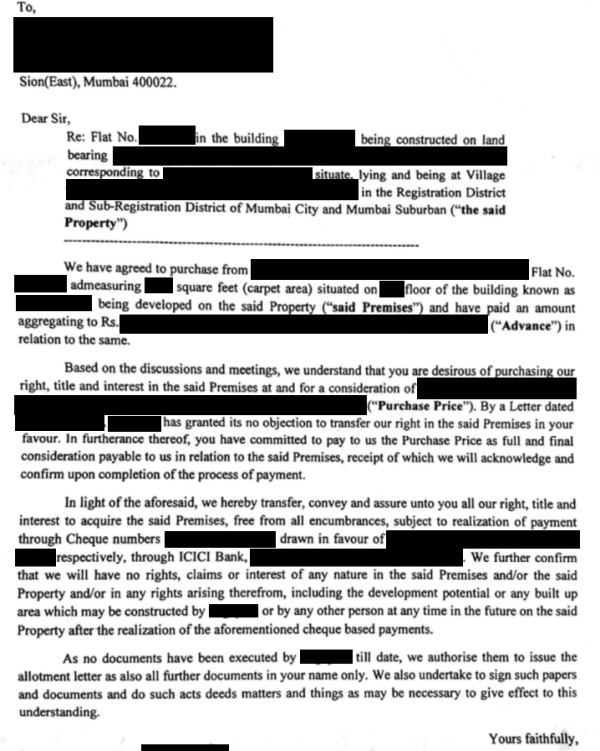

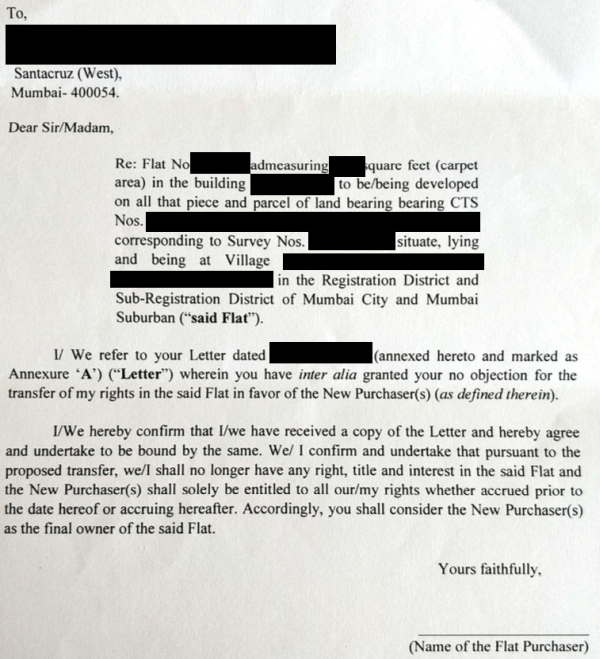

I had booked a property (residential flat) in pre-launch in December 2014 by paying 19.9% of the agreed upon Agreement Value from a JV of 2 builders (money was credited to the account of one of the two builders). Unfortunately, the project approvals did not come through. In June 2017, the other builder offered to pay back the invested amount along with 9% per annum simple interest in lieu of transfer of rights to the said property. I accepted the offer and the builder paid me the money after deducting 1% TDS.

Questions:

1. Will this transaction be considered as a capital asset sale transaction? Keep in mind that the construction of the underlying asset - residential flat - never even began

2. If yes, will it be considered a STCG transaction as per the 36 months holding period rule that was prevalent in December 2014 or will it be considered as a LTCG transaction as per the 24 months holding period rule that was in force at the time of resale (June 2017)?

3. How can I avoid paying tax on the gains I made as part of this transaction?

CAclubindia

CAclubindia