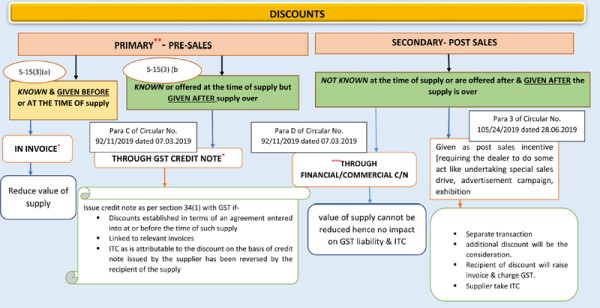

* Supplier shall be entitled to avail the ITC for such inputs, input services and capital goods used in relation to the supply of goods or services or both on such discounts means supplier no need to reverse ITC for reduction in value of outward supply due to discount.

** Discount under "Buy more, save more" scheme and post supply / volume discounts established before or at the time of supply.

*** Not required to reverse ITC though payment (due to discount through financial C/N) not made fully- 2nd proviso to section 16(2)- [Para 5 of Circular No. 105/24/2019]

Refer Circular No. 92/11/2019 dated 07.03.2019 for treatment of sales promotion schemes

A. Free samples and gifts

B. Buy one get one free offer

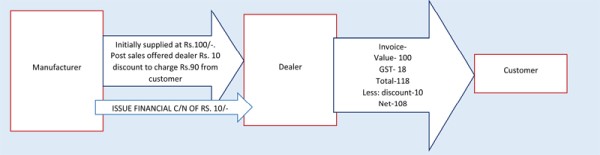

Circular No. 105/24/2019 dated 28.06.2019-

Additional discount given by the supplier of goods to the dealer to offer a special reduced price by the dealer to the customer to augment the sales volume

Additional discount would represent the consideration flowing from the supplier of goods to the dealer for the supply made by dealer to the customer. This additional discount as consideration, payable by any person (supplier of goods in this case) would be liable to be added to the consideration payable by the customer, for the purpose of arriving value of supply, in the hands of the dealer, under section 15 of the CGST Act.

Get circular

CAclubindia

CAclubindia