After going through lot of ups & downs, twists & turns, government has finally notified the TDS provisions under GST w.e.f 01-10-2018. Let us discuss in a simple yet comprehensive manner, everything about TDS in GST.

1. What is TDS under GST?

• Generally, the onus to collect and deposit tax lies with the supplier of goods or service in GST. However, in few cases, the onus would be on the recipient to deposit the applicable GST to the government.

• TDS is one of the means of collecting GST from the recipient. However, unlike section 9(3), 9(4) where the recipientpays GST at applicable rates(5/12/18/28, as the case may be), here the recipient only deducts a certain percentage fromthe value of supply(2%) and disburses the same to the government. In case of RCM provisions, the onus to pay tax is on the recipient of services or goods; however, in TDS, the onus of tax payment still lies with the supplier of goods/services. Onlyrecipient, on behalf of supplier, would deposit (not pay)a certain portion of tax.

• These provisions are applicable only to persons notified. The person deducting the amount (generally receiver of supply) is the deductor and the other person (generally supplier) is the deductee.

2. Who are the persons notified to deduct TDS?

|

Category of persons |

Section |

Example |

|

Department or an establishment of CG/SG |

Category of persons notified u/s 51(1) |

ISRO (Department of space) |

|

Local authority |

Panchayat, as defined in Article 243(d) of Constitution |

|

|

Governmental agencies |

Defence Research and Development Organisation (DRDO) |

|

|

Authority or board, set up by an act of parliament or state legislature |

Category of persons notified vide Notification 50/2018 CT dated 13-09-2018 |

IIM’s (set up by IIM Act) |

|

Authority or board, established by any govt. with 51% or more participation by way of equity or control |

Bharat Heavy Electricals Limited |

|

|

Society established under CG/SG/local authorities |

Amul |

|

|

Public sector undertakings |

Air India Limited |

3. Why was TDS introduced?

• It has been introduced to bring high value transactions under proper control, to curb fraudulent transactions and restrain tax avoidance. It is also aimed to bring the unorganized sector into the tax net.

• This is not new in indirect taxes. It was in force in Maharashtra and other states in the earlier VAT regime. However, TDS was applicable only for works contract transactions; now, its base has been widened to include all transactions (goods as well as services), to a specific category of persons.

• This is mainly applicable for government and governmental agencies. Usually, the outward supplies provided by government/governmental agencies would be exempt; thus, they wouldn’t be eligible for ITC. So, there is an inherent risk that the supplier doesn’t pay the applicable GST to the government (even, recipient wouldn’t be concerned as he is not eligible for ITC). To ensure that this risk is minimised, TDS provisions are made applicable in GST.

4. When would TDS be deductible?

• Amount: - TDS would be deducted when the total value of supply, under a contract, exceeds Rs. 2.5 lakhs [Section 51(1)].

• Rate: - The deductor would deduct TDS at the rate of 2% [1% CGST & 1% SGST or 2% IGST] from the payment made/credited to the supplier of taxable goods or services.

• Computation of value of supply: - For the purpose of TDS, value of supply would be the amount excluding CGST, SGST, IGST, UTGST and Cess, as indicated in the invoice.

• Time of deduction:- TDS would be deductible at the time when the payment is made or credited to the supplier.

Example:-

1. Assume, the payeris a society registered under Central Govt; state whether TDS would apply or not in the following cases:-

|

Taxable value |

GST rate (%) |

Invoice value |

TDS deductible |

Reasons |

|

2,00,000 |

12 |

2,24,000 |

No |

As value of supply is less than 2.5 lakhs, TDS is not applicable. |

|

2,45,000 |

5 |

2,57,250 |

No |

Value of supply is the value excluding GST, which is 2, 45,000. Since, it is less than 2.5 lakhs, TDS is not deductible |

|

2,50,000 |

18 |

2,95,000 |

No |

Value of supply is Rs 2.5 lakhs; it doesn’t exceed Rs. 2, 50,000. |

|

2,60,000 |

12 |

2,91,200 |

Yes |

Applicable as value of supply(excluding GST) exceeds Rs. 2.5 lakhs |

|

2,70,000 |

Exempt |

2,70,000 |

No |

TDS is applicable only to taxable goods or services. |

2. Suppose Supplier X entered into a works contract agreement with ONGC (public sector undertaking), wherein the payment is to be made and invoices to be issued in installments, as given below. Determine the applicability of TDS provisions.

