APPLICABILITY:

With the introduction of the negative list concept since July, 2012, the scope of applicability of Service tax has increased manifold. Today, there is Service tax implication on almost every sector, and real estate is no exception.

A summarised analysis is contained herein providing guidance on the implication of Service tax on various forms of real estate transactions.

Service tax is leviable only on the taxable services provided in the taxable territory and hence the services provided outside the taxable territory would be out of the service tax net. At present, the service tax levy extends to whole of India except the state of Jammu and Kashmir.

RATE:

The present rate of Service Tax is 12.36%, consisting of Service Tax 12%, Education Cess 2% and Secondary Education Cess 1% thereon. However in certain cases abatements are available as mentioned here-in-after.

WHAT IS SERVICE?

‘Service’ means –

• any activity

• carried out by a person for another

• for consideration

• and includes a declared service.

However ‘Service’ does not include an activity that constitutes merely–

• transfer of title in goods or immovable property by way of sale, gift or in any other manner

• transfer, delivery or supply of goods which is deemed to be a sale of goods within the meaning of clause (29A) of article 366 of the Constitution

• transaction in money or actionable claim

• service provided by an employee to an employer in the course of the employment.

• fees taken in any court or a tribunal set up under a law for the time being in force

In the present Service tax regime, all services other than the services specified in the negative list are taxable. However, specific exemptions are available to certain services as listed in the Mega Exemption Notification.

SERVICES:

Some of the services which are commonly prevalent in the Real estate sector are discussed below:

1. RENTING OF IMMOVABLE PROPERTY

2. CONSTRUCTION SERVICES

• CONSTRUCTION OF RESIDENTIAL COMPLEX

• COMMERCIAL OR INDUSTRIAL CONSTRUCTION

• SPECIAL SERVICES BY BUILDERS

3. WORKS CONTRACT

4. MAINTENANCE/ MANAGEMENT OF IMMOVABLE PROPERTY

5. SERVICES UNDER REVERSE CHARGE MECHANISM (LIABILITY AS SERVICE RECIPIENT)

6. RENTING OF IMMOVABLE PROPERTY:

“Renting” means ‘‘allowing, permitting or granting access, entry, occupation, usage or any such facility, wholly or partly, in an immovable property, with or without the transfer of possession or control of the said immovable property and includes letting, leasing, licensing or other similar arrangements in respect of immovable property’.

EXEMPTED/ NON-TAXABLE SERVICES

• Renting of vacant land, with or without a structure incidental to its use, relating to agriculture.

• Renting of residential dwelling for use as residence.

• Renting out of any property by the Reserve Bank of India

• Renting out of any property by a Government or a local authority to a non-business entity.

• Renting of precincts of a religious place meant for general public.

• Renting of a hotel, inn, guest house, club, campsite or other commercial places meant for residential or lodging purposes, having declared tariff of a room below rupees one thousand per day or equivalent.

• Renting of immovable property to an educational institution in relation to education exempted from service tax

ABATEMENTS

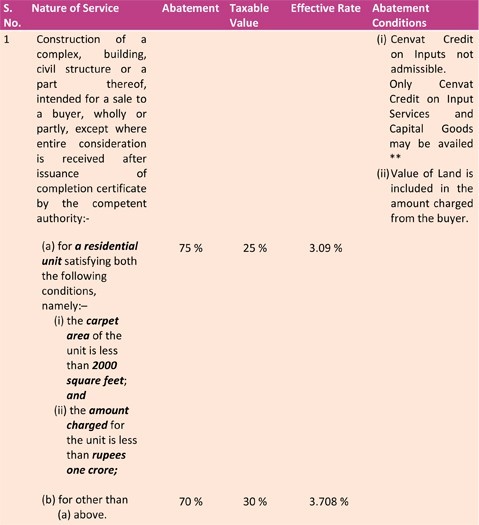

CONSTRUCTION SERVICES:

Construction services have been specifically defined as declared service to mean construction of a complex, building, civil structure or part thereof intended for sale to a buyer where any part of the consideration is received from the buyer before the issuance of completion certificate by the competent authority. In cases where the entire consideration is received from the buyer after issuance of completion certificate, no service tax is required to be paid on the same.

Completion certificate is issued by any authority authorized to issue completion certificate under any law. In case of non requirement of such certificate from such authority, the Completion certificate can be obtained from a registered architect or chartered engineer or licensed surveyor.

