TIME OF SUPPLY IN CASE OF GOODS:

Forward charge:

Regular Dealers:

Earlier of the following;

- Date of Invoice

- Last date on which invoice is to be issued u/s 31(1)*

Composition Dealers:-

Earlier of the following;

- Date of Invoice

- Last date on which invoice is to be issued u/s 31(1)*

- Receipt of Payment

Receipt of Payment will be the earlier of the following dates:

- Date of entry in Books

- Date of credit in Bank.

Reverse charge:-

Earlier of the following;

- Date of Receipt of goods

- Date of Payment

- Date of Invoice of supplier+31 days.

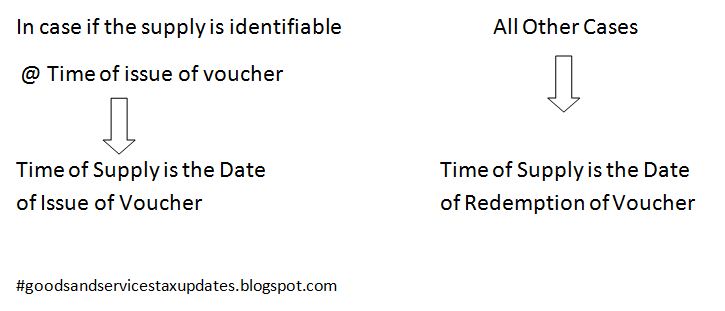

IN CASE OF VOUCHERS:

IN CASE OF INTEREST ON DELAYED PAYMENT:

Time of supply is the date on which supplier receives such addition in value.

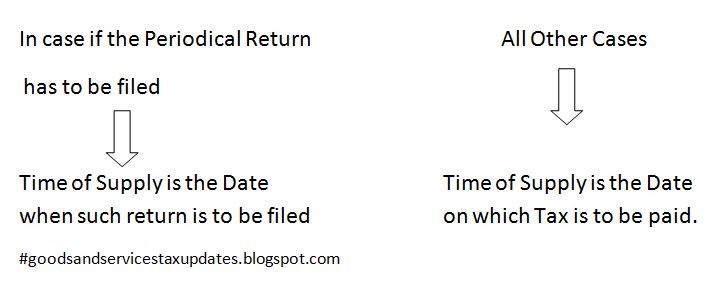

RESIDUAL CLAUSE:

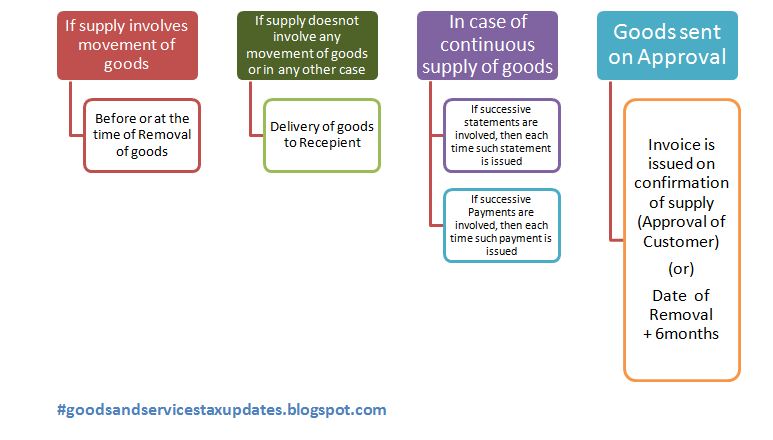

*TIME LIMIT TO ISSUE AN INVOICE U/S 31(1):

IN CASE OF SUPPLY OF SERVICES:

FORWARD CHARGE:

REVERSE CHARGE:

Earlier of the following;

- Date of Payment

- Date of Invoice + 61 days

IN CASE OF SUPPLY BY ASSOCIATED ENTERPRISES:

Service Provider is in Outside India and Service recipient is in India, the Time of supply shall be the date of entry in the books of accounts of the recipient of the supply or the date of payment, whichever is earlier.

IN CASE OF VOUCHERS: (Same as in case of Goods)

IN CASE OF INTEREST ON DELAYED PAYMENT: (Same as in case of Goods)

Time of supply is the date on which supplier receives such addition in value.

RESIDUAL CLAUSE: (Same as in case of Goods)

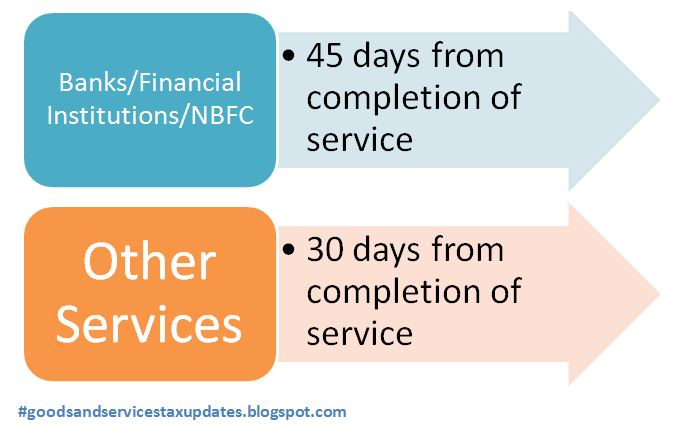

*TIME LIMIT TO ISSUE INVOICE FOR SERVICES U/S 31:

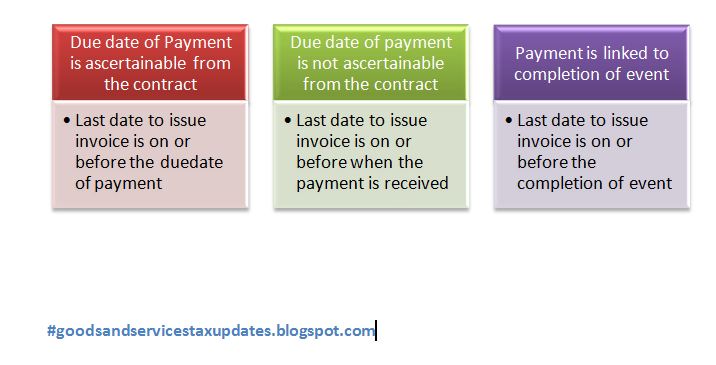

IN CASE OF CONTINUOUS SUPPLY OF SERVICES:

CAclubindia

CAclubindia