Hello everyone as a professor its very important to understand what material is being used for drafting papers, understand the trend so that I can make students hit bulls eye. So we worked for many hours to give you accurate and path breaking analysis. Last time it was out of box paper this time, ICAI drafted comparatively much easier paper. Few questions were tricky and some were again from remote corners of module.

After analyzing papers setting for so many years, I have come to conclusion, that paper setters of ICAI draft paper from either remote corners of module or PM / RTP / Past Papers. So in some attempt you may face many questions which you have not seen in past or it could be cake walk if many questions are from PM / RTP / Past Papers etc, but scoring will depend on how strong is you understanding of subject and how well you connect and present your knowledge. I have seen many students cram from PM and put it in exams, but they don't get good marks because there answer is not expressing real meaning examples etc

So PM / RTP is must but it cannot be first and base of your studies.

Source of Drafting Paper in May17

You will be surprised to see many of below facts. (Paper was of 120 marks) (Don't add up below marks there is overlapping of the source)

1. After last times analysis, I saw a trend that many questions were asked from module and PM which were in bold & italics, has diagram, chart or highlighted as case study. We even identified all such areas and uploaded important file online. So we suggested all students who came in touch that target such areas.

Bingo guys this time 25 Marks paper was from such areas. May be ICAI wanted target changes or it was natural human behaviour to pick such questions. So those who followed this strategy got rich dividends with very low time investment.

2. ICAI has a problem it has 2 materials for same topic with little bit of difference, in this exam 3 questions were asked from such topics on sampling, now sampling is covered in SA 530 also and special audit technique also. I personally feel content in SA is better more logical, better expressed and easy to retain. So if students follow SA 530 content it will be fine. These 3 questions accounted for 14 Marks on only one point related to sampling. All these points were one below another in special audit chapter 5.2.1 / 5.2.5 / 5.2.6

3. Last 5 years RTPs contributed to 75 Marks of paper. May 17 RTP contributed around 20 marks, that is superb number. And surprisingly Nov 15 RTP contributed highest 20 marks. (Last time no questions were asked from recent RTP)

4. Last 10 years papers contributed to 60 Marks of paper.

5. PM contributed to 59 Marks paper, last time it was 37. So this time there was drastic increase. This also indicates PM doesn't cover all RTP questions.

6. There were questions of 29 Marks exclusively (Not Covered in PM / RTP) from module.

7. We have linked our notes to all PM questions, through PM analysis file so that you can covers PM along with notes efficiently and effectively. Students those who followed our notes and covered PM could target 111 marks.

I will suggest follow your class notes as base, very important for understanding and retention + PM for practicing questions. You should keep Module & Collection of past 5 year RTPs to see if any particular topic is left out, just see headings and topic questions are targeting.

Important Note:- In these suggested answer lot of content is picked from PM, module, bare act etc ICAI may not be expecting some points in details as covered below. So don't worry if your answer doesn't match as it is. Further ICAI gives 40-50% marks if your content is not bang on target. These answers are framed to help students understand paper and what was expected.

Q1(a) - M/s. ABC & Co. is an audit firm having partners Mr. A, Mr. B and Mr. C, whose tenure as statutory auditor in R Ltd. a listed entity, has expired as per the companies Act, 2013. M/s. XY is another audit firm which is appointed as the statutory auditor of R Ltd. for the subsequent year. Mr. A joins M/s. XY as partner, 3 months after it was appointed as the statutory auditor of R Ltd. Comment.

Similar Question in RTP May 16 Q7(a)

Alternative 1 (New Firm Disqualified)

Applicable:- Section 139 (2) &Company Audit & Auditor Rules (Rule 6 (3)(ii) Explanation II)

Sec & Rules:- if a partner, who is in charge of an audit firm and also certifies the financial statements of the company, retires from the said firm and joins another firm of chartered accountants, such other firm shall also be ineligible to be appointed for a period of five years.

Facts & Discussion of Case: In above case rotation is applicable to R Ltd and their auditor M/s ABC & Co should be replaced, and they are replaced by M/s XY. But one of the partner 'A' joins firm XY as partner. Further we assume that he has left the old firm and he was signing partner in old firm (M/s ABC & Co).

From this point it is clear that new firm will get ineligible (disqualified) to be auditor for 5 years.

Conclusion: New firm M/s XY will be disqualified as signing partner has left the firm under rotation and joined M/s XY

Alternative 2 (New Firm Not Disqualified)

Applicable: Section 139 (2)

Sec & Rules: Provided further that as on the date of appointment no audit firm having a common partner or partners to the other audit firm, whose tenure has expired in a company immediately preceding the financial year, shall be appointed as auditor of the same company for a period of five years.

Facts & Discussion of Case: In above case, rotation is applicable to R Ltd and their auditor M/s ABC & Co should be replaced, and they are replaced by M/s XY. But one of the partner 'A' joins firm XY as a partner. Further, we assume that he has not left the old firm M/s ABC & Coso this is common partner situation, but an important point is common partner situation should be seen at the time of appointment. Here common partner situation has come after 3 months of appointments, so it is perfectly fine.

Conclusion:- New firm M/s XY will not be disqualified / ineligible as there is no common partner situation on date of appointment but after 3 months.

Extra Points

Now similar question but not the same was there on May 16 RTP Q7(a), but in this question, it was clearly specified that partner retires from OLD Audit firm and he is signing partner.

So our exams question was different. If we assume that partner who joins NEW Audit Firm has retired from old firm and he was signing partner then we can say that as per Rule 6 (3)(ii) Explanation II of Sec 139(2) such new firm will also be ineligible / disqualified for such 5 years.

But one more possibility is there if don't assume he retired from old firm then it will become case of common partner, As per 2nd proviso to sec 139 (2) we have to see situation of common partner at the date of appointment, in this case common partner situation arises 3 months after appointment so this position is absolutely fine, so new firm will not be disqualified.

So 2 answers are possible for above company audit question. Because certain things are missing and it is explicitly said that joining is after 3 months I prefer 2nd as more appropriate answer.

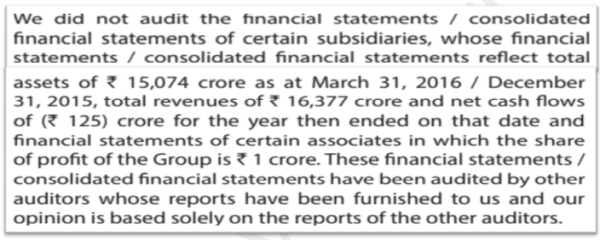

Q1(b) C Ltd. is holding 55% shares of D Ltd. AB & Associates are statutory auditors of C Ltd. whereas for D Ltd. there is another firm appointed as statutory auditors. what are the reporting responsibilities of M/s. AB & Associates for audit of consolidated financial statements ?