Construction includes additions, alterations, replacements or remodeling of any existing civil structure.

EXEMPTED/ NON-TAXABLE SERVICES

• Services provided to the Government or local authorities by way of construction, erection, commissioning, installation, completion, fitting out, repair, maintenance, renovation or alteration of:-

(a) a civil structure or other original works meant predominantly for use other than commerce, industry, or other business or profession.

(b) a historical monument, archaeological site or remains of national importance, archaeological excavation, or antiquity specified under the Ancient Monuments and Archaeological Sites and Remains Act, 1958 (24 of 1958);

(c) a structure meant predominantly for use as an educational, clinical, art or cultural establishment;

(d) canal, dam or other irrigation works;

(e) pipeline, conduit or plant for water supply, water treatment, sewerage treatment or disposal;

(f) a residential complex predominantly meant for self-use or the use of their employees or other persons like Members of Parliament, Members of State Legislative, Members of Panchayats, Members of Municipalities and Members of other local authorities, etc.

• Services provided by way of construction, erection, commissioning, installation, completion, fitting out, repair, maintenance, renovation or alteration of:-

(a) a road, bridge, tunnel, or terminal for road transportation for use by general public;

(b) a civil structure or other original works pertaining to a scheme under Jawaharlal Nehru National Urban Renewal Mission or Rajiv Awaas Yojana;

(c) a building owned by a Charitable entity registered under Section 12 AA of the Income tax Act, 1961(43 of 1961) and meant predominantly for religious use by general public.

(d) a pollution control or effluent treatment plant, except located as a part of a factory or

(e) structure meant for funeral, burial or cremation of deceased.

• Services by way of construction, erection, commissioning or installation of original works pertaining to:-

(a) an airport, port or railways;

(b) a single residential unit otherwise than as a part of a residential complex.

(c) low- cost houses up to a carpet area of 60 square metres per house in a housing project approved by competent authority empowered under the ‘Scheme of Affordable Housing in Partnership’ framed by the Ministry of Housing and Urban Poverty Alleviation, Government of India.

(d) post- harvest storage infrastructure for agricultural produce including a cold storages for such purposes or

(e) mechanised food grain handling system, machinery or equipment for units processing agricultural produce as food stuff excluding alcoholic beverages.

ABATEMENTS

SPECIAL SERVICES BY BUILDERS

Amounts received from the buyers for preferential location, other extra charges, etc. are taxable as Special Services by Builders. Service Tax needs to be paid at full rate of 12.36% as no abatement is available on such amounts.

REAL ESTATE ARRANGEMENTS

Across the country, divergent business models and practices are being followed in the real estate sector. Some of these business models and service tax applicability on these models are discussed as below:

JOINT DEVELOPMENT MODEL (AREA SHARING/ ALLOCATION)

Parties in the model:

(i) landowner;

(ii) builder/ developer

In these kinds of Joint Ventures, total saleable area of the project is shared between Landowner and Developer, and each party is entitled to sell his allocated area/unit to the buyers.

Taxability Landowner –

(a) sale of land by the landowner - not a taxable service;

(b) sale of landowner’s share of flats/units by him to buyers, where any part of consideration is received by him before issuance of completion certificate - is a taxable service.

Developer –

(a) flats/units agreed to be given by builder/developer to the land owner towards the land /development rights - is a taxable service.

(b) sale of flats/units to buyers, where any part of consideration is received before issuance of completion certificate - is a taxable service.

The builder/developer receives consideration for the construction service provided by him, from two categories of service receivers:

(a) from landowner: in the form of land/development rights; and

(b) from other buyers: normally in cash/ cash equivalents.

Construction service provided by the builder/developer is taxable in case any part of the payment/development rights of the land was received by the builder/ developer before the issuance of completion certificate and the service tax would be required to be paid by builder/developers for the flats given to the land owner.

However, Service tax is liable to be paid by the builder/developer on the ‘construction service’ involved in the flats to be given to the land owner, at the time when the possession or right in the property of the said flats are transferred to the land owner by entering into a conveyance deed or similar instrument.

