Click Here to read the 1st part of the article

Click Here to read the 2nd part of the article

Click Here to read the 3rd part of the article

Click Here to read the 4th part of the article

Amendment 87: Section 135 [Corporate Social Responsibility]

An obligation of spending money on CSR has been introduced now and this provision is applicable to every Company with net worth of >= Rs. 500 crores or a turnover of >= Rs. 1000 crores or more or a net profit of >= Rs. 5 crores during any FY. Such companies are required to set up a CSR Committee of the board consisting of 3 or more directors including at least 1 independent director. This committee shall then recommend CSR policies to the Board.

Amendment 88: Section 135 [Corporate Social Responsibility read with Rule 3(2)]

This rule specifies that each company which ceases to be a company under Section 135(1) for 3 consecutive FYs, is not required to constitute a CSR Committee nor is required to comply with the provisions of Section 135 (2) – (5). This exception is there till a time it meets the criteria of the thresholds prescribed under Section 135(1).

Amendment 89: Section 135 [Corporate Social Responsibility]

The Board of every company is vested with a responsibility to ensure that the company spends in every FY, at least 2% of the average net profits it made during the 3 immediately preceding FYs in pursuance of its CSR Policy. The board in its report shall have to explain reasons in case it fails to spend such an amount.

Amendment 90: Section 135 [Corporate Social Responsibility read with Rule 4(2)]

Companies have been permitted to undertake the CSR activities via a registered trust or registered society or a company established by the company established by the company or its holding/subsidiary/associate company under Section 8 or otherwise. In case such a trust society/company isn’t established by the company its holding/subsidiary/ associate company, it should have a track record of 3 years in undertaking similar kinds of programs or projects.

Amendment 91: Section 135 [Corporate Social Responsibility read with Rule 4(5)]

Projects/ Programs/ Activities undertaken for the sole benefit of the employees of the company & their families shall not be considered as CSR.

Amendment 92: Section 135 [Corporate Social Responsibility read with Rule 4(6)]

In order to build CSR capacities of their own personnel as well as of their implementing agencies companies can spend up to 5% of total CSR expense of the company in one FY.

Amendment 93: Section 135 [Corporate Social Responsibility read with Rule 8(1)]

The Board report of a company as per the provisions of Section 135 along with the rules thereto shall now include an annual report on CSR as well.

Amendment 94: Section 211 [Establishment of Serious Fraud Investigation Office (SFIO)]

Due to the increase in number of Fraudulent Activities in Corporates, the term Fraud has been now defined and declared as a Non-cognizable Offence. Big frauds and scams in companies shall be investigated by a Serious Fraud Investigation Office (SFIO). This office has been given wide range of statutory powers for conducting search/seizure/arrests etc.

Amendment 95: Section 380 (Documents etc. to be delivered to Registrar by Foreign Companies read with Rule No. 3)

The orbit of functioning of the Foreign Companies has been increased. All the foreign companies which carry business via Electronic means shall now deemed to have a place of business in India and shall have to register in India within 30 days of establishment of a place of business in India.

Amendment 96: Section 2(60) (Definitions)

The term “Officer in Default” has now been broadened and is inclusive of CFO, Share Transfer Agents, Registrars and Merchant Bankers to the issue or transfer of shares. All such directors who are well aware of the default by way of participation in Board Meeting or even by receiving minutes without raising any objection will also be included in this category in spite of Company having a MD/WTD/ Other KMP.

Amendment 97: Section 123 (Declaration of Dividend)

A company is now prohibited to declare interim dividend at a rate which is > average dividends declared by it during the immediately preceding 3 FYs in case it has incurred any loss during the current FY up to the end of the quarter immediately preceding the date of declaration of interim dividend.

Amendment 98: Section 455 (Dormant Company)

In case a company is formed & registered under this Act for giving effect to a future project or to hold an asset or intellectual property and it has no significant accounting transaction, such a company or an in activity shall have an option of making an application to the Registrar for obtaining the status of a Dormant Company. Some of the prescribed criteria are enumerated below:-

• No inspection/inquiry/Inspection has been ordered or taken up or carried out against the company.

• No prosecution under any law has been initiated and pending against the company.

• The company is neither having any outstanding public deposits nor is the company a defaulter in payment thereof or interest thereon.

• The company is not having any outstanding loan (both secured and unsecured).

• There is no dispute in the management/ownership of the company & there is a certificate in this regard in the prescribed form.

• The company doesn’t have any outstanding liability towards Statutory Taxes, Duties etc. which are payable to the Central Government or any State Government/ Local Authorities.

Amendment 99: Section 455 (Dormant Company read with Rule No. 6)

Dormant Companies have been exempted from complying with various provisions of this Act and are required to file only a “Return of Dormant Company” annually which shall indicate the financial position of the company duly signed by practicing CA along with filing return of allotment & change in directors. The provisions related to rotation of Directors are also not applicable to Dormant Companies.

Amendment 100: Section 464 (Prohibition of association or partnership of persons exceeding certain number read with Rule No. 10)

The New Act has given a flexibility by raising the bar on number of partners/ members for a partnership firm/ association of persons made with a profit motive from 20 to 50.

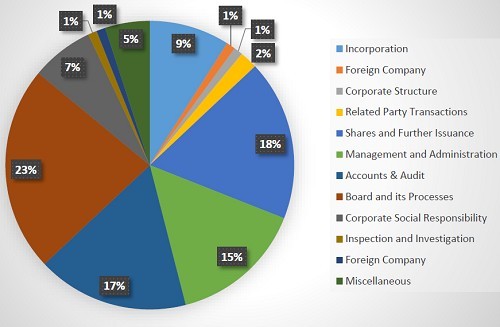

% of Amendments given

CAclubindia

CAclubindia