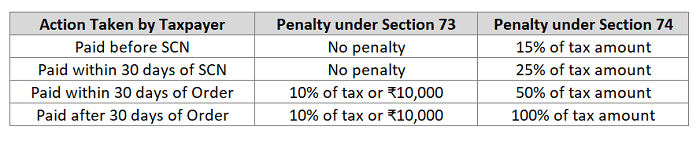

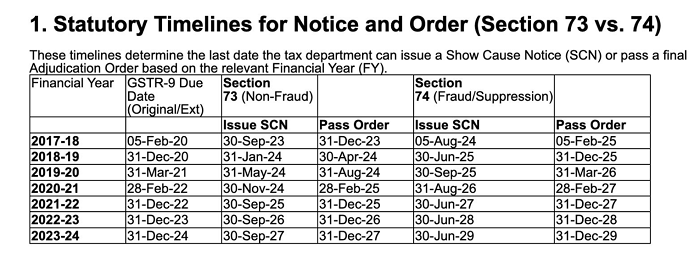

Penalties vary significantly depending on whether the case involves bona fide errors (Section 73) or intentional fraud/suppression (Section 74).

Penalties vary significantly depending on whether the case involves bona fide errors (Section 73) or intentional fraud/suppression (Section 74).

BHUPINDER SHAH AND COMPANY

New Delhi

CA Inter

View DetailsArvindkumar Maniar & Co.

Rajkot

CA

View DetailsTriveni Turbine Limited

Bengaluru

CA

View DetailsA R JADHAV AND ASSOCIATES

Mumbai

CA Inter

View Details

CAclubindia

CAclubindia