TDS, means Tax Deducted at Source, seems to be very tedious at the first instance. I have come across many people who take TDS as a very complicated task. This made me write an article on this topic. This article is intended only for the basic understanding of the concept of TDS. I would be pleased to write about each section in particular. But to begin with, this article has been written keeping in mind the beginners for this concept. Further, this article is related only to the understanding of the concept. There is the also other side of the coin, i.e. the difficulties faced in practical life regarding TDS, which is not discussed here. There is a reason for it which is mentioned later in this article.

Introduction:

TDS means, as we all know, Tax Deducted at Source. This concept was introduced by the Income Tax Department in the year 2004. This concept is based on the system of “Pay as you Earn”. It means that, the Government shall get a part of your total tax, as soon as you have earned it. There were many reasons behind introduction of TDS by the department. Some of them are covered below:

a. The Government gets revenue round the year.

b. Once tax is deducted and return is filed, the information about the person whose tax is deducted is already with the department. So, in order to avoid any consequences, that person files his Income Tax Return.

c. To curb the fake and bogus expenditure claimed by assesses. This is because if tax is not deducted and paid to the Government, the expenditure is disallowed and tax has to be paid by the person claiming that expenditure.

d. To expand the tax base in the nation.

National Securities Depository Limited (NSDL), after its success in Indian Capital Market for scripless settlement at Stock Exchanges, started its process for forming the nationwide Tax Information Network, i.e. TIN, on behalf of the Income Tax Department. TDS was also made a part of TIN.

Important Terms about TDS:

1. Deductor: The person responsible to deduct the tax is called as deductor. Deductor is the person who shall deduct the tax from the payments eligible for TDS and pay it to the Government.

2. Deductee: The person whose tax is deducted and paid to Government is called as deductee. For the payments eligible for TDS, the deductee does not get full payment against his invoices. The amount is paid net of TDS.

3.TAN: TAN is Tax Deduction Account Number. Every deductor has to apply for TAN and on successful allotment of TAN he has to pay the tax so deducted on account of this TAN. TAN is unique for each deductor.

4. TDS Return: After deduction of tax and payment thereof to the Government, the deductor has to file quarterly statements giving the details of the deductees and payments made to them.

5. TDS Certificate: After filing the quarterly statements, the deductor has to issue TDS certificate to the deductee mentioning therein the details of the amounts paid and tax deducted.

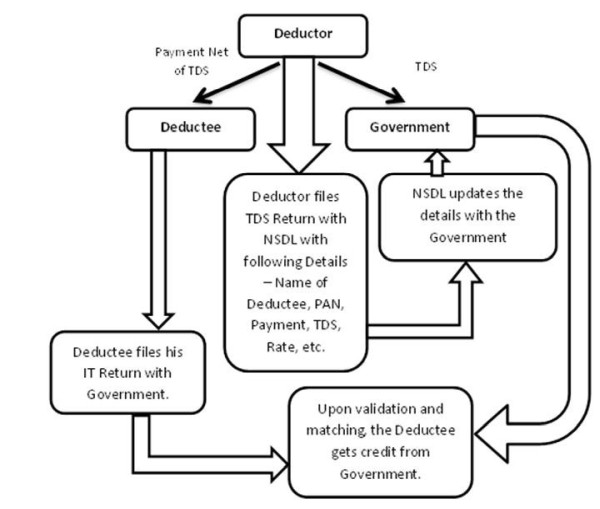

How does the Mechanism Work?

The TDS mechanism works in the following manner. I have tried my best to make you understand graphically.

This is the basic theme about TDS and its mechanism.

Earlier in the article, I have mentioned that there is another side of the coin also, i.e. the darker side. Theoretically, TDS is not Tedious, but due to lack of proper information and reporting, TDS has become a Tedious job. In my next article, I’ll include the practical difficulties and tips to prevent practical difficulties that have led TDS to become Tedious.

CA Amol Gopal Kabra

CAclubindia

CAclubindia