PF, ELSS, LIC, NSC, PPF,SSY, Tuition fee, FD for 5 years, ULIP, Home loan principal repayment, Post office saving scheme etc are the common strike off's in our mind as soon as we read "80C". This article states about drawing layout from records of client we owe, value addition we can deliver through strategically presenting the information. It also paves way for other best avenues which are knocking at our doorstep. Do CA's handling lots of client's resources can explore a world which is beyond 80C? The answer to these lies ahead…

[A] 80C- A limited scope

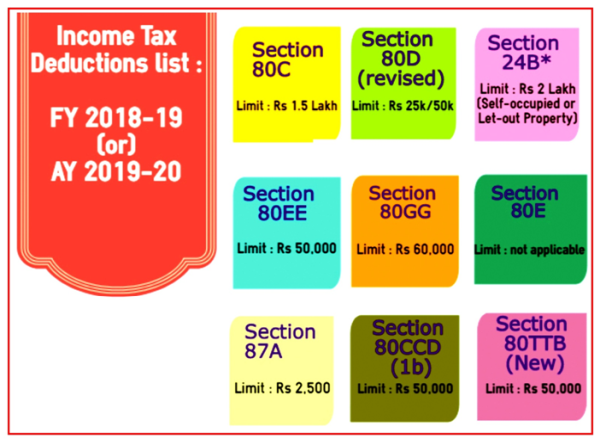

80C means LIC, PF, tuition fees, NSC, UTI plan...These words are too washed up to critique. Looking at services we provide and consideration we receive for filling ITR, one can give a thought to advertisements like" You are tax expert, we are investment expert". We being CA can provide insights apart from taxation. However u/s 80C our scope gets restricted to some extent. This is due to dump of dedicated amounts in tax savers instruments like HL-principal repayments, ELSS, NSC and predominant PF component covering paramount share for persons falling in higher tax slabs. By default tax saving is also restricted to Rs 1.5 lacks only. To plan over & above that income tax also requires to step out to other section, so do we !!!!

[B] World Beyond Section 80C (Magnifying from records)

Investments proof/ Form 16 are the common documents we receive while filling ITR. Apart from audit, accounts and taxation, can't there be space for financial roof of client's financial goal? Yes, it can be by magnifying from records. So let's begin the journey to other spectrum of sections after analyzing the very basic resource called "Bank statement".

- Are we missing huge "taxable" income credits (interest income) taken as income from other sources in ROI? Our role lies in analyzing banking habit of client. Ability to generate return more than FD comes into picture but only after suggesting six month contingency/emergency fund savings. (Real rate of return on FD v/s money market investments). For HNI clients, is the interest component in saving is more? If yes then, divergence of parked funds to flexi FD/RD, mini FD, etc options will increase their ROI by few percentages, but over and above that advance tax compliance portion for themselves will be shifted to bank. 80TTA will restrict to Rs 10000/40000, while our scope is extensive.

- Any SIP's? If banking habits are good, then why not to suggest correct time for lump sum investment instead of SIP( Systematic Investment Plan) which averages the return on investment and also gives rise to SWP (Systematic Withdrawal Plan).Though it's coverage falls in ambit of 80C, a world beyond 80C is too large to cover 80C!!

Mutual Fund statement -Tax savers? Not really required. Going through limit u/s 80C , if it's already exhausted with tuition fees and other regular components like PF, why is there necessity to invest in tax saver schemes of MF? Instead multi-cap, small cap and other varied options can be looked. Are we noticing broker details in MF statement, direct or regular plan is taken? If through broker(regular plan), then client knows about TER? Real return decreases by adopting broker route, so net return(compounding effect) after deducting TER should be evaluated and explained. Data analytics can be drawn for retail investors through direct route in equity funds from AMFI. Only 10% invests via direct route!! If investments are not made through broker ,instead direct route is opted then awareness of CKYC, nominee, FATCA/CRS declarations, personal e-mail ID updation instead of giving official mail ID's and reading factsheets were the exercise performed before investing? All answers to questions can be found by viewing MF statement.

Talking about mutual funds , reminds me of an event witnessed recently.

Parents generally give kids pocket money. In earlier days, kids used to save in their piggy bag , which 21st century kids now think of investing in mutual fund from small amount of say Rs 500 by seeing advertisement or going through comic strips "Choti saving se kuch bada karo, MF sahi hai". Hat's off to their thinking as they now don't opt for soft cushion of FD!