RTP May 15 Q11 / PM Ch10 Q7

Answer: When the Parent's Auditor is not the Auditor of all its Components:

SA 600

In a case where the parent's auditor is not the auditor of all the components included in the consolidated financial statements, the auditor of the consolidated financial statements should also consider the requirement of SA 600 'Using the Work of Another Auditor'. (Which says about division of responsibility should be specified in audit report)

SA 706

As prescribed in SA 706 'Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor's Report', if the auditor considers it necessary to make reference to the audit of the other auditors, the auditor's report on the consolidated financial statements should disclose clearly the magnitude of the portion of the financial statements audited by the other auditor(s).

Quantification

This may be done by stating aggregate rupee amounts or percentages of total assets, revenues and cash flows of components included in the consolidated financial statements not audited by the parent's auditor.Total assets, revenues and cash flow not audited by the parent's auditor should be presented before giving effect to permanent and current period consolidation adjustments. Reference in the report of the auditor on the consolidated financial statements to the fact that part of the audit of the group was made by other auditor(s) is not to be construed as a qualification of the opinion but rather as an indication of the divided responsibility between the auditors of the parent and its subsidiaries.

(Material Subsidiary [OMP] Vs Immaterial Subsidiary [OMP Optional])

From Audit Report of Reliance Industries

Q1(c) "Moon Ltd. acquired 65% shares of Sun Ltd. on 28th October 2016 On 25th April 2017 they sold 25% shares of Sun Ltd. While preparing consolidated financial statements for the year ended 31st March, 2017, accountant of Moon Ltd. .did not consider financial statements of Sun Ltd. for consolidation. Comment."

RTP Q2(a) May 11/ RTP Q1(a) May 12/ PM Ch1 Q6(a)

Answer:

AS 21 Exclusions

Consolidation of Financial Statement: AS 21 'Consolidated Financial Statements', states that a subsidiary should be excluded from consolidation when:

(i) Control is intended to be temporary because the shares are acquired and held exclusively with a view to its subsequent disposal in the near future; or

(ii) Subsidiary operates under severe long-term restrictions which significantly impair its ability to transfer funds to the parent.

Current Case of Temporary Holding

Where an enterprise owns majority of voting power by virtue of ownership of the shares of another enterprise but shares are sold within 6 months hence, the control by the first mentioned enterprise would be considered temporary and the investments in such subsidiaries should be accounted for in accordance with AS 13 'Accounting for Investments'.

Schedule III

However, as per Section 129(3) of the Companies Act, 2013 read with Rule 6 of the Companies (Accounts) Rules, 2014, where a company having subsidiary, which is not required to prepare consolidated financial statements under the Accounting Standards, it shall be sufficient if the company complies with the provisions on consolidated financial statements provided in Schedule III to the Act.

And the requirement of schedule III is to mention the list of subsidiaries not consolidated along with reasons for the same.

Conclusion

In this case, Moon Ltd's intention is to dispose off the shares in the near future as shares are being sold on 25th April which is within 6 months, so it is quite clear that the control is temporary, however for the compliance of provisions related to consolidation of financial statements given under the Section 129(3) of the Companies Act, 2013 read with Companies (Accounts)Rules, 2014, H Ltd. is required to mention list of subsidiaries not consolidated along with reasons for the same.

Q1(d) While commencing the statutory audit of ABC company Ltd., the auditor undertook the risk assessment and found that the detection risk relating to a certain class of transactions cannot be reduced to acceptance level. Explain. PM Ch 4 Q15 / RTP Q5(a) Nov 16 / RTP Nov 13 / Exam Nov 11

Answer:

SA 315 & SA 330 Applicable

Assessment of Risk and Acceptable Level:

SA 315 and SA 330 'Identifying and Assessing the Risk of Material Misstatement Through Understanding the Entity and its Environment' and 'The Auditor's Responses to Assessed Risks'

Understanding Risks: Establishes standards on the procedures to be followed to obtain an understanding of the accounting and internal control systems and on audit risk and its components: inherent risk, control risk and detection risk.

Relationship between risk components: 'Detection risk' is the risk that an auditor's substantive procedures will not detect a misstatement that exists in an account balance or class of transactions that could be material. The higher the assessment of inherent and control risks, the more audit evidence the auditor should obtain from the performance of substantive procedures. When both inherent and control risks are assessed as high, the auditor needs to consider whether substantive procedures can provide sufficient appropriate audit evidence to reduce detection risk, and therefore audit risk, to an acceptable low level.

Ultimate Goal: SA 315 and SA 330 require that the auditor should use professional judgment to assess audit risk and to design audit procedures to ensure that it is reduced to an acceptably low level.

Failure to achieve Goal: If it cannot be reduced to an acceptable level, the auditor should express a qualified opinion or a disclaimer of opinion as may be appropriate.

Q2 (a) ABC co. Ltd. a company having trans-national operations, conducts its entire operations in a computerised Information Systems (CIS) environment. As the audit partner of M/s. XYZ & Co., draw out the audit plan for evaluating the reliability of controls. RTP Q20(c) Nov 15 / EXAM Nov 08

Answer:

Effect of Control on Audit

Audit Plan for Evaluating the Reliability of Controls in CIS Environment: In evaluating the effects of a control, the auditor needs to assess the reliability by considering the various attributes of a control. Some of the attributes for example are that the control is in place and is functioning as desired,

General Controls (CIS Department Level)

Generality versus specificity of the control with respect to the various types of errors and irregularities that might occur, general control inhibit the effect of a wide variety of errors and irregularities as they are more robust to change,

Specific Controls (Individual Application Level)

Controls in the application sub-system which tend to be specific control because the component in these sub-systems execute activities having less variety, that whether the control acts to prevent, detect or correct errors etc.

Auditor's Focus

The auditor focuses here on-

(i) Preventive controls: Controls which stop errors or irregularities from occurring. (Eg Computer Operation Controls)

(ii) Detective controls: Controls which identify errors and irregularities after they occur.(Eg Scanning unusual logins)

(iii) Corrective controls: Controls which remove the effects of errors and irregularities after they have been identified.(Eg Inquiry, Action, Punishment of such people)

The auditors are expected to see a higher density of preventive controls at the early stages of processing or conversely, they expect to see more detective and corrective controls later in system processing.