|

Percentage of completion |

Payment(Rs. excluding GST at 18%) |

|

50% |

2,25,000 |

|

100% |

2,00,000 |

|

6 months after completion |

1,50,000 |

Answer: - TDS will have to be have to be deducted, as the total value of supply under a contract is Rs. 5.75 lacs. It is immaterial if the payment are made in installments or if the invoice is issued in smaller chunks. As long as the total value of the contract(excluding GST) exceeds Rs. 2.5 lacs and the payer is a person specified u/s 51, TDS at the rate of 2% would be deductible.

5. Cases when TDS need not be deducted:-

No deduction needs to be made if the location of the supplier and the place of supply is in a State/UT, which is different from the State/ UT of registration of the recipient [Proviso to section 51(1)]

|

Particulars |

Case-1 |

Case-2 |

Case-3 |

|

Location of Supplier |

Delhi |

Delhi |

Delhi |

|

Place of Supply |

Delhi |

Bangalore |

Delhi |

|

Type of Tax |

CGST, SGST(Delhi) |

IGST |

CGST, SGST(Delhi) |

|

Location of recipient |

Delhi |

Bangalore |

Bangalore |

|

Whether TDS deductible |

Yes; deduct 1% CGST, 1% SGST |

Deduct 2% IGST |

No; as location of supplier and POS is in Delhi, whereas location of recipient is in Bangalore. |

6. Procedural requirements:-

• Registration:- Every person, who is required to deduct tax, shall obtain registration irrespective of the fact that whether such person is separately registered under the Act or not [Section 24(vi)]. Hence, there are no threshold limits for registration as deductor and registration is mandatory.

• Returns to be filed by deductor:- The deductor needs to file GSTR-7 electronically through common portal, as per rule 66(1). The amount needs to be paid within 10 days after the end of month in which such deduction is made [Section 51(2)]

• Whether TDS certificate is required to be issued to the deductee: -Just like the income tax Law, the deductor would require furnishing a certificate mentioning the contract value, rate of deduction, amount deducted, amount paid to the Government and other particulars in form GSTR-7A. [Section 51(3)]

• Time limit for furnishing TDS certificate:- The deductor would furnish the TDS certificate within 5 days of crediting such amount to the government. [Section 51(4)]

• Penalty for delay in furnishing certificate:- Late fee payable would be Rs. 100 per day (from the day after the expiry of such five days) until the failure is rectified (i.e.until the date such certificate is furnished), subject to a maximum of Rs. 5,000.

• How can deductee(supplier) claim such credit:-

• The amount would be credited to the electronic cash ledger of the deductee(supplier). [Section 51(5)]

• The supplier may use the same to set off against his output tax liability for the period.

• Balance, if any, after set off against output tax liability, may be claimed as refund in form RFD-01 on the common portal.

• What if the deductor doesn’t deposit such amount:- He would be liable to pay interest at 18%, in addition to the amount of tax deducted. [Section 51(6)]

• What if excess amount has been deducted erroneously:-

• The deductor or deductee may claim refund of the same, in accordance with section 54.

• However, if amount has already been credited to electronic cash ledger of the deductee, refund would not be granted to the deductor. In other words, deductee has to obtain the refund himself in such cases.[Proviso to section 51(8)]

|

Whether amount has been credited to the electronic cash ledger |

No |

Yes |

|

Persons eligible for refund |

Deductor or deductee |

Deductee only |

7. Commonly asked Questions:-

• Whether TDS provisions are applicable on IGST (inter-state) transactions also?