If these is the thinking of 21st century, can't CA give more insights for healthy saving to India's future? Of course, we being the strategic partner ought to have conceptual clarity of time value of money, rebalancing of portfolio, ETF's , portability options and so on.... the latest being REIT's.

Huge bonus credits?Any client will always think of buying a real estate. All concerns finds one solution i.e."Tax impact" irrespective of property be under construction, land purchase, construction or resale and it's effect under house property, 80C and exemption.

Another very crucial aspect of "Estate planning" is often missed out. No one ever wish to leave debt in succession for his family members, it's all about planning and documenting it which makes wealth gathered till the date, worthy "for the people, of the people and by the people". Nowadays companies also plan succession employee keeping in view going concern of business; If for non-human's succession is important , then can't we empathies its value for human's? They must be made aware of this "soothing factor" .

Ultimate goal comes to one stop i.e. bringing them out of fence of FD and investing in stock market through direct or indirect way. One should never say that “investing in stock market is RISKY". Observing the current frauds taking place across the finance industry, the aforesaid saying could be iterated as “investing in stock market is ALSO risky". Gentle reminder any bank if liquidates, one can claim maximum benefit up to Rs one lakh only. Initiatives by our institute like investor awareness program, incorporating financial services and capital markets in syllabus are to be duly taken note of. Now, let's sail through sections.....

Section 80G : Donations

Experiencing the various man-made and natural calamities, we are well aware of funds opened to beat against such calamities like Kerala draught relief fund (CMDRF), CMPRF, etc. Apart from funds created, it's eligibility for 100% deduction is the thing to bring to notice for those client who delightfully donates.

Ch VI A (Section 80D : Medical Insurance)

Taken through company? 80D plans are floating with lots of schemes, floaters; private player’s schemes v/s jeevan arogya could be interesting. When any client brings sweet for upcoming family members, do they have Insurance prior hand to enjoy that occasion instead of expensing it out of pocket? The reason is most of Insurance companies don't accept Insurance after certain weeks in maternity or after delivery:- 6 months. Exclusions and sub limit information are the paramount data each should be made aware of to avoid unexpected surprises. E.g. Room rent restricted to 10% of sum assured.

How many of us are using NIR platform for all policies? I guess handful of us may be. New India-digital India is live and so should we. It takes only one minute to opt for e-Insurance or updation in existing policies. It serves as preventive and hassle free measure in case of lost of physical documents or any contingencies. It's benefits, procedures, application, FAQ's are just a click away. Slogan states that "Apke vaade, sar aankhon par", hence it becomes our duty to give reminder for " Apke vaade" made at the time of buying insurance.

We always have risk vs return running in our vein. That's the basic logic anyone will apply while getting into Insurance. One always wishes that risk is covered by premium, what is return there? It's not always money or occurrence of events but knowledge gained for cradle to grave of Insurance i.e. claims, premiums, riders, top-ups, annuity, settlement options and latest e-form. Literacy in lieu of premium weigh elite for this product.

Apart from LIC & medical cover, can we make them invest in PMSBY( Pradhan Mantri Suraksha Bima Yojana) Rs 12 & Rs 33 mandatorily and stand true at our maxim of " CA partner in nation building". It's about explaining what benefit one gets just by spending a minimal amount of less than Rs 50. Do we observe ULIP in one's portfolio and also term insurance? Protection against risk should be adequate but excess to be avoided. Also there are products to explore which gives dual benefits of section 80C and 80D.

Section 80CCD1(B): NPS

Pension fund invested just to get additional benefit of Rs 50000?Is it the ultimate goal? No, it’s not only about additional benefit, but from sowing those seeds when one gets PRAN(Permanent Retirement Account Number) ,nurturing it by bringing clarity about accumulation & distribution and harvesting by maximizing return with a reminder to opt for annuity selection before six month of maturity will bear "fruit of additional benefit in real sense".

Also a comparative study about exit options at various intervals on various occasions viz first home purchase purpose after 3 years from inception, return under NPS vs APY & using Tier II account u/s 80C,etc… could serve as fertilizers. Any long term investments should be communicated to family members especially instruments like pension funds, these advice serve as initiative by us to bring awareness across people. These area opens wide scope for retirement planning because you come to know about the behavior of client as soon as they opt for pension schemes.

One of the incident turning the table is that parents or family members of female investing in such schemes taking into account the retirement planning for them to make some sort of saving "Today" which soothes their way in life's turbulence of different roles she plays from child to woman. Really this socialist thinking is bridging the gap between ends of spectrum. As addressed by honorable PM Modiji, "Our CA community must ensure transformation of our economy towards a New India where integrity is valued and glory of nation in all domains is established." Thinking beyond finance, taxation and audit, thinking socially, and our ability to take 360* view is unquestionable for sure.

