SERVICE TAX

Cenvat For Automobile Dealers

Brief Introduction

Automobile Dealers are normally engaged in Selling of Vehicles, Selling of Spare parts of vehicle, and working as an Authorized Service Station on behalf of the principal. In the course of selling the cars they do provide a lot of Business Auxiliary Services to other business entities (Insurance & Finance Business Companies as the also provide business to these companies)

Type of Services Rendered:

Taxable:

- Authorized Service Station (Servicing of Vehicle is done)

- Rent a cab

- Business Auxiliary Services (Insurance & Finance Business at time of Selling of Cars)

Exempt:

- Selling of Cars

- Selling of Parts

No Cenvat credit if no excise duty or service tax payable on output

Basic principle is that Cenvat credit is available only when excise duty is payable on final product or service tax is payable on output services [Rule 6(1) of Cenvat Credit Rules].

The Change in Definition & position changed

The term Exempted Services as defined in rule 2(e) of Cenvat Credit Rules, 2004 prior to recent budget 2011 read as follows:-

“Exempted Services” means Taxable services which are exempt from the whole of the Service Tax leviable thereon, and includes services on which no service tax is leviable under section 66 of the Finance Act; (for being Exempted Service it first need to be a Service )

Now this definition has been extended as follows:

““exempted services” means taxable services which are exempt from the whole of the service tax leviable thereon, and includes services on which no service tax is leviable under section 66 of the Finance Act and taxable services whose part of value is exempted on the condition that no credit of inputs and input services, used for providing such taxable service, shall be taken.

Explanation- For the removal of doubts, it is hereby clarified that “exempted services” includes trading.

Rule 6 of Cenvat Credit Rules

Rule 6 applies where both exempted goods and taxable goods are manufactured or exempted and taxable services provided

Following 4 options are available to assessee

- Maintain separate inventory and accounts of receipt and use of inputs and input services used for exempted goods/exempted output services and take only eligible Cenvat Credit – Rule 6(2) of Cenvat Credit Rules

- Take Entire Cenvat Credit and pay amount equal to 6% of value of exempted goods (if he is ‘manufacturer’) and of value of exempted services (if he is service provider) – Rule 6(3)(i) as amended w.e.f. 1-4-2012 [The ‘amount’ payable was 5% upto 31-3- 2012]

- Take Entire Credit and pay an ‘amount’ equal to proportionate Cenvat credit attributable to exempted final product/ exempted output services, as provided in rule 6(3A) – Rule 6(3)(ii) of Cenvat Credit Rules

- Maintain separate accounts for inputs and pay ‘amount’ as determined under rule 6(3A) in respect of input services

Rule 6(2) of Cenvat Credit Rules as recast w.e.f. 1-4-2011 elaborates how records in respect of exempted goods ad exempted services shall be maintained.

(a) the receipt, consumption and inventory of inputs used-

(i) in or in relation to the manufacture of exempted goods;

(ii) in or in relation to the manufacture of dutiable final products excluding exempted goods;

(iii) for the provision of exempted services; (iv) for the provision of output services excluding exempted services.

- Assessee shall take CENVAT credit only on inputs under sub-clauses (ii) and (iv) of clause (a).

(b) the receipt and use of input services-

(i) in or in relation to the manufacture of exempted goods and their clearance upto the place of removal;

(ii) in or in relation to the manufacture of dutiable final products, excluding exempted goods, and their clearance upto the place of removal;

(iii) for the provision of exempted services; and

(iv) for the provision of output services excluding exempted services,

- Assessee shall take CENVAT credit only on input services under sub-clauses (ii) and (iv) of clause (b).

Working in Case of Rule 6 (3A)

Since the Trading Activity is specifically included in the Exempted services, Full input of Services used for both Exempted & Taxable Service can’t be Claimed & the provisions of Rule 6 of the Cenvat Credit Rules, 2004 will be attracted. The value to be taken for this calculation will be as per explanation to rule 6(3) and (3A) of the Cenvat Credit Rules, 2004 which reads as follows:-

Value of trading of cars “shall be the difference between the sale price and the cost of goods sold (determined as per the generally accepted accounting principles without including the expenses incurred towards their purchase) Or

10% of the cost of goods sold, whichever is more”

