Steps towards implementation of GST

2004: Dr. Kelkar Task Force recommended the need of a National GST

Jan. 2007: First GST study released by Dr. Shome

2007: Consultation with stakeholders on GST Model

April 2007: CST phase out started

May 2007: Joint Working Groups appointed by E.C.

Nov 2007: 13th Finance Commission Constituted

Nov 2007: Joint Working Groups submitted Report

Feb 2008: FM announced introduction of GST from 1.4.2010 in Budget Speech 2008-09

April 2008: Empowered Committee (EC) finalized its views on GST structure

July 2009: FM announced dual GST from April 1, 2010 in Budget Speech 2009-10

Oct 2009: 13th Finance Commission to submit its report

Nov 2009: Release of First Discussion Paper on GST

2009-2010:Consultation on Model of inter-state transactions, RNR and other issues - In progress

Nandan Nilekani given the responsibility for creating the required IT structure and NSDL has been chosen as the technology partner for operating the structure.

Dec 2014: 122nd Constitution Amendment Bill introduced in Parliament

May 2015: 122nd Constitutional Amendment bill passed by Lok Sabha and referred to the Select Committee of Rajya Sabha to submit its report in first week on Monsoon Session

Taxes to be subsumed:

• Excise

• Customs - CVD & SAD

• Service Tax

• VAT

• CST

• Other taxes like Entry Tax, Entertainment Tax, Taxes on Lottery & Gambling

More than 100 countries across globe have introduced GST.

The GST rates in various countries ranges from as low as 5% in Taiwan to as high as 25% in Denmark.

Revenue Neutral rate (RNR) of our country comes to _____%

FM has recently proposed GST rate of _____%

GST means

• any taxes on supply of goods or services or both

• except taxes on the supply of the alcoholic liquor for human consumption

"Services" means anything other than good.

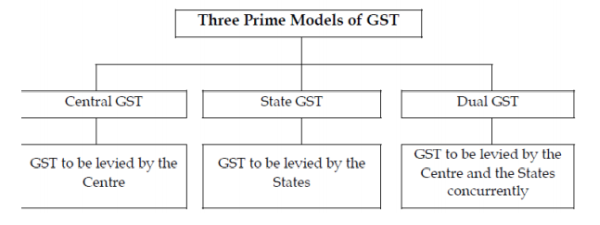

There are three prime models of GST:

• GST at Central (Union) Government Level only

• GST at State Government Level only

• GST at both Union & State Government Levels

Features of Proposed GST :

1. Destination based taxation.

2. Apply to all stages of the value chain

3. Apply to all taxable supplies of goods or services (As against manufacture, sale or provision of service) made for a consideration except -

• Exempted goods or services - common list for CGST & SGST

• Goods or services outside the purview of GST

• Transactions below threshold limits

4. Dual GST having two concurrent components -

• Central GST levied and collected by the Centre

• State GST levied and collected by the States

5. All goods or services likely to be covered under GST except:

• Alcohol for human consumption - State Excise plus VAT

• Electricity - Electricity Duty

• Real Estate - Stamp Duty plus Property Taxes

• Petroleum products (to be brought under GST from date to be notified on recommendation of GST Council)

6. Tobacco Products under GST with Central Excise duty.

7. CGST and SGST on intra-state supplies of goods or services in India.

8. IGST (Integrated GST) on inter-state supplies of goods or services in India - levied and collected by the Centre.

9. IGST applicable to -

• Import of goods and services

• Inter-state stock transfers of goods and services

10. Export of goods and services - Zero rated

11. Additional tax of 1% on inter-state taxable supply of goods by state of origin and non cenvatable

To read the full article: Click here

CAclubindia

CAclubindia