Statutory Provisions

SECTION 7: SCOPE OF SUPPLY

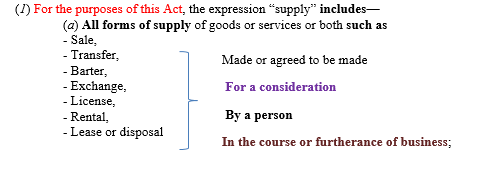

(1) For the purposes of this Act, the expression 'supply' includes-

(a) Import of services for a consideration whether or not in the course or furtherance of business;

(b) The activities specified in Schedule I, made or agreed to be made without a consideration; and

(c) The activities to be treated as supply of goods or supply of services as referred to in Schedule II.

(2) Notwithstanding anything contained in sub-section (1), -

(a) Activities or transactions specified in Schedule III; or

(b) Such activities or transactions undertaken by the Central Government, a State Government or any local authority in which they are engaged as public authorities, as may be notified by the Government on the recommendations of the Council, shall be treated neither as a supply of goods nor a supply of services.

(3) Subject to the provisions of sub-sections (1) and (2), the Government may, on the recommendations of the Council, specify, by Notification, the transactions that are to be treated as-

i. A supply of goods and not as a supply of services; or

ii. A supply of services and not as a supply of goods.

Analysis by Author

As we discussed in introduction part, there must be some certain events which are going to be taxed and the person on whom the tax is to be imposed for collection should be made clear by the charging provisions. As we know in all earlier taxes there were some events which were going to be taxed like in Central Excise Law the taxable event was manufacturing, in vat the taxable event was sale of goods and in service tax the taxable event was provisioning of services. In Goods and Service Tax Law the taxable event is 'SUPPLY' i.e. Supply of Goods or Supply of Services. However, Supply has not been defined in entire Goods and Service Tax Law. Section 7 gives only an illustrative list of supply but does not define the supply completely.

<1> Understanding of the words 'For the purposes of this Act' Section 7 begins with the words 'For the purpose of this Act', means for the purpose of Central Goods and Service Tax Act. Section 7 defines the scope of supply for the purpose of Central Goods and Service Tax. It may be possible the provision of other act like State Goods and Service Tax Act of any state may include different provisions for defining the scope of supply. For example, if you read the section 7 supply includes 'Exchange' as a supply but it may be possible any State Goods and Service Tax Act doesn't include the 'Exchange' as a supply.

<2> Understanding of the words 'Includes'

Friends, for your basic understanding I want to share with you a very basic thing 'how to read a definition'. If a definition starts with the words 'MEANS' it means it is an exhaustive definition. The scope of such definition is limited to the extent it has been defined. But if a definition starts with the words 'Includes' it means it is an illustrative definition. The scope of such definition is beyond its definition. If I talk about the section 7: scope of supply - 'Supply includes' it means supply includes all type of supply and includes Sale, exchange, transfer, barter, disposal, license, and rental. Here it means any transaction which is not a 'sale, exchange, transfer, barter, disposal, license, and rental' it is not necessary it cannot be supply it can be a supply because the word supply has not been defined in entire law. The word includes here representing only examples of supply.

<3> Understanding of the words 'made or agreed to be made'

Friends, the implications of these words are -

* In Goods and Service Tax Law if any supply is made then it is taxable even Supplies which have only been agreed to be made but are yet to be made are also taxable.

* Receipts of advances for supplies agreed to be made become taxable before the actual supply.

* Advances that are retained by the supplier in the event of cancellation of contract for supply by the recipient become taxable as these represent consideration for a supply that was agreed to be made.

