SEBI LISTING REGULATIONS (LODR)

“CORPORATE GOVERNANCE REQUIREMENTS WITH RESPECT TO SUBSIDIARY OF LISTED ENTITY”

CONDITIONS With Respect to Subsidiary of Listed Entity:

I. Board of Director:

At least one Independent Director of Listed Company shall be director on the Board of Material unlisted Subsidiary Company (hereafter referred as “MUS”), incorporate in India.

Materiality of Related Party Transaction:

A transaction with a [1]related party shall be considered material;

o if the transaction(s) to be entered into individually or taken together with previous transactions during a financial year,

o exceeds 10% of the annual consolidated turnover of the listed entity

o As per the latest Audited Financial Statements.

Example[2]

II. Review of Financial Statement:

The audit committee of the listed entity shall also review the financial statements of MUS, in particular, the investments made by the MUS.

III. Minutes:

The Minutes of the Board Meeting of Subsidiary Company shall be placed at the meeting of the Board of Directors of the listed entity.

IV. Statement of All Significant Transactions and Arrangements:

The management of the unlisted subsidiary shall periodically place before the Board of Directors of the listed entity, a statement of all significant transactions and arrangements entered into by the unlisted subsidiary.

Definition of Significant Transactions and Arrangements:

Any individual transaction or arrangement that exceeds or is likely to exceed below given limits of the unlisted material subsidiary for the immediately preceding accounting year.

· 10% (ten percent) of the total revenues or

· 10% (ten percent) of the total expenses or

· 10% (ten percent) of the total assets or

· 10% (ten percent) of the total liabilities,

Disinvestment by Listed Entity:

i. A Listed entity shall not dispose of shares in its material Subsidiary resulting in reduction of its [3]shareholding to less than 50% (fifty percent) OR

ii. A Listed entity shall not dispose of shares in its material Subsidiary resulting cease the exercise of control over the subsidiary

Without approval of Shareholders in General Meeting by passing of Special Resolution

EXCEPTION:

Such divestment is made under a scheme of arrangement duly approved by a Court/ Tribunal.

SELLING, LEASING & DISPOSING OF ASSESTS OF SUBSIDIARY:

A Listed entity shall not sell, dispose and lease assets of its material Subsidiary without approval of Shareholders in General Meeting by passing of special resolution IF, such dispose of aggregate in a financial year is more than 20% of the assets of the material subsidiary

EXCEPTION:

Such sale/dispose/lease is made under a scheme of arrangement duly approved by a Court/ Tribunal.

CHAIN OF SUBSIDIARY:

Where a listed entity has a listed subsidiary, which is itself a holding company, the provisions of this regulation shall apply to the listed subsidiary in so far as its subsidiaries are concerned.

Example:

If Company ‘A’ Listed entity have subsidiary ‘B’ Listed entity. Company ‘B’ also has a Subsidiary ‘C’ unlisted material subsidiary.

Provision of this regulation applicable On Company ‘B’.

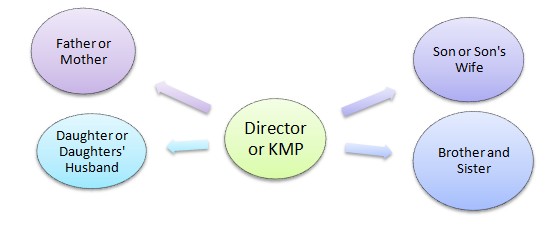

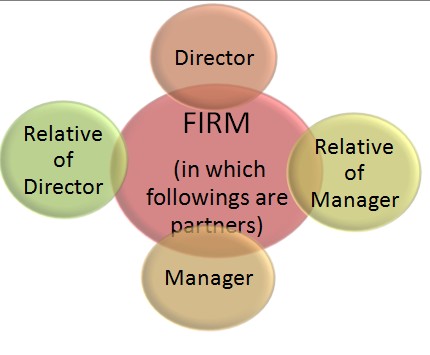

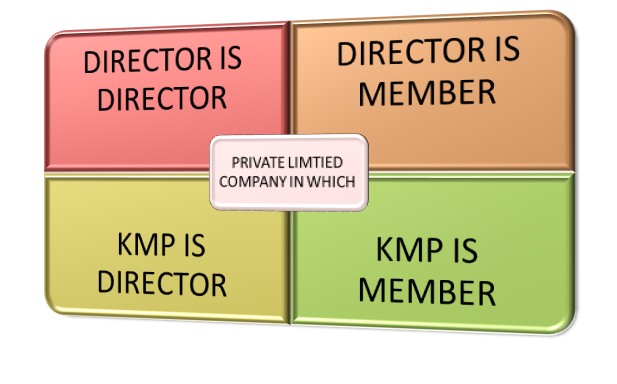

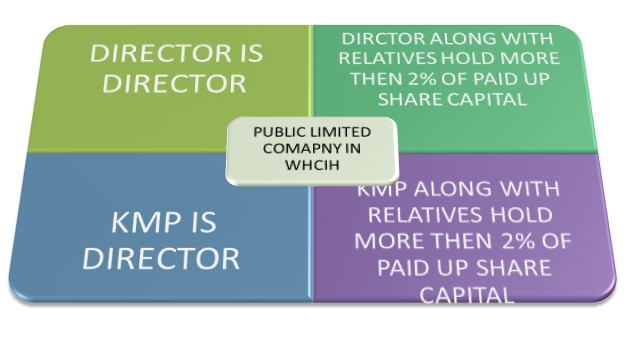

A. “RELATED PARTY” means a related party as defined under sub-section (76) of section 2 of the [4]Companies Act, 2013 or under the applicable accounting standards:

Not Applicable: This definition shall not be applicable for the units issued by mutual funds which are listed on a recognized stock exchange(s);

Definition of Related Party as per 2(76) of Companies act, 2013 (DRAWINGS)

[1]Define at the end of the Article.

[2] During financial year if company enters into transaction with related party, that transaction together with other transactions during that financial year amounting more than 10% of consolidated turnover of the listed company shall be consider as material related party transaction. For calculation of 10% of consolidated turnover latest audited financial statement of the listed company shall be taken into consideration.

[3]Either On Its Own Or Together With Other subsidiaries

[4]Define at the end of the Article

CAclubindia

CAclubindia