Further, while evaluating the reliability of controls, the auditor should:

System & Application Software

(vi) Prevent unauthorized amendments to the program;

(vii) Provide for safe custody of source code of application software and data files.

Input

(i) Ensure that authorized, correct and complete data is made available for processing;

(ii) Provide for timely detection and correction of errors.

Processing

(iii) Ensure that the case of interruption in the work of the CIS environment due to power, mechanical or processing failures, the system restarts without distorting the completion of the entries and records;

Output

(iv) Ensure that accuracy and completeness of output;

Safety & Security

(v) Provide adequate data security against fire and other calamities, wrong processing, frauds etc.,

Q2(b) Secure Bank Ltd. is working as a depository along with their normal banking activities. The securities and Exchange Board of India (SEBI) wants to appoint Mr. 'w' as an inspector to inspect books of accounts and records of the depository. Explain the purpose for which SEBI can appoint a person to inspect these books of accounts and records. RTP Q20(c) Nov 15/ Exam Nov 08

Answer: Purpose of Appointing Inspecting Officer of a Depository:

Investigation of Depository

The SEBI may appoint one or more persons as inspecting officer to undertake the inspection of the records, books of account, documents and infrastructure, systems and procedures or

Investigation of MF / Trustee / AMC etc

To investigate the affairs of a mutual fund, the trustees and asset Management Company for any of the following purposes, namely-

(Interests of Market)

(4) To ascertain whether the systems, procedures and safeguards are being followed in the interests and to secure the market; (Eg SMS system)

(5) To ensure that the affairs are being conducted in the interest of the Investors / Securities markets.(Eg Frauds in dormant, senior citizen accounts)

(Legal Compliance)

(1) To ensure that the books of accounts are maintained in the names specified in the regulations;(Eg Materialisation & Dematerialisation books)

(3) To ascertain whether the provisions of the Act, bye-laws agreements and these regulations are being complied;(Eg Maintaining books for 5 years)

(Complaints)

(2) To look into the complaints received from depositors' participant, beneficial owners or other persons;(Eg bonus shares not received)

Q2(c) The auditor should select sample items in such a way that the sample can be expected to be representative of the population. comment.

PM Ch5 Q10 Similar / RTP Q20(b) Similar Nov 15/ Exam May 12

Answer:

Basic Principle in Selection

Selection of the sample - The auditor should select sample items in such a way that the sample can be expected to be representative of the population. This requires that all items in the population have an opportunity of being selected.

Methods of Selection

There are many methods of selecting samples. The principal methods are as follows:

(a) Random selection (applied through random number generators, for example, random number tables).

(b) Systematic selection, in which the number of sampling units in the population is divided by the sample size to give a sampling interval, for example, 50, and having determined a starting point within the first 50, each 50th sampling unit thereafter is selected. Although the starting point may be determined haphazardly, the sample is more likely to be truly random if it is determined by use of a computerized random number generator or random number tables. When using systematic selection, the auditor would need to determine that sampling units within the population are not structured in such a way that the sampling interval corresponds to a particular pattern in the population.

Example (Just for understanding no need to write in exams)

Total Number of Sales 20 / Sample Size = 5 / Selection Interval = 20 ÷5 = 4 / Select Starting Point Randomly Between 1-4 , say 3, So selection will be 3 , 7, 11, 15, 19

|

Bill No |

Bill Amount |

|

1 |

50,000 |

|

2 |

3,00,000 |

|

3 |

1,00,000 |

|

4 |

2,50,000 |

|

5 |

1,00,000 |

|

6 |

75,000 |

|

7 |

25000 |

|

8 |

40,000 |

|

9 |

60,000 |

|

10 |

1,50,000 |

|

11 |

85,000 |

|

12 |

60,000 |

|

13 |

90,000 |

|

14 |

15,000 |

|

15 |

45,000 |

|

16 |

95,000 |

|

17 |

98,000 |

|

18 |

84,000 |

|

19 |

1,29,000 |

|

20 |

1,49,000 |

(c) Monetary Unit Sampling is a type of value-weighted selection in which sample size, selection and evaluation results in a conclusion in monetary amounts.

Example (Just for understanding no need to write in exams)

Total Sales 20,00,000 / Sample Size 5 / Monetary Interval between 2 bills should be 20,00,000 ÷5 = 4,00,000 / Select Starting Point Randomly Between (1 – 2,00,000) is say 620 /

Selection will be 620 / 4,00,620 / 8,00,620 / 12,00,620 / 16,00,620

|

Bill No |

Bill Amount |

Cumulative Amount |

Selection Base |

|

1 |

50,000 |

50,000 |

620 |

|

2 |

3,00,000 |

3,50,000 |

|

|

3 |

1,00,000 |

4,50,000 |

4,00,620 |

|

4 |

2,50,000 |

7,00,000 |

|

|

5 |

1,00,000 |

8,00,000 |

|

|

6 |

75,000 |

8,75,000 |

8,00,620 |

|

7 |

25000 |

9,00,000 |

|

|

8 |

40,000 |

9,40,000 |

|

|

9 |

60,000 |

10,00,000 |

|

|

10 |

1,50,000 |

11,50,000 |

|

|

11 |

85,000 |

12,35,000 |

12,00,620 |

|

12 |

60,000 |

12,95,000 |

|

|

13 |

90,000 |

13,85,000 |

|

|

14 |

15,000 |

14,00,000 |

|

|

15 |

45,000 |

14,45,000 |

|

|

16 |

95,000 |

15,40,000 |

|

|

17 |

98,000 |

16,38,000 |

16,00,620 |

|

18 |

84,000 |

17,22,000 |

|

|

19 |

1,29,000 |

18,51,000 |

|

|

20 |

1,49,000 |

20,00,000 |

(d) Haphazard selection, in which the auditor selects the sample without following a structured technique. Although no structured technique is used, the auditor would nonetheless avoid any conscious bias or predictability (for example, avoiding difficult to locate items, or always choosing or avoiding the first or last entries on a page) and thus attempt to ensure that all items in the population have a chance of selection. Haphazard selection is not appropriate when using statistical sampling.

(e) Block selection involves selection of a block(s) of contiguous items from within the population. Block selection cannot ordinarily be used in audit sampling because most populations are structured such that items in a sequence can be expected to have similar characteristics to each other, but different characteristics from items elsewhere in the population. Although in some circumstances it may be an appropriate audit procedure to examine a block of items, it would rarely be an appropriate sample selection technique when the auditor intends to draw valid inferences about the entire population based on the sample.

Q3(a) Describe the principal method of design of the samples and its evaluation.