The procedure prescribed under Rule 6(3A) of CCR 04 requires the MFP/OSP to comply with following:

a. Intimate in writing to the Superintendent of Central Excise, giving the specified particulars;

b. Determine and pay provisionally every month, an amount equivalent to CENVAT credit attributable to manufacture of exempted goods/provision of exempted services in accordance with the formula prescribed in Rule 6(3A)(b) of CCR 04;

c. Determine finally, the amount of CENVAT credit attributable to exempted goods/exempted services for the whole financial year, in accordance with the formula prescribed in Rule 6(3A)(c) of CCR 04;

d. Determine shortfall/surplus in payment of CENVAT Credit;

e. Pay the shortfall by 30th June. In case of delay, interest would be payable at the rate of 24% per annum;

f. Adjust the excess amount on their own by taking credit of such amount; and Intimate in either case to the jurisdictional Superintendent of Central Excise, within 15 days from the date of payment/date of adjustment giving the specified particulars.

Another amendment with the formula prescribed in Rule 6(3A)(b) of CCR 04;

In many cases of taxable services a lesser rate of service tax has been prescribed on composition basis. For example, on works contracts, service tax can be paid @ 4 % on the gross amount as per the relevant rules {Works Contract (Composition Scheme for Payment of Service Tax)Rules, 2007} The said rules prohibit availment of Cenvat credit on inputs if composition scheme is opted. Similar compositions schemes are also available under sub Rules (7), (7B) ad (7C) of Rule 6 of the Service Tax Rules, 1994 for air travel agent, forex broking and lottery promotion services. These services are not considered as exempted services for the purposes of Rule 6 of the CCR, 2004. But service tax is paid only at a lower rate on these services on the total amount. Hence if the entire value of such services is treated as value of taxable services, it will lead to allowing more credit. As per the formulae under sub rule (3A), the credit to be reversed would be in proportion to value of exempted goods and services to the value of both dutiable goods and exempted goods and taxable and exempted services.

Let us taken an example for better understanding.

Credit taken in a month : Rs,10,00,000

Value of exempted goods : Rs.25,00,000

Value of dutiable goods : Rs.75,00,000

Value of taxable services : Rs.50,00,000

(which also includes value of Rs.10,00,000 on Works Contract service, for which service tax was paid under composition scheme).

Value of exempted services : Rs.25,00,000

Prior to this amendment, the credit to be reversed would be:

Rs.25,00,000 + Rs.25,00,000

Rs.10,00,000 X ----------------------------------------------------------------- = Rs. 2,85,714.

Rs.25,00,000 + Rs.75,00,000 + Rs.50,00,000 + Rs.25,00,000

The present amendment requires that in case of the service for which the composition scheme is opted, the value shall the actual service tax paid under composition, converted into corresponding value, by applying the standard rate of service tax. In the given example, on a value of Rs.10,00,000 service tax of Rs.40000 has been paid @ 4 % (Education CESS, etc. ignored for ease of understanding). At the standard rate of 10 %, this service tax of Rs.40,000 will correspond to a value of Rs.4,00,000. So, only Rs.4,00,000 will be considered as the value of this taxable service, for the purpose of the formula. Hence, the credit to be reversed would be

Rs.25,00,000 + Rs.25,00,000

Rs.10,00,000 X ----------------------------------------------------------------- = Rs. 2,95,858.

Rs.25,00,000 + Rs.75,00,000 + Rs.44,00,000 + Rs.25,00,000

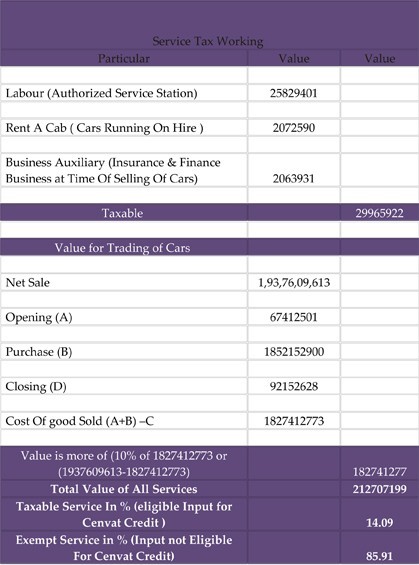

Illustration to make Rule 6 (3A) Simple

CAclubindia

CAclubindia