JOINT DEVELOPMENT MODEL (REVENUE SHARING)

Parties in the model:

(i) landowner;

(ii) builder/ developer

In this kind of model, land owner and builder/developer join hands and may either create a new entity or otherwise operate as an unincorporated association, on partnership /joint / collaboration basis, with mutuality of interest and to share common risk/profit together. The new entity undertakes construction on behalf of landowner and builder/developer.

In these kinds of Joint Ventures, total revenue/ profit of the project is shared between Landowner and Developer, and each party is entitled to receive sale proceeds/ profit of the project.

Taxability - Sale of flats/units by the new entity/ all parties (if operating as an unincorporated association) to buyers, where any part of consideration is received by them before issuance of completion certificate - is a taxable service.

However in case of an unincorporated association, depending on the facts and circumstances, there might be tax implications between land owner and developer also, as an unincorporated association and its members are treated as distinct persons for the purpose of service tax

INVESTMENT MODEL: In this model, before the commencement of the project, the same is on offer to investors. Either a specified area/ flats are earmarked/ allotted to the investors. Additionally the investor may also be promised a fixed rate of interest. After a certain specified period an investor has the option either to exit from the project on receipt of the amount invested along with interest or he can nominate/ re-sell the said allotment to another buyer or retain the flat for his own use.

Taxability - Investment amount shall be treated as consideration paid in advance for the construction service to be provided by the builder/developer to the investor and the said amount would be subject to service tax. If the investor decides to exit from the project at a later date, either before or after the issuance of completion certificate, the builder/developer would be entitled to take service tax credit (to the extent he has refunded the original amount). If the builder/developer resells the flat before the issuance of completion certificate, again tax liability would arise.

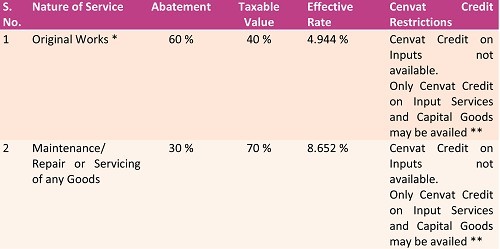

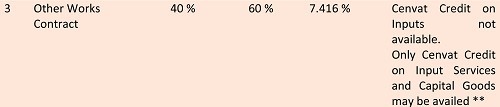

WORKS CONTRACT SERVICE:

“Works Contract" means a contract wherein transfer of property in goods involved in the execution of such contract is leviable to tax as sale of goods and such contract is for the purpose of carrying out construction, erection, commissioning, installation, completion, fitting out, repair, maintenance, renovation, alteration of any movable or immovable property or for carrying out any other similar activity or a part thereof in relation to such property;

EXEMPTIONS AVAILABLE – Please refer to the Exemptions mentioned for Construction services above.

VALUATION OF WORKS CONTRACT SERVICES:

VALUATION ON ACTUAL BASIS:

Works contract service= Gross amount charged for works contract-value of property in goods transferred in the execution of such works contract

Although value of service in the works contract has to be calculated after deducting value of property in goods from the gross consideration but the following would be included in the Value of works contract service -

(i) labour charges for execution of the works;

(ii) amount paid to a sub-contractor for labour and services;

(iii) charges for planning, designing and architect's fees;

(iv) charges for obtaining on hire or otherwise, machinery and tools used for the execution of the works contract;

(v) cost of consumables such as water, electricity, fuel used in the execution of the works contract;

(vi) cost of establishment of the contractor relatable to supply of labour and services;

(vii) other similar expenses relatable to supply of labour and services; and

(viii) profit earned by the service provider relatable to supply of labour and services;

Taxability – Service Tax is payable at the rate of 12.36% on the value determined as aforesaid.

ALTERNATE METHOD for determination of service tax payable on the service portion in a works contract (similar to erstwhile Composition scheme):

*Original works means:

(i) all new constructions;

(ii) all types of additions and alterations to abandoned or damaged structures on land that are required to make them workable;

(iii) erection, commissioning or installation of plant, machinery or equipment or structures, whether pre-fabricated or otherwise;

MAINTENANCE/ MANAGEMENT OF IMMOVABLE PROPERTIES

Maintenance or Management charges are collected by the Builders/ Developers from the buyers/customers for providing common maintenance of the residential/ commercial complex, shopping malls, etc. These services are liable to be taxed at 12.36 %.

GENERAL THRESHOLD EXEMPTION

Turnover based exemption is available to all persons (service providers) for an amount of taxable services provided up to Rs.10 lacs during a financial year, provided the total amount of taxable services provided during the year preceeding the relevant financial year does not exceed Rs.10 lacs.