Page 5.12 of Module

Answer:

Design of the sample and its evaluation - In designing an audit sample, the auditor has to consider the following -

Audit Objectives (Say Valuation of Debtors)

Audit sampling enables the auditor to obtain and evaluate audit evidence about some characteristic of the items selected in order to form or assist in forming a conclusion concerning the population from which the sample is drawn. Audit sampling can be applied using either non-statistical or statistical sampling approaches.

Audit Procedures (Say External Confirmation / Subsequent Recovery / Ledger Scrutiny)

When designing an audit sample, the auditor's consideration includes the specific purpose to be achieved and the combination of audit procedures that is likely to best achieve that purpose.

Nature of Audit Evidence (Say Documentary / Oral) & Nature of Misstatement (Fake Debtors etc)

Consideration of the nature of the audit evidence sought and possible deviation or misstatement conditions or other characteristics relating to that audit evidence will assist the auditor in defining what constitutes a deviation or misstatement and what population to use for sampling. In fulfilling the requirement of paragraph 8 of SA 500 (Revised), when performing audit sampling, the auditor performs audit procedures to obtain evidence that the population from which the audit sample is drawn is complete.

Defining Population (E.g. all debtors having balances or all debtors with zero balance)

The population is the entire set of data from which the auditor wishes to sample in order to reach a conclusion. The auditor determines that the population from which he draws the sample is appropriate for the specific audit objective. For example, if the auditor's objective were to test for overstatement of accounts receivable, his population could be defined as the accounts receivable trial balance. On the other hand, if he was testing for understatement of accounts payable, his population would not be the accounts payable trial balance but could be subsequent disbursements, unfair invoices, unmatched receiving reports(goods sent report from supplier)or other populations that would provide evidence of understatement of accounts payable. The individual items that make up the population are known as sampling units.

Division into Sampling Units

The population can be divided into sampling units in a variety of ways. For example, if the auditor's objective is to test the validity of the entity's accounts receivable, he could define the sampling unit for confirmation purposes as either customer balances or individual customer invoices. The auditor should define the sampling unit in order to obtain an efficient and effective sample to achieve the particular audit objective.

Precautions while defining Population

Further regarding population, it should be noted:

(a) Population, or field or universe (i.e. the total number of items potentially subject toscrutiny within a defined area, must be sufficiently large.(Doesn't make sense in defining 10 items as population)

(b) The system which produces the records to be tested must be sufficiently reliable.

(c) All items within a particular population must be homogeneous, i.e. they must all fall withinthe same category.(Then only we can draw proper conclusion, all debtors should b from same system)

(d) Items within the population must be both (i) identifiable; and (ii) accessible.(Can be distinguished from other and it can be accessed individually, for example items in a bill cannot be defined as population)

Selection Method

Such selection should therefore be entirely random, and for this purpose random number tables are often used. The difficulty often arises, however, that the items within the population are themselves not identifiable in a way which enables such random selection to take place. Petty cash vouchers, for example, are rarely preprinted with a sequential numbering series and randomness will thus have to be ensured in some other way; it will hardly be practical for the auditor himself to set about entering the numbers on the vouchers.

Set Confidence Level

The reliability referred to is usually termed the confidence level. More precisely, in an auditing context, it is the mathematical probability that the mis-statement rate in the sample will not differ from the error rate in the population by more than a stated amount.Confidence level is conveniently expressed as a percentage. Thus, when we speak of confidence level of 90% we mean that there are 90 chances that the item would fall within the confidence intervals of about 90 to 100, against 10 chances, i.e. the risk we take, that it will not (once again, at a specified level of precision). The confidence level is therefore seen to be complementary to risk.

Set Precision

The precision may be defined with which we can describe the attributes of a given population. For example, our sample may be chosen such that the mis-statement in the population can be proved to be within 5 percent of the monetary value. But how precise do we require this percentage to be? The bigger our sample, clearly the more precise we can be, but we can never be completely precise for the same reasons as we can never be 100 percent confident. The degree of precision required will depend on the materiality of the items in question. For example, if Rs3,000 of mis-statement in a sales ledger population of MaterialityRs100,000would be considered to be just not material, then 3 percent would be our precision limits. From this you will deduce that confidence level and precision limits are essentially inter-related, and the two combined would determine the quality of testing. The auditor's assessment of the following factors will primarily be responsible for selecting total limit:

(i) Evaluation of the functioning of the system of internal control in the area under examination.

(ii) Materiality of the amounts involved.

Q3(b) Mr. Ram, a Chartered Accountant has appeared before the Income Tax Authorities as the authorized representative of his client and delivers to the Income Tax Authorities a false declaration. What are the liabilities of Mr. Ram under Income Tax Act, 1961? Page 7.7 of Module

Sections & Rules:- Sec 277 & Rule 12A of Income Tax Act

Content of Section & Rule :-

Answer:

Sec 277.

If a person makes a statement in any verification under this Act or under any rule made thereunder, or delivers an account or statement which is false, and which he either knows or believes to be false, or does not believe to be true, he shall be punishable, -

(i) in a case where the amount of tax, which would have been evaded if the statement or account had been accepted as true, exceeds twenty-five hundred thousand rupees, with rigorous imprisonment for a term which shall not be less than six months but which may extend to seven years and with fine;

(ii) in any other case, with rigorous imprisonment for a term which shall not be less than three months but which may extend to two years and with fine.

Rule 12A

Under Rule 12A of the Income Tax Rules: Under this rule a Chartered Accountant who as an authorised representative has prepared the return filed by the assessed, has to furnish to the Assessing Officer, the particulars of accounts, statements and other documents supplied to him by the assessee for the preparation of the return.

Facts & Discussion

Here Mr Ram chartered Accountant, is authorised representative of assessee .Where the Chartered Accountant has conducted an examination of such records, he has also to submit a report on the scope and results of such examination. The report to be submitted will be a statement within the meaning of Section 277 of the Income Tax Act. Thus if this report contains any information which is false and which the Chartered Accountant either knows or believes to be false or untrue, he would be liable as per section 277.

Mr Ram a chartered accountant has submitted false information as per and he will be liable as per punishments in sec 277 as mentioned above

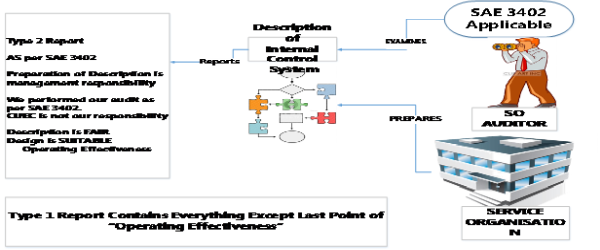

Q3(c) How does an auditor report on the description, design and operating effectiveness of controls at a service organization?

