Non Holding of AGM within due date.

Ministry of Corporate Affairs has issued notice to approximately 3000 companies due to non compliance of provision of Section 96(1) for not holding of AGM within Due date.

As per notice companies have to reply the notice within 15 days of receipt of notice. In case of non reply of notice within 15 days it shall be presumed that company has nothing to say and penal action shall be initiate against the company.

In this editorial author will discuss the followings:

- Reply of Notice of MCA

- Penal Provisions for non holding of AGM within Due Date

- Process of Compounding of such non compliance

IMPORTANT NOTE

• This is non compliance of Section 96.

• Penal provisions for same are mentioned under Section 99.

• Compounding u/s 441.

• Adjudication power u/s 454.

Step - I: Reply of Notice to MCA

As per provision of Section 96 Company have to held AGM within 6 month from the end of Financial Year or within 15 month from the last AGM of Company, Whichever is earlier.

Therefore, this is responsibility of company to reply the notice of MCA with following points:

a. Actual reasons for not holding of AGM within Due date.

b. As non compliance occur in previous years therefore mention in reply that Company will file application for Compounding with appropriate authority. If possible file the compounding application and attached receiving of same with Notice.

Penal Provision - Non Compliance of 96

As per Section 99 If any default is made in holding a meeting of the company in accordance with section 96 or section 97 or section 98 or in complying with any directions of the Tribunal,

The company and every officer of the company who is in default shall be punishable with Fine which may extend to one lakh rupees and in the case of a continuing default, with a further fine which may extend to five thousand rupees for every day during which such default continues.

Officer who is in default: means any of the following officers of a company, namely

(i) whole-time director;

(ii) key managerial personnel;

(iii) where there is no key managerial personnel, such director or directors as specified by the Board in this behalf and who has or have given his or their consent in writing to the Board to such specification, or all the directors, if no director is so specified;

Note: Therefore, separate fine shall be impose on Company and Office in default both.

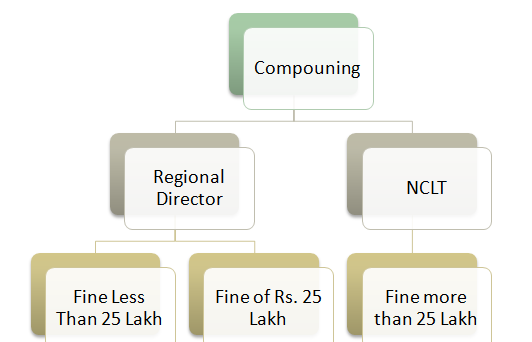

COMPOUNDING:

As mention above in section 96 fine is less than 25 Lakh therefore power of compounding vested with Regional Director.

Step - II: Process of Compounding with RD:

As the power of compounding in above mentioned matter vested with Regional Director of the Region. Therefore Company have to file application with Regional Director by following process:

i. Preparation of Application:

There is no specific format of Compounding application with RD under Companies Act. Therefore, Company have to prepare a normal application mentioning the following: (these are some examples:

· Name

· Registered Office

· Capital Structure

· Jurisdiction of RD

· Facts of the Case

· Relief to be sought

Application should annex with proper attachments Like:

· Affidavit verifying the application

· Financial Statements of Company

· Proof of holding of Annual General Meeting, etc.

ii. Filing of Application with Registrar of Companies:

Company has to file a copy of such application with Registrar of Company in e-form GNL-2. After receipt of GNL-2 ROC shall prepare its report and submit the same with Regional Director.

iii. Filing of Application with Regional Director:

Company has to file a copy of such application with Regional Director in e-form RD-1 and submit hard copy of application with all annexure to Regional Director.

iv. Hearing by Regional Director:

There will be a personal hearing before the Regional Director, which shall decide the amount to be paid for compounding.

v. Passing of Order Regional Director:

Get the order passed by the RD and pay the amount stipulated within the time fixed.

vi. Filing of Order with ROC:

File Order of RD with ROC in e-form INC-28 and Roc will take note of the same.

CONCLUSION:

If company done non compliance of Section 96 there is no way out then compounding for making default good. As per Act RD can’t impose penalty more than mentioned in the concerned section.

CAclubindia

CAclubindia