• TDS would be applicable on IGST transactions as well, provided the place of supply and location of recipient fall in the same state. [Proviso to section 20 of IGST Act]

• However, notification 50/2018 CT has notified effective date of TDS as 01-10-2018 for intra-state supplies; similar notifications have been issued in SGST also. However, no notification is issued in IGST till date. Thus, the effective date of TDS for IGST transactions is yet to be notified.

• Goods have been supplied on 05-09-2018; however, the payment is made on 07-10-2018. Whether TDS needs to be deducted?

• In terms of section 51(1), TDS is to be deducted from the payment made or credited to the supplier. In other words, the factor to be considered for deducting TDS is payment, not supply.

• So, even if the supply has taken place before the appointed date (01-10-2018), payment is made after the appointed date; thus, TDS would be deductible.

• Whether TDS is to be deducted in case of exempt supplies?

• TDS would be deductible from the payment made to supplier of taxable goods or service [section 51(1)]. As the goods are exempt, no need to deduct TDS.

• Further, the objective of TDS is to ensure better compliance, not to tax exempt supplies. Thus, no need to deduct TDS.

• Whether TDS is to be deducted in case of supplies from unregistered persons?

Answer: - As URP cannot issue a tax invoice, there is no need to deduct TDS in case of supplies from unregistered persons.

• State the differences between TDS and RCM provisions

|

Particulars |

TDS |

RCM |

|

Liability to pay tax |

Liability to pay tax with supplier; deductor only deduct and pay 2% to govt. which will be credited to the cash ledger |

The onus to pay tax lies wholly with the recipient of goods/service |

|

Collection of GST on invoice |

The supplier would collect GST from the payer. Only 2% of basic value is withheld and paid to govt. |

The GST portion is not paid to supplier. Recipient directly pays the same to govt. |

|

Documents to be issued |

TDS certificate to be issued |

Self-invoice and payment voucher to be issued |

|

Payment of tax to govt. |

Payment to govt. will always be at 2% of taxable value |

Payment to govt. will be on applicable rates(5/12/18/28) on taxable value |

|

Requirement for separate return |

Requirement for separate return, i.e. GSTR-7; in addition to the monthly GSTR-3B |

No requirement for separate return, these details to be disclosed in monthly return (GSTR-3B) |

• How to determine the applicability of TDS if a taxable as well as exempt supply is undertaken, on a single contract. Suppose the total value of contract(excluding GST at 12%) is Rs. 5,50,000. The taxable portion is Rs. 2,25,000(without GST). Examine whether TDS is deductible or not. Would your answer differ if the taxable portion is Rs. 3,75,000(excluding GST)

• Exempt supplies are to be wholly ignored for the purpose of TDS deduction. If the value of supply of taxable portion(excluding GST and cess) exceeds RS. 2.5 lakhs, then TDS would be deductible (only on the taxable portion).

• In the given case, taxable portion is Rs. 2,25,000; thus, TDS is not applicable.

• However, if the taxable portion is Rs. 3,75,000, TDS at 2% would be deductible on Rs. 3,75,000.

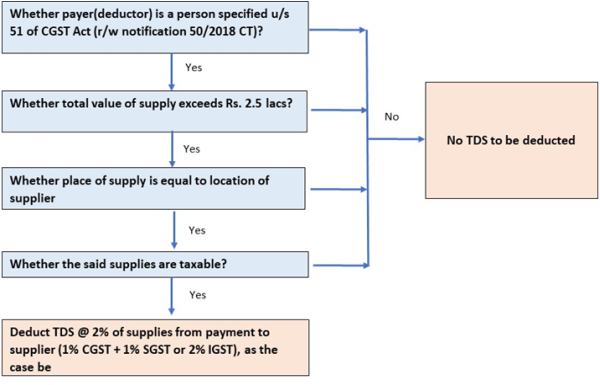

8. Flowchart of TDS under GST

CAclubindia

CAclubindia