Companies Act 2013 (the Act) can be one legislation that can be contrary to the most popular slogan “Ease of doing business in India”, it has led many corporates and professionals to re-think and re-define this slogan. With too many weird provisions in the Act the new slogan that emerge on account of the ambiguity of the various provisions is “Difficulty of doing business in India”.

Impact of Section 403

Section 403 of the Act has been drafted in a manner that is detrimental to the corporate in all respects. We all understand the concept of 9 months, which signifies BIRTH, but in the Act beyond 9 months and 30 days it can signify DEATH, for a company that fails to comply with section 403. Companies are required to make corporate filings and each of these filings have a deadline that is prescribed by the Act; the minimum in most cases is 30 days time frame from the corporate action. In case the company fails to file the prescribed forms within 30 days, it can choose to file the same during the lifetime of the company with a maximum penalty of 9 times of the filing fee. But there are 6 instances where the lawmakers have decided to cap the lifeline of these forms to 10 months only and in case a company defaults in filing then there are severe penalties prescribed in the Act that can result in death of small companies. The contents of the section 403 is reproduced herein for easy understanding:

403. (1) Any document, required to be submitted, filed, registered or recorded, or any fact or information required or authorised to be registered under this Act, shall be submitted, filed, registered or recorded within the time specified in the relevant provision on payment of such fee as may be prescribed:

Provided that any document, fact or information may be submitted, filed, registered or recorded, after the time specified in relevant provision for such submission, filing, registering or recording, within a period of two hundred and seventy days from the date by which it should have been submitted, filed, registered or recorded, as the case may be, on payment of such additional fee as may be prescribed:

Provided further that any such document, fact or information may, without prejudice to any other legal action or liability under the Act, be also submitted, filed, registered or recorded, after the first time specified in first proviso on payment of fee and additional fee specified under this section.

(2) Where a company fails or commits any default to submit, file, register or record any document, fact or information under sub-section (1) before the expiry of the period specified in the first proviso to that sub-section with additional fee, the company and the officers of the company who are in default, shall, without prejudice to the liability for payment of fee and additional fee, be liable for the penalty or punishment provided under this Act for such failure or default.

The sections where mention has been made of section 403 is listed herein:

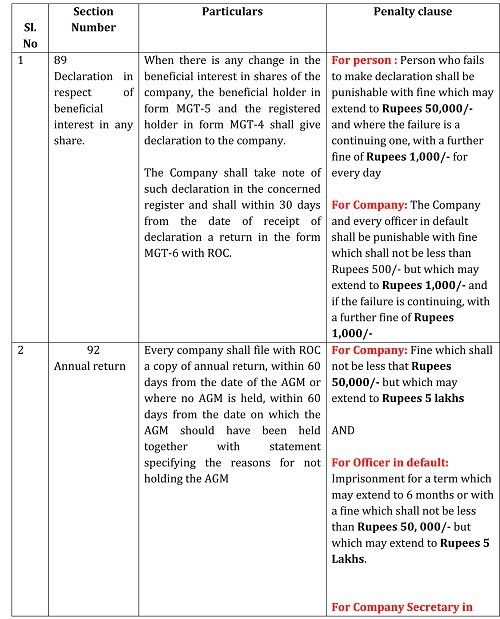

Section 89 - Declaration in respect of beneficial interest in any share.

The Company shall take note of such declaration in the concerned register and shall within 30 days from the date of receipt of declaration file a return with ROC. – FORM MGT 6

Section 92 – Annual Return

Every company shall file with ROC a copy of annual return, within 60 days from the date of the AGM or where no AGM is held, within 60 days from the date on which the AGM should have been held together with statement specifying the reasons for not holding the AGM – FORM 20B/FORM MGT 7

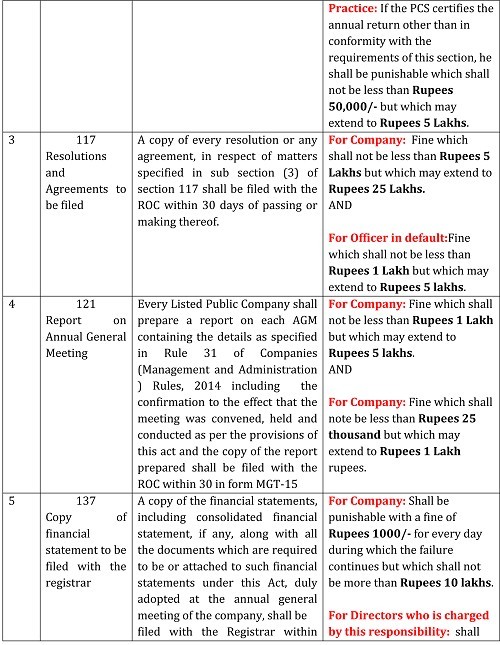

Section 117 - Resolutions and Agreements to be filed

A copy of every resolution or any agreement, in respect of matters specified in sub section (3) of section 117 which shall be filed with the ROC within 30 days of passing or making thereof. – FORM MGT 14

Section 121 - Report on Annual General Meeting

Every Listed Public Company shall prepare a report on each Annual General Meeting containing the details as specified in Rule 31 of Companies (Management and Administration) Rules, 2014 including the confirmation to the effect that the meeting was convened, held and conducted as per the provisions of this Act and the copy of the report shall be filed with the ROC within 30 days from the date of meeting - FORM MGT-15

Section 137 – Copy of financial statement to be filed with the Registrar

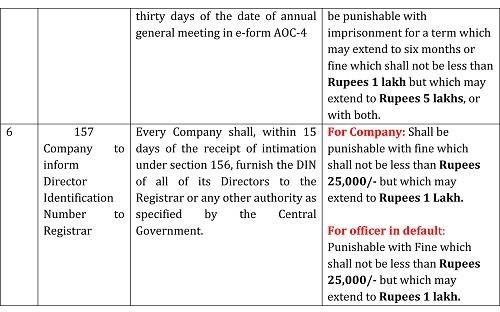

A copy of the financial statements, including consolidated financial statement, if any, along with all the documents which are required to be attached to such financial statements under this Act, duly adopted at the annual general meeting of the company, shall be filed with the Registrar within thirty days of the date of annual general meeting -Form AOC-4

Section 157 - Company to inform Director Identification Number to Registrar

Every Company shall, within 15 days of the receipt of intimation under section 156, furnish the DIN of all of its Directors to the Registrar or any other authority as specified by the Central Government. – FORM DIR 3C

The onus is on the professionals to identify the corporate actions, which require filing of any of the forms listed above. In case of default in filing the form and if the time limit exceeds 300 days then the company does not have a choice but to go ahead and immediately file a compounding application under section 441 (yet to be notified).

Read the penal provisions under these 6 Sections that have drawn reference to section 403, in case of any slip up, the company is in for serious trouble and for a small company the implications can lead to grave consequences.

The table gives details on to the penal provisions under the each section mentioned above:

CAclubindia

CAclubindia