AS PER SECTION 44AB OF INCOME TAX ACT,

Tax Audit is an Examination or Review of accounts of any Business or Profession carried out by taxpayers from an income tax viewpoint

A. Conducted to achieve the following objectives

- Ensure proper maintenance and correctness of books and certification of the same by a tax auditor

- Reporting

a) observations/discrepancies noted by tax auditor AFTER EXAMINATION

b) prescribed information such as tax depreciation, compliance of income tax law

- Checks frauds and malpractices in filing income tax returns.

All these enable tax authorities in verifying the correctness of income tax returns filed by the taxpayer. Calculation and verification of total income, claim for deductions etc. also becomes easier

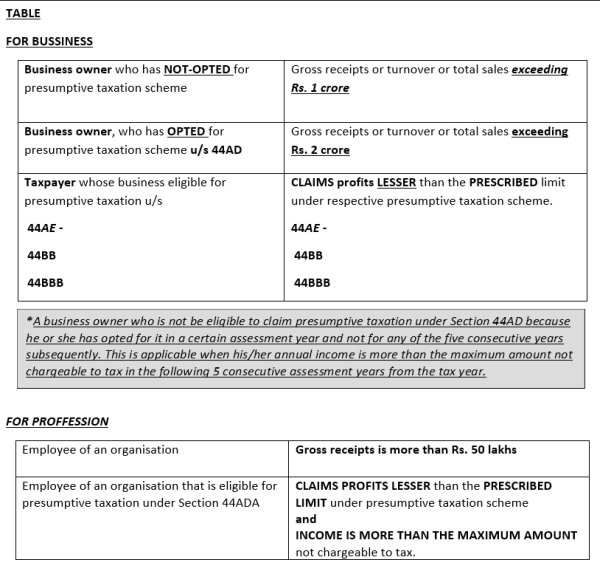

B. Who is mandatorily subject to tax audit?

Refer Table

C. What happens if a person is required to get his accounts audited under any other law

Like Statutory audit of companies under company law provisions?

In such cases, the Taxpayer need not get his accounts audited again for income tax purposes. It is sufficient if accounts are audited under such other law before the due date of filing the return

D. What constitutes Audit Report?

Tax auditor shall furnish his report in a prescribed form which could be either Form 3CA or Form 3CB where:

Form No. 3CA is furnished when a person carrying on business or profession is already mandated to get his accounts audited under any other law.

Form No. 3CB is furnished when a person carrying on business or profession is not required to get his accounts audited under any other law.

In case of both above mentioned reports, tax auditor must furnish the prescribed particulars in Form No. 3CD, which forms part of audit report.

E. How and when tax audit report shall be furnished?

Tax auditor shall furnish tax audit report online

- By using his login details in the capacity of ‘Chartered Accountant’.

- Taxpayer shall also add CA details in their login portal.

- Once the tax auditor uploads the audit report, same should either be accepted/rejected by taxpayer in their login portal.

- If rejected for any reason, all the procedures need to be followed again till the audit report is accepted by the taxpayer

You must file the tax audit report on or before the due date of filing the return of income i.e. 30 September of the subsequent year

in case the taxpayer has entered into an international transaction then 30 November of the subsequent year

F. Penalty of non-filing or delay in filing tax audit report –

Least of the following may be levied as a penalty:

- 0.5% of the total sales, turnover or gross receipts

- Rs 1,50,000

Also Read: Tax Audit Section 44AB, the limit for business Rs 1crore or 2 crore?

SOME RECENT AMENDMENTS MADE BY FINANCE ACT 2020 i.e. APPLICABLE FOR FY 2020-21

The Finance Act 2020 has made amendment in section 44AB by inserting a proviso in clause (a) of Section 44AB. As per the new proviso, the tax audit turnover limit would be INR 5 Crores in case the following two conditions are satisfied:

Condition-1: Total of all the amount received (including the amount received towards sales or turnover or gross receipts) IN CASH during the previous year doesn’t exceed 5% of such amounts; and

Condition-2: Total of all the payments (including amount incurred for expenditure) IN CASH during the previous year does not exceed 5% of such payments

Thus, in case the person satisfies both the above conditions, then the person is not required to gets the books of accounts audited till the sales or turnover or gross receipts of the person exceeds INR 5 Crores.

CAclubindia

CAclubindia