What is the exact meaning of Government or local authority

Government

Government has not been defined in the Finance Act, 1994 or the rules made thereunder. As per clause 23 of section 3 of the General Clauses Act, 1897, Government shall include both the Central Government and any State Government.

It would include various departments and offices of the Central or State Government or the Union Territory Administrations which carry out their functions in the name and by order of the President of India or the Governor of a State.

Local authority

Local authority is defined in clause (31) of section 65B and means the following:-

A Panchayat as referred to in clause (d) of article 243 of the Constitution

A Municipality as referred to in clause (e) of article 243P of the Constitution

A Municipal Committee and a District Board, legally entitled to, or entrusted by the Government with, the control or management of a municipal or local fund

A Cantonment Board as defined in section 3 of the Cantonments Act, 2006

A regional council or a district council constituted under the Sixth Schedule to the Constitution

A development board constituted under article 371 of the Constitution, or

A regional council constituted under article 371A of the Constitution.

b)What are the Services covered in this Rule

(i)Agency or intermediary services on commission basis (distribution of mutual funds, bonds, passport applications, collection of telephone and electricity bills), which are provided by the Department of Posts to non-government entities are liable to service tax because these are Agency services carried out on payment of commission on non-government business.

(ii) As Per clause 49 of Section 65 B "support services" means

infrastructural,

operational,

administrative,

logistic,

marketing or

any other support of any kind comprising functions that entities carry out in ordinary course of operations themselves but may obtain as services by outsourcing from others for any reason whatsoever

and shall include

advertisement and promotion,

construction or works contract,

renting of immovable property,

security,

testing and analysis;

(iii) Sovereign right shall be treated as non-taxable

Thus services which are provided by government in terms of their sovereign right to business entities, and which are not substitutable in any manner by any private entity, are not support services.

Examples

Grant of mining or licensing rights or

Audit of government entities established by a special law, which are required to be audited by CAG under section 18 of the Comptroller and Auditor-Generals (Duties, Powers and Conditions of Service) Act, 1971 (such services are performed by CAG under the statue and cannot be performed by the business entity themselves and thus do not constitute support services.)

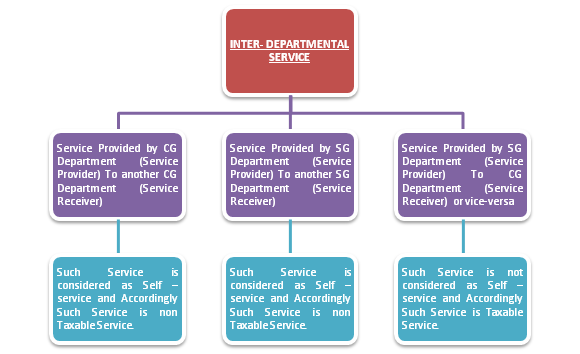

(iv) INTER- DEPARTMENTAL SERVICE

4. Services by the Reserve Bank of India

Analysis

All services provided by the Reserve Bank of India are in the Negative list.

But services provided to the Reserve Bank of India are not in the negative list and would be taxable unless otherwise covered in any other entry in the negative list.

As Per clause 42 of section 65B of finance Act,1994 - "Reserve Bank of India" means the bank established under section 3 of the Reserve Bank of India Act, 1934 (2 of 1934.).

5. Services by a foreign diplomatic mission located in India

Any service that is provided by a diplomatic mission of any country located in India is in the negative list.

This entry does not cover services, if any, provided by any office or establishment of an international organization.

6. Services relating to agriculture or agricultural produce by way of

(i)Agriculture has been defined in the Act as cultivation of plants and rearing or breeding of animals and other species of life forms for foods, fiber, fuel, raw materials or other similar products but does not include rearing of horses. Activities like breeding of fish (pisciculture), rearing of silk worms (sericulture), cultivation of ornamental flowers (floriculture) and horticulture, forestry included in the definition of agriculture.

(ii) Agricultural produce has also been defined in Section 65B of the Act which means any produce of agriculture on which either no processing is done or such processing is done as is usually done by a cultivator or producer which does not alter its essential characteristics but makes it marketable for primary market. It also includes specified processes in the definition like tending, pruning, grading, sorting etc. which may be carried out at the farm or elsewhere as long as they do not alter the essential characteristics. The following activity will be covered under Agriculture produce:-

a)Plantation crops like rubber, tea or coffee.

b)Cleaning of wheat carried out outside the farm, Since this activity do not alter essential character of Wheat

Whereas, the following activity will not qualify as Agriculture Produce

a) Preparation Potato chips or tomato ketchup

b)Operations like shelling of paddy

c)Processes of grinding, sterilizing, extraction packaging in retail packs of agricultural products which make the agricultural products marketable in retail market

CAclubindia

CAclubindia