Bare Standards SA 3402

Answer:

It will be as per SAE 3402. 2 types of report are possible type 1 & type 2

The service auditor's opinion, expressed in the positive form, on whether, in all material respects, based on suitable criteria:

(i) In the case of a type 2 report:

a. The description fairly presents the service organization's system that had been designed and implemented throughout the specified period;

b. The controls related to the control objectives stated in the service organization's description of its system were suitably designed throughout the specified period; and

c. The controls tested, which were those necessary to provide reasonable assurance that the control objectives stated in the description were achieved, operated effectively throughout the specified period.

(ii) In the case of a type 1 report:

a. The description fairly presents the service organization's system that had been designed and implemented as at the specified date; and

b. The controls related to the control objectives stated in the service organization's description of its system were suitably designed as at the specified date.

Q3(d) What are the specific matters to be included in auditor's report in an audit of Non-Banking Financial Company (NBFC) not accepting public deposits?

PM Ch14 Q6 / Exam Nov 07

Answer: In the case of all non-banking financial companies:

I. Whether the company is engaged in the business of non-banking financial institution and whether it has obtained a Certificate of Registration (CoR) from the Bank.

II. In the case of a company holding CoR issued by the Bank, whether that company is entitled to continue to hold such CoR in terms of its asset/income pattern as on March 31 of the applicable year.

'Bank' means RBI

In the case of a non-banking financial company not accepting public deposits:

Apart from the aspects enumerated above, the auditor shall include a statement on the following matters, namely: -

(i) Whether the Board of Directors has passed a resolution for non- acceptance of any public deposits;

(ii) Whether the company has accepted any public deposits during the relevant period/year;

(iii) Whether the company has complied with the prudential norms relating to income recognition, accounting standards, asset classification and provisioning for bad and doubtful debts as applicable to it in terms of Non-Banking Financial (Non- Deposit Accepting or Holding) Companies Prudential Norms (Reserve Bank) Directions, 2007.

(iv) In respect of Systemically Important Non-deposit taking NBFCs as defined in paragraph 2(1)(xix) of the Non-Banking Financial (Non- Deposit Accepting or Holding) Companies Prudential Norms (Reserve Bank) Directions, 2007

(a) whether the capital adequacy ratio as disclosed in the return submitted to the Bank in form NBS- 7, has been correctly arrived at and whether such ratio is in compliance with the minimum CRAR prescribed by the Bank;

(b) whether the company has furnished to the Bank the annual statement of capital funds, risk assets/exposures and risk asset ratio (NBS-7) within the stipulated period.

Q4(a) Explain briefly the duties and responsibilities of an auditor in case of material misstatement resulting from management fraud?

PM Ch1 Q30 / PM Ch7 Q3 / RTP Q9(a) Nov15 / RTP Q7(b) May17/ Exam Nov 09

Answer: Source of MMST& What is Fraud?

Misstatement in the financial statements can arise from fraud or error.

The term fraud refers to an 'Intentional Act' by one or more individuals among management, those charged with governance, employees, or third parties, involving the use of deception to obtain an unjust or illegal advantage.

Primary Responsibility

As per SA 240 'The Auditor's Responsibilities Relating to Fraud in an Audit of Financial Statements', the primary responsibility for the prevention and detection of fraud rests with both those charged with governance of the entity and management.

Auditor Responsibility about Fraud

The auditor, conducting an audit, is responsible for obtaining reasonable assurance that the financial statements taken as a whole are free from material misstatement, whether caused by fraud or error. Owing to the inherent limitations of an audit, there is an unavoidable risk that some material misstatements of the financial statements may not be detected, even though the audit is properly planned and performed in accordance with the SAs.

Detecting Error Vs Detecting Fraud

As described in SA 200, the potential effects of inherent limitations are particularly significant in the case of misstatement resulting from fraud. The risk of not detecting a material misstatement resulting from fraud is higher than the risk of not detecting one resulting from error. This is because fraud may involve sophisticated and carefully organized schemes designed to conceal it, such as forgery, deliberate failure to record transactions, or intentional misrepresentations being made to the auditor. Such attempts at concealment may be even more difficult to detect when accompanied by collusion. Collusion may cause the auditor to believe that audit evidence is persuasive when it is, in fact, false. While the auditor may be able to identify potential opportunities for fraud to be perpetrated, it is difficult for the auditor to determine whether misstatements in judgment areas such as accounting estimates are caused by fraud or error.

Management Fraud Vs Employee Fraud

Furthermore, the risk of the auditor not detecting a material misstatement resulting from management fraud is greater than for employee fraud, because management is frequently in a position to directly or indirectly manipulate accounting records, present fraudulent financial information or override control procedures designed to prevent similar frauds by other employees.

Professional Skepticism

When obtaining reasonable assurance, the auditor is responsible for maintaining professional skepticism throughout the audit, considering the potential for management override of controls and recognizing the fact that audit procedures that are effective for detecting error may not be effective in detecting fraud.

Sec 143(12)

Additionally, as per section 143(12) of the Companies Act, 2013, if an auditor of a company, inthe course of the performance of his duties as auditor, has reason to believe that an offenceinvolving fraud is being or has been committed against the company by officers or employees of the company, he shall immediately report the matter to the Central Government within60 days of his knowledge and after following the prescribed procedure.

CARO

The auditor is also required to report as per Clause (x) of Paragraph 3 of CARO, 2016,if there is any fraud on or by the company by officers or employees has been noticed or reported during the year. The nature and the amount involved are to be indicated.

Q4(b) What is included in an Auditors' Responsibility paragraph?

Module Page 8.3

Answer:

Auditor's Responsibility: The auditor's report shall include a section with the heading Auditor's Responsibility.

Objective

The auditor's report shall state that the responsibility of the auditor is to express an opinion on the financial statements based on the audit.

Scope of Audit

The auditor's report shall state that the audit was conducted in accordance with Standards on Auditing issued by the Institute of Chartered Accountants of India. The auditor's report shall also explain that those Standards require that the auditor comply with ethical requirements and that the auditor plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

Elaborate Scope

The auditor's report shall describe an audit by stating that:

(a) An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements;

(b) The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control.