80E: Interest paid on loan taken for higher education

Very rare, but yes, this section is getting hit by "Learning Lovers". Not only BYJU's is emerging in children education, but also initiates by almost all institutions across the globe are mammoth, which is looked as healthy means of fostering change. The same can be witnessed by taking example of our own institute, how? By spreading horizons of knowledge through all forms like e-learning and across varied areas addressing each category of people. E.g. Non finance executive courses, post CA qualification courses, certifications, etc.

After exploring the world and form the universe of information gathered, it's time to design layout and draft ways to communicate. We may not owe "all" resources required to analyze, but strategically presenting it opens up inalienable access to required documents. Two views can be drawn. 1st is for the people who are in industry. They can start to have look at their own portfolio. 2nd for the practicing member. Sub -bifurcations based on client could be extended.

[C] Wrap up

After exploring the world and form the universe of information gathered, it's time to design layout and draft ways to communicate. We may not owe "all" resources required to analyze, but strategically presenting it opens up inalienable access to required documents. Two views can be drawn. 1st is for the people who are in industry. They can start to have look at their own portfolio. 2nd for the practicing member. Sub -bifurcations based on client could be extended.

A basic resource one can start from their office is articles, very small portfolio, but awareness and the ideas with which they comes up, paves way for prospective investor. Moving ahead with our own investments/returns and patterns gives insights to our strength and grip on core areas, where we have generated return as desired. This is crucial as it leads to self-actualization and boosts confidence. Next comes our client base and type of service we offer them. Finding out relevant information and most important a chance to expand our horizon is present? If yes, then definitely we can't leave any stone unturned.

Ways to communicate may be direct or indirect, which will ultimately aim to play our cards right. Indirect ways like drafting questionnaire while providing usual services, gentle reminder or offbeat call during market swings and innovative mail crafted in form of factsheet and ending with question," Hope you never missed tracking your investment factsheet?" gets onto one of the roads that diverge from paved trails. Direct ways include formally offering financial services. Precluding about which agency to take up in financial serves stripes the straddle waves in our mind, isn't it? The answer is

without agency we can. How? Without taking agency or by-passing broker way and boosting direct investment route enlightens way to investor awareness in real sense.

It empathies a stints of social service satisfaction along with consideration. One can always demark dictum of service scope v/s consideration charged by applying due diligence and explaining the client scope of analysis which is " atomic" in finance field. Divergent trends, window dressing, teeming and lading, credit appraisals, ratings, Ind -AS impact of financial statements, off balance sheet items ..etc are all vigilant factors standing at centre of financial analysis. Looking beyond a factsheet is what CA can crack craft fully.

Skeleton of Balance sheet is firmly fitted in our body that we "Trust but verify".This maxim best suits in current scenario of scams witnessed and sounds sensible when we say for balance sheet that we know "what is balance and what is sheet". To make client realize aforesaid facts , it's very crucial that we draw adequate inferences from data.

Is it the only financial advice/analysis expected from our end? No, there is no limit to serve when our profession is addressed as," Flag bearers of Indian Excellence". It stretches spheres to the realm of knowledge. Wrapping it up, I would say it's high time to feel the paradigm shift in our profession by cooking the nest egg besides balancing the books and ending up with golden handshake in the country once called," Golden Sparrow".

[D] Conclusion

Not just earning but investing or allocating hard earned money is equally important. Explaining the financial figures in those investments of client and co-relating them to their financial goals paves way for blue ocean areas for CA's!!Blue ocean areas are those which are emerging areas apart from routine well known in the market. Examples of the same could be forensic audits, valuation, insolvency and bankruptcy, etc. Asset allocation and product knowledge are the key to wealth creation, which falls under our fiduciary responsibility bucket. We should make ourselves portable by reshuffling portfolio of services , thereby keeping pace with sustained progress.

Resources are ample just data mining through eyes of CA, a financial touch is awaiting client retention forever. Creating opportunity for varied services is laying at our office records only, which is understood from above look depicting a snapshot without any figures, explaining the importance of figures!!

So, let's gear up to galvanize the glow of our profession with gamut of services and let the audit, IT, taxation think tank turn the table to ticking clock of need.

I hope the journey to the world beyond 80C has a limit called "SKY" with stroke of our "Signature". As said by Adnan Nalwala, "Do whatever you want, provided the outcome is Income"

CAclubindia

CAclubindia