We will also discuss this provision as the time of discussing the provision of 'TIME OF SUPPLY'

<4>Understanding of the words 'for a consideration' In order to fall within the scope of supply, the supply must be carried out for a consideration. Consideration in simple word is 'something in return'. However, the term consideration has been defined in CGST as under:

Section 2(31) 'Consideration' in relation to the supply of goods or services or both includes-

a. Any payment made or to be made, whether in money or otherwise, in respect of, in response to, or for the inducement of, the supply of goods or services or both, whether by the recipient or by any other person but shall not include any subsidy given by the Central Government or a State Government;

b. The monetary value of any act or forbearance, in respect of, in response to, or for the inducement of, the supply of goods or services or both, whether by the recipient or by any other person but shall not include any subsidy given by the Central Government or a State Government:

Provided that a deposit given in respect of the supply of goods or services or both shall not be considered as payment made for such supply unless the supplier applies such deposit as consideration for the said supply;

As we discussed in point no. 2 above, the definition of Consideration is inclusive. It means the term consideration is much wider then this definition. One more thing since this definition is inclusive it will not be out of place to refer the definition of Consideration as per Indian Contract Act, 1872 as follows -

'When, at the desire of the promisor, the promise or any other person has done or abstained from doing, or does or abstains from doing, or promises to do or abstain from doing, something, such act or abstinence or promise is called a consideration for the promise'.

That means Consideration will cover the consideration as per section 2(31) of CGST Act and as well as consideration as per Indian Contract Act, 1872.

4.1 What are the implications of the condition that supply should be carried out for a 'consideration'?

* To be taxable a supply should be carried out by a person for a 'Consideration'.

* Supply carried out without any consideration is outside the ambit of taxability.

However, there is certain exception of this condition, activity referred in Schedule I would be supply even if made or agreed to be made WITHOUT CONSIDERATION.

4.2 Understanding of the words 'whether in money or otherwise' in section 2(31).

The words 'whether in money or otherwise' stands for monetary consideration (in money) and non-monetary consideration (otherwise). Monetary consideration means any consideration in the form of money. Money has been defined in Section 2(75).

2(75) 'money' means the Indian legal tender or any foreign currency, cheque, promissory note, bill of exchange, letter of credit, draft, pay order, traveler cheque, money order, postal or electronic remittance or any other instrument recognized by the Reserve Bank of India when used as a consideration to settle an obligation or exchange with Indian legal tender of another denomination but shall not include any currency that is held for its numismatic value;

Non-monetary consideration means compensation in kind such as following -

* Supply of goods and services in return for provision of service

If………… And in return……..

A agrees to dry clean B's Clothes B agrees to click A's Photograph

* Refraining or forbearing to do an act in return for provision of service.

|

If………… |

And in return…….. |

|

A agrees not to open dry clean shop in B's neighbourhood |

B agrees not to open photography shop in A's neighbourhood |

* Tolerating an act or a situation in return for provision of a service.

|

If………… |

And in return…….. |

|

A agrees to design B's house |

B agrees not to object to construct of A's house in his neighborhood. |

* Doing or agreeing to do an act in return for provision of service.

|

If………… |

And in return…….. |

|

A agrees to construct 3 flats for B on land owned by B |

B agrees to provide one flat to A without any monetary consideration. |

4.3 How we will ascertain the money value of non-monetary?

The non-monetary consideration also needs to be valued for determining the tax payable on the supply since CGST is levied on the value of consideration received or to be received on monetary consideration and money value of non-monetary consideration. The value of non-monetary consideration is to be determined according to the 'Determination of Value of Supply' Rules.

4.4 Can a consideration for service to be paid by a person other than the person receiving the service?

Yes, the consideration for a service may be provided by a person other than the recipient. As per section 2(75) consideration includes-

'Any payment made or to be made, whether in money or otherwise, in respect of, in response to, or for the inducement of, the supply of goods or services or both, whether by the recipient or by any other person but shall not include any subsidy given by the Central Government or a State Government'

<5> Understanding of the words 'by a person'

Person is not restricted to natural person. Person has been defined in Section 2(84) of the Act. The following shall be considered as persons for the purpose of this Act.

(84) 'Person' includes-

(a) an individual;

(b) a Hindu Undivided Family;

(c) a company;

(d) a firm;

(e) a Limited Liability Partnership;

(f) an association of persons or a body of individuals, whether incorporated or

not, in India or outside India;

(g) any corporation established by or under any Central Act, State Act or

Provincial Act or a Government company as defined in clause (45) of section 2 of

the Companies Act, 2013;

(h) Anybody corporate incorporated by or under the laws of a country outside

India;

(i) a co-operative society registered under any law relating to co-operative

(j) a local authority;

(k) Central Government or a State Government;

(l) society as defined under the Societies Registration Act, 1860;

(m) trust; and

(n) every artificial juridical person, not falling within any of the above;

I think now you are very clear that every person has been covered in to Goods and Service Tax Law.