In circumstances when the auditor also has a responsibility to express an opinion on the effectiveness of internal control in conjunction with the audit of the financial statements, the auditor shall omit the phrase that the auditor's consideration of internal control is not for the purpose of expressing an opinion on the effectiveness of internal control; and

(c) An audit also includes evaluating the appropriateness of the accounting policies used and the reasonableness of accounting estimates made by management, as well as the overall presentation of the financial statements.

Where the financial statements are prepared in accordance with a fair presentation framework, the description of the audit in the auditor's report shall refer to ―the entity's preparation and fair presentation of the financial statements - or the entity's preparation of financial statements that give a true and fair view, as appropriate in the circumstances.

Result: The auditor's report shall state whether the auditor believes that the audit evidence the auditor has obtained is sufficient and appropriate to provide a basis for the auditor's opinion.

Q4(c) What are the main phases in the conduct of Risk Based Audit.

RTP Q6 (OLD) / RTP Q20(c) May 15 / Exam May 16

Answer:

General Steps in the Conduct of RBA - RBA consists of four main phases starting with the identification and prioritization of risks, to the determination of residual risk, reduction of residual risk to acceptable level and the reporting to auditee of audit results. These are achieved through the following:

- Understand auditee operations to identify and prioritize risks(Inherent Risk)

- Assess auditee management strategies and controls to determine residual audit risk(Control Risk)

- Manage residual risk to reduce it to acceptable level(RMM perform extensive audit procedures)

- Inform auditee of audit results through appropriate report

Understanding auditee operations involves processes for reviewing and understanding the audited organizations risk management processes for its strategies, framework of operations, operational performance and information process framework, in order to identify and prioritize the error and fraud risks that impact the audit of financial statements.

(Changes in environment)

The environment in which the auditee operates, the information required to monitor changes in the environment, and the process or activities integral to the audited entity's success in meeting its objectives are the key factors to an understanding of agency risks. Likewise, a performance review of the audited entity's delivery of service by comparing expectations against actual results may also aid in understanding agency operations.

Assessment of management risk strategies and controls is the determination as to how controls within the auditee are designed. The role of internal audit in promoting a sound accounting system and internal control is recognized, thus the statutory auditor should evaluate the effectiveness of internal audit to determine the extent to which reliance can be placed upon it in the conduct of substantive tests.

Management of residual risk requires the design and execution of a risk reduction approach that is efficient and effective to bring down residual audit risk to an acceptable level. This includes the design and execution of necessary audit procedures and substantive testing to obtain evidence in support of transactions and balances. More resources should be allocated to areas of high audit risks, which were earlier known through the analytical procedures undertaken.

The results of audit shall be communicated by the auditor to the audited entity. The auditor must immediately communicate to the auditee reportable conditions that have been observed even before completion of the audit, such as weaknesses in the internal control system, deficiencies in the design and operation of internal controls that affect the organization's ability to record, process, summarize and report financial data.

Q5(a) You have been appointed as an energy auditor of Sunlight Energy Ltd. what are the key functions you would carry out?

PM Ch17 Q1 /RTP Q14(OLD)/ RTP Q16(a) May17/ RTP 20(b) May16 / Exam Nov 11, May 07, May 04

Answer:

Key functions of Energy Auditor:

What is Energy Audit?

Energy auditing is defined as an activity that serves the purposes of assessing energy use pattern of a factory or energy consuming equipment and identifying energy saving opportunities.

In that context, energy management involves the basis approaches reducing avoidable losses, improving the effectiveness of energy use, and increasing energy use efficiency.

The function of an energy auditor could be compared with that of a financial auditor. The energy auditor is normally expected to give recommendations on efficiency improvements leading to monetary benefits and also advise on energy management issues. Generally, energy auditor for the industry is an external party.

Key Functions of Energy Auditor

The following are some of the key functions of the energy auditor:

Conduct preliminary and detailed energy audits which should include the following:

(i) Quantify energy costs and quantities.

(ii) Devise energy database formats to ensure they depict the correct picture � by product, department, consumer, etc.

(iii) Data collection and analysis.

(iv) Measurements, mass and energy balances.

(v) Correlate trends of production or activity to energy costs.

(vi) Highlight areas that need attention for detailed investigations.

(vii) Identification of energy efficiency projects and techno-economic evaluation.

(viii) Reviewing energy procurement practices.

(ix) Advise and check the compliance of the organization for policy and regulation aspects.

(x) Establishing action plan including energy saving targets, staffing requirements, implementation time requirements, procurement issues, details and cost estimates.

(xi) Recommendations on goal setting for energy saving, record keeping, reporting and energy accounting, organization requirements, communications and public relations.

Q5(b) What is tolerable misstatement and tolerable rate of deviation?

RTP Q7(e) May 14 / Exam May 14

Answer:

Tolerable misstatement - A monetary amount set by the auditor in respect of which the auditor seeks to obtain an appropriate level of assurance that the monetary amount set by the auditor is not exceeded by the actual misstatement in the population.

When designing a sample, the auditor determines tolerable misstatement in order to address the risk that the aggregate of individually immaterial misstatements may cause the financial statements to be materially misstated and provide a margin for possible undetected misstatements. Tolerable misstatement is the application of performance materiality, as defined in SA 320 (Revised), to a particular sampling procedure. Tolerable misstatement may be the same amount or an amount lower than performance materiality.

Tolerable rate of deviation is a rate of deviation from prescribed internal control procedures set by the auditor in respect of which the auditor seeks to obtain an appropriate level of assurance that the rate of deviation set by the auditor is not exceeded by the actual rate of deviation in the population.

Q5(c) M/s. SB & Co. has been appointed as tax auditor under section 44 AB of lncome Tax Act, 1961 by Woodcraft Interior Consultants, a professional partnership firm, having turnover 1.25 Crores. M/s. RS & Co. are the statutory auditors of the firm but they are unable to give their report on the financial statements of the firm. M/s. SB & Co., have, however, completed their tax audit and want to issue their reports. comment.

Module Page 15.11

Answer:

A question may arise in the case where the statutory auditor has not been appointed by the authorities concerned as to where the tax auditor appointed under section 44AB can complete his audit without waiting for statutory audit report on the accounts audited by the statutory auditors.

It may be noted that Form No. 3CA requires the tax auditor to enclose a copy of the audit report conducted by the statutory auditor or the auditor of the financial statements as the case may be. Where a statutory auditor has not been appointed by the authorities concerned or where the report of the statutory auditor is not available for whatever reasons, it will be possible for the tax auditor to give his report in Form No. 3CB and to certify the relevant particulars in Form No.3CD. This is particularly important in those cases where the assessee concerned has suffered losses in the relevant accounting year. It may, however, be noted that the tax auditor in such cases will have to conduct the financial audit as well in order to enable him to certify whether or not the accounts reported upon by him give a true and fair view of the state of affairs of the assessee whose accounts are audited by him under section 44AB.