However, Service tax registration needs to be obtained once the taxable service provided exceeds Rs.9 lacs during a financial year.

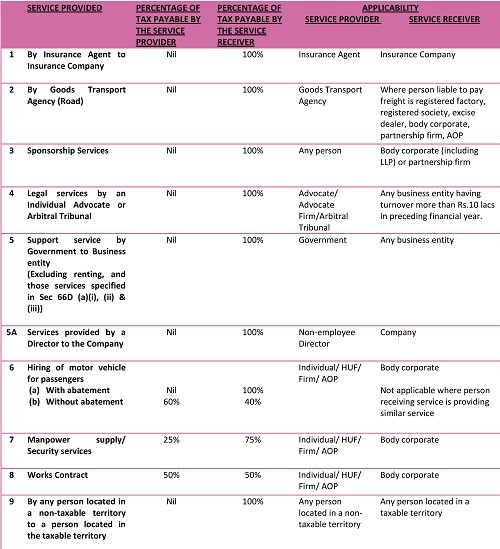

REVERSE CHARGE MECHANISM:

With effect from 1st July, 2012, the reverse charge mechanism of taxation has been introduced whereby in case of certain specified services, the liability to pay service tax has been imposed on both service provider and service receiver in the mentioned proportion. The specified list of services and the liability to pay tax are given below:

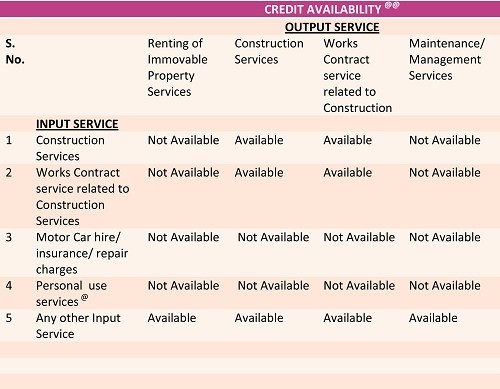

CENVAT CREDIT:

Cenvat Credit is normally available on Inputs, Capital Goods and Input Services. In this write-up, we have focused on rules relating to Cenvat Credit available on Input services in connection with real estate activities.

“Input Service” means any service used by a provider of taxable service for providing an output service.

Cenvat Credit may be availed on the input services as mentioned below:

@ Cenvat Credit cannot be availed on the following input services:

Outdoor Catering, Beauty Treatment, Health Service, Cosmetic/Plastic surgery, Membership of a club, health and fitness centre, Life insurance, Health insurance and Travel benefits, when such services are used primarily for personal use or consumption of any employee.

@@ Following basic conditions need to be fulfilled to avail Cenvat Credit on Input Services:

• Input service must be used for providing taxable output service.

• Credit can be availed on the basis of a valid invoice/ bill or challan issued by the service provider.

• In case where the service tax is paid under Reverse charge mechanism as a service recipient, the credit of the same shall be allowed on the basis of payment challan.

Provided the payment of the value of input service and the service tax paid or payable as indicated in the invoice/bill/challan is not made within 3 months of the date of the invoice/bill/challan, the service provider shall pay an amount equal to the CENVAT credit taken on such input service.

• The supporting invoice/bill must contain the following particulars:

a) Details of duty or service tax payable

b) Description of goods or taxable services

c) Assessable Value

d) Central Excise or Service Tax Registration number.

e) Name and address of the premises.

• Separate records needs to be maintained in respect of the input services utilized in both taxable and exempted services. However if no separate records are maintained, the service provider has an option to pay an amount equal to 6% of the value of the exempted services.

• Certain other conditions also needs to be followed as per Cenvat Credit Rules, 2004 such as reversal of credit in case of service provider providing exempted services also, maintenance of cenvat credit records, etc.

Disclaimer:

Statements and opinions expressed in write-up herein are our personal views based on the current service tax law. While every care has been taken in the compilation of this information and every attempt made to present up-to-date and accurate information, we cannot guarantee that inaccuracies will not occur. We will not be held responsible for any claim, loss, damage or inconvenience caused as a result of any information within this write-up or any information accessed herein.

By: Vikash Parakh, FCA

CAclubindia

CAclubindia