<6> Understanding of the words 'In the course or furtherance of business'

Section 7(1) (a) says that supply should be 'IN THE COURSE OF BUSINESS OR FURTHERENCE OF BUSINESS' we can interpret that if a person (Mr. X) sells his personal old jewellery to a jeweller for Rs. 1 Lac, since he is an individual covered in the definition of a person u/s Section 2(84) and consideration is also exist in the form of Rs. 1 Lac and Sale of Jewellery is also covered in the scope of supply as 'SALE' but the sale made by Mr. X is not in the course of business or furtherance of business. Because Mr. X is not a dealer of Gold Jewellery, such sale is not a part of his business. Such supply is out of the scope of supply.

Therefore, the supply should in the course of business or furtherance of business for levying CGST but Import of services for a consideration whether or not in the course or furtherance of business will be leviable for CGST that means in case of import it is not necessary that it should be made in the course of business or furtherance of business even import for personal use is also leviable for CGST.

<7> The activities to be treated as supply of goods or supply of services as referred to in Schedule II.

There may be some doubt in case of a supply whether it is a supply of goods or supply of services for e.g.. works contract. Schedule II will specify in some cases that a particular supply is a supply of goods or supply of service. In our example Schedule II specifies that works contract supply will be treated as a supply of service only. One more thing to discuss here only in case of some specified cases schedule II will clear your doubt and other cases which are not covered in schedule II may be cleared later on by the Govt. on the recommendations of Council. That's why below mentioned words are used in section 7.

Subject to the provisions of sub-sections (1) and (2), the Government may, on the recommendations of the Council, specify, by Notification, the transactions that are to be treated as-

(a) A supply of goods and not as a supply of services; or

(b) A supply of services and not as a supply of goods.

Now a question arises, now all we know that CGST is leviable on supply whether a supply of goods or supply of service then why schedule II is there to specify a supply is supply of goods or supply of services. Is is just because of there are some provisions in GST Law which are different in case of supply of goods and supply of services mainly TIME OF SUPPLY is different in case of Supply of Goods and Supply of Services which we will discuss in our chapter 'TIME OF SUPPLY' and one another reason may be different rate of tax in case of supply of goods and supply of services.

<8> What are activities that are neither a supply of goods nor a supply of services i.e. not leviable to GST. Schedule III of the CGST Act, 2017 covers certain activities which are neither supply of goods nor supply of services and these activities are :

1. Services by an employee to the employer in the course of or in relation to his employment.

2. Services by any court or Tribunal established under any law for the time being in force.

3. (a) the functions performed by the Members of Parliament, Members of State Legislature, Members of Panchayats, Members of Municipalities and Members of other local authorities;

(b) the duties performed by any person who holds any post in pursuance of the provisions of the Constitution in that capacity; or

(c) the duties performed by any person as a Chairperson or a Member or a Director in a body established by the Central Government or a State Government or local authority and who is not deemed as an employee before the commencement of this clause.

4. Services of funeral, burial, crematorium or mortuary including transportation of the deceased.

5. Sale of land and, subject to clause (b) of paragraph 5 of Schedule II, sale of building.

6. Actionable claims, other than lottery, betting and gambling.

We will discuss all these activities in depth later on in our next Articles.

Apart from above mentioned activities, Govt. has power to specify certain activities which shall be treated neither as a supply of goods nor supply of services, on the recommendations of council.

(2) Notwithstanding anything contained in sub-section (1), --

(a) Activities or transactions specified in Schedule III; or

(b) Such activities or transactions undertaken by the Central Government, a State Government or any local authority in which they are engaged as public authorities, as may be notified by the Government on the recommendations of the Council, shall be treated neither as a supply of goods nor a supply of services.

You can also subscribe our Youtube channel "ALL ABOUT TAXES" for more updates by clicking: https://www.youtube.com/allabouttaxes

CAclubindia

CAclubindia