Q5(d) ABC Ltd. owns a piece of Land and Building situated at IP road, Mumbai which was purchased before 30 years. The title deeds for the same are deposited with State Bank of India for obtaining credit facilities by the company. As the statutory auditor of the company for the year ended 31'st March, 2017, what are the audit procedures to be followed and what is the reporting under CARO 20L6 ?

Similar RTP Q8(b)(ii) May17

Answer:

Title deeds of Immovable Property in the name of Director: As per Clause (i)(c) of Paragraph 3 of the CARO, 2016, the auditor is required to report on whether the title deeds of immovable properties are held in the name of the company. If not, provide the details thereof.

The auditor should verify the title deeds available and reconcile the same with the fixed assets register. The scrutiny of the title deeds of the immovable property may reveal a number of discrepancies between the details in the fixed assets register and the details available in the title deeds. This may be due to various reasons which needs to be examined.

If title deeds are with third party, auditor should think whether it is nor mal practice not to have title deeds with client, should ask for external; confirmation from SBI.

If sufficient and appropriate evidence is received regarding title deeds auditor should make positive comment.

But if evidence is not obtained auditor will have to give negative comment. As given below.

Thus, the auditor shall report on the same under Clause (i)(c) of Paragraph 3 of the CARO, 2016.

Auditor should comment on non-availability of evidence to comment on this point.

Q6(a) Mr. M, a Chartered Accountant in practice, has printed visiting cards which besides other details also carries a Quick Response (QR) code. The visiting card as well the QR code contains his name, office and residential address, contact details, e-mail id and name of the firm's website. comment with reference to the chartered Accountants Act, 1949 and schedules thereto.

Module Page 22.32

Answer: Sch 1 Part1 Clause 7

Further via a clarification on -

Whether the Chartered Accountants in practice can print their photograph on their visiting cards?,

The Committee on Ethical Standards (CES) of the Institute has opinioned that mostly the business class prints the photograph on their visiting cards for promoting their business and soliciting clients. As such, it is not permissible for the chartered accountants in practice to print their photograph on their visiting cards.

However, a member in practice is allowed to print Quick Response Code (QR Code) on the visiting Card, provided that the Code does not contain information that is not otherwise permissible to be printed on a visiting Card.

Note : QR is Quick Response Code allowed on visiting card of practicing CA. It is a black berry like code, once you scan information in visiting card gets saved automatically in mobile phone. As per ICAI clarification such quick response code is allowed provided only that information should get saved which is allowed on visiting card. Module has included this explanation below Sch 1 Part 1 Clause 7. Students could have explained clause 6 as well. Further some students thought that he is promoting his website, this is not correct, writing name of website on visiting card is allowed, writing please visit website is not allowed. Which was not the case here.

Q6(b) L, a chartered accountant prepares and certifies projected financial statements of his client Abacus Ltd. Abacus Ltd. forwarded the same to their banks to secure some loans and bank, on that basis sanctioned a loan' comment with reference to the chartered Accountants Act, 1949 and schedules thereto.

PM Ch22 Q3(d) / RTP Q19(c) May16 / Exam May14 /May 08

Answer: Certification of Financial Forecast: As per Clause (3) of Part I of Second Schedule to the Chartered Accountants Act, 1949, a chartered accountant in practice is deemed to be guilty of professional misconduct if he permits his name or the name of his firm to be used in connection with an estimate of earnings contingent upon future transactions in a manner which may lead to the belief that he vouches for the accuracy of the forecast.

Further, SAE 3400 'The Examination of Prospective Financial Information', provides that the management is responsible for the preparation and presentation of the prospective financial information, including the identification and disclosure of the sources of information, the basis of forecasts and the underlying assumptions. The auditor may be asked to examine and report on the prospective financial information to enhance its credibility, whether it is intended for use by third parties or for internal purposes. Thus, while making report on projection, the auditor need to mention that his responsibility is to examine the evidence supporting the assumptions and other information in the prospective financial information, his responsibility does not include verification of the accuracy of the projections, therefore, he does not vouch for the accuracy of the same.

In the instant case, Mr. L after having prepared the projections stated in his report certified projected financial statements, that means he vouched for accuracy and appropriateness of projected financial statements hence he will be guilty of professional misconduct.

Q6(c) X, a chartered accountant in practice, in spite of several reminders from the secretary of the Institute of chartered Accountants of India fails to submit Form 18. Is he liable for misconduct ?

PM Ch22 Q23(d) / Exam May 10

Answer.

Failed to Supply Information Called For: As per Clause (2) of Part III of the First Schedule to the Chartered Accountants Act, 1949, a member, whether in practice or not, will be deemed to be guilty of professional misconduct if he does not supply the information called for, or does not comply with the requirements asked for, by the Institute, Council or any of its Committees, Director (Discipline), Board of Discipline, Disciplinary Committee, Quality Review Board or the Appellate authority.

Thus, in the given case, Mr. X has failed to reply to the letters of the Institute asking him to confirm the date of leaving the service as a paid assistant. Therefore, he is held guilty of professional misconduct as per Clause (2) of Part III of the First Schedule to the Chartered Accountants Act, 1949.

Q6(d) P' a chartered Accountant holding certificate of practice, is a leading Income Tax practitioner in Gurugram. He is also trading in derivatives. comment with reference to the chartered Accountant Act, 1949 and schedules thereto.

PM Ch22 Q15/ RTP Q19(a)(ii) Nov 11/ Exam Nov 08

Answer:

Engaging into Business/Profession Other Than the Profession of CA: As per Clause (11) of Part I of First Schedule to the Chartered Accountants Act, 1949 (hereinafter referred as 'Act'), a Chartered Accountant is deemed to be guilty of professional misconduct if he 'engages in any business or occupation other than the profession of Chartered Accountant unless permitted by the Council so to engage'.

However, the Council has granted general permission to the members to engage in 12 specific occupation. In respect of all other occupations specific permission of the Institute is necessary.

In this case, CA. P is engaged in the occupation of trading in derivatives which is not covered under the general permission.

Hence specific permission of the Institute has to be obtained otherwise he will be deemed to be guilty of professional misconduct under Clause (11) of Part I of First Schedule of the Act.

Q7(a) Auditor's right to Lien as per Companies Act, 2013.

Module Page 6.24

Answer: Right to Lien- In terms of the general principles of law, any person having the lawful possession of somebody else's property, on which he has worked, may retain the property for non-payment of his dues on account of the work done on the property. On this premise, auditor can exercise lien on books and documents placed at his possession by the client for non-payment of fees, for work done on the books and documents. The Institute of Chartered Accountants in England and Wales has expressed a similar view on the following conditions:

(i) Documents retained must belong to the client who owes the money.

(ii) Documents must have come into possession of the auditor on the authority of the client. They must not have been received through irregular or illegal means. In case of a company client, they must be received on the authority of the Board of Directors.

(iii) The auditor can retain the documents only if he has done work on the documents assigned to him.

(iv) Such of the documents can be retained which are connected with the work on which fees have not been paid.

Under section 128 of the Act, books of account of a company must be kept at the registered office. These provisions ordinarily make it impracticable for the auditor to have possession of the books and documents. The company provides reasonable facility to auditor for inspection of the books of account by directors and others authorized to inspect under the Act. Taking an overall view of the matter, it seems that though legally, auditor may exercise right of lien in cases of companies, it is mostly impracticable for legal and practicable constraints. His working papers being his own property, the question of lien, on them does not arise.

SA 230 issued by ICAI on Audit Documentation (explanatory text, A- 25), 'Standard on Quality Control (SQC) 1, Quality Control for Firms that Perform Audits and Reviews of Historical Financial Information, and Other Assurance and Related Services Engagements -, issued by the Institute, provides that, unless otherwise specified by law or regulation, audit documentation is the property of the auditor. He may at his discretion, make portions of, or extracts from, audit documentation available to clients, provided such disclosure does not undermine the validity of the work performed, or, in the case of assurance engagements, the independence of the auditor or of his personnel.

Q7(b) Proper books of accounts as per Companies Act, 2013.

PM Ch6 Q31 / Exam May 05, May 15

Answer: Proper Books of Account Not Maintained:

Sec 128: Section 128(1) of the Companies Act, 2013 requires that every company shall prepare and keep at its registered office books of account and other relevant books and papers and financial statement for every financial year which give a true and fair view of the state of the affairs of the company, including that of its branch office or offices, if any, and explain the transactions effected both at the registered office and its branches and such books shall be kept on accrual basis and according to the double entry system of accounting.

The provisions mentioned above are required to be followed by the company to maintain proper books of accounts. The Auditor is required to check that the company has complied with all the provisions related to maintenance of books of accounts etc.

Further, the books have to be maintained under accrual system and if the statutory auditor finds the books are not maintained accordingly, he will have to modify his report.

Sec 143: According to Section 143(3)(b), the auditor's report shall also state whether, in his opinion, proper books of account as required by law have been kept by the company so far as appears from his examination of those books and proper returns adequate for the purposes of his audit have been received from branches not visited by him.

If answer is in negative or with qualification, the report shall state the reasons therefore.

Q7(c) Differentiate between audit report and audit certificate.

Answer: A certificate is a written confirmation of the accuracy of the facts stated therein and does not involve any estimate or opinion. The term 'certificate' is, therefore, used where the auditor verifies the accuracy of facts. An auditor may thus, certify the circulation figures of a newspaper or the value of imports or exports of a company. An auditor's certificate represents that he has verified certain figures and is in a position to vouch safe their accuracy as per his examination of documents and books of account.

A report, on the other hand, is a formal statement usually made after an enquiry, examination or reviews of specified matters under report and includes the reporting auditor's opinion thereon. Thus, when a reporting auditor issues a certificate, he is responsible for the factual accuracy of what is stated therein.

On the other hand, when a reporting auditor gives a report, he is responsible for ensuring that the report is based on factual data, that his opinion is in due accordance with facts, and that it is arrived at by the application of due care and skill. The 'report' involves expression of opinion which may differ from one professional to another.

There is no question of exactitude in case of a report since the information contained therein is based on estimates and involves judgement element.

Q7(d) 'Inquiry' as one of the methods of collecting audit evidence.

PM Ch5 Q7(b)

Answer: Definition: Inquiry consists of seeking information of knowledgeable persons, both financial and non- financial, within the entity or outside the entity.

Written or Oral: Inquiry is used extensively throughout the audit in addition to other audit procedures. Inquiries may range from formal written inquiries to informal oral inquiries.

Responses: Evaluating responses to inquiries is an integral part of the inquiry process. Responses to inquiries may provide the auditor with information not previously possessed or with corroborative audit evidence. Alternatively, responses might provide information that differs significantly from other information that the auditor has obtained, for example, information regarding the possibility of management override of controls. In some cases, responses to inquiries provide a basis for the auditor to modify or perform additional audit procedures.

Evidence about Management's Intent: Although corroboration of evidence obtained through inquiry is often of particular importance, in the case of inquiries about management intent, the information available to support management's intent may be limited. In these cases, understanding management's past history of carrying out its stated intentions, management's stated reasons for choosing a particular course of action, and management's ability to pursue a specific course of action may provide relevant information to corroborate the evidence obtained through inquiry. In respect of some matters, the auditor may consider it necessary to obtain written representations from management and, where appropriate, those charged with governance to confirm responses to oral inquiries.

Q7(e) Verification of payment of remuneration to an insurance agent.

Ch12 Q15 / RTP Q13 Nov 15

Answer: Commission Paid to Insurance Agents:

Role of Agents: It is a well-known fact that insurance business is solicited by insurance agents. The remuneration of an agent is paid by way of commission which is calculated by applying a percentage to the premium collected by him. Commission is payable to the agents for the business procured through them and is debited to Commission on Direct Business Account. There is a separate head for commission on reinsurance accepted which usually arise in case of Head Office.

Condition before paying commission:

It may be noted that under section 40 of Insurance Act, 1938, no commission can be paid to a person who is not an agent or intermediary of the insurance company.

The auditor should, inter alia, do the following for verification of commission-

(i) Vouch disbursement entries with reference to the disbursement vouchers with copies of commission bills and commission statements.

(ii) Check whether the vouchers are authorized by the officers-in–charge as per rules in force and income tax is deducted at source, as applicable.

(iii) Test check correctness of amounts of commission allowed.

(iv) Scrutinize agents' ledger and the balances, examine accounts having debit balances, if any, and obtain information on the same. Necessary rectification of accounts and other remedial actions have to be considered.

(v) Check whether commission outgo for the period under audit been duly accounted.

To view the question paper on Advanced Auditing (CA Final) : Click Here

To enrol Advanced Auditing (CA Final) subject of the author : Click Here

CAclubindia

CAclubindia