Refund Process under GST Regime

Hello friends, in this article we discuss all main issues related with refund in GST regime.

We divided whole topic in 6 parts which are as follows:

- Introduction

- Refund forms

- Time limit for filing refund

- Documents required for claiming refund

- Procedure for claiming refund

- Time limit for granting refund

Introductions:

In the taxation administration, refund refers to any amount that is due to the tax payer from the tax administration. In the present taxation system it is considered as a strained area, both for the taxpayer and the tax administration. So in order to establish an effective and efficient tax administration system it is essential that issues on which refund arises ought to be kept at minimum and be clearly defined in the law.

Situations under which refund may arise:-

As under GST there are several indirect taxes which subsume together such as excise duty, VAT, custom duty, service tax etc. The situation under which refund may be arises are as follows:

- Mistakenly excess payment of tax,

- Export of goods/services under rebate or refund of accumulated input credit of duty/tax when goods are exported,

- Finalization of provisional assessment,

- Refund of pre-deposit amount deposited at the time of filing appeal or when appeal is decided in favour of the appellant,

- Payment of duty / tax during investigation but no or less liability arises at the time of finalization of investigation / adjudication,

- Refund of tax payment on purchases made by Embassies or UN bodies,

- Credit accumulation due to output being tax exempt or nil-rated,

- Credit accumulation due to inverted duty structure i.e. due to tax rate differential between output and inputs,

- Year-end or volume based incentives provided by the supplier through credit notes,

- Tax refund for international tourists.

Refund Forms:-

Refund forms are very simple, easy to understand and in electronically format so that anyone can file its refund application rapidly. There are separate forms for refund claim, refund order, reduction/adjustments of refund and refund claimed by Embassies/ international and public organizations and their officials.

|

S. No. |

Form Number |

Detail |

|

1 |

GST RFD-01 |

Refund application form along with details of goods certified by a chartered accountant. |

|

2 |

GST RFD-02 |

Acknowledgement for refund claimed |

|

3 |

GST RFD-03 |

Notice of Deficiency on Application for Refund |

|

4 |

GST RFD-04 |

Provisional Refund Sanction Order |

|

5 |

GST RFD-05 |

Refund Sanction/Rejection Order |

|

6 |

GST RFD-06 |

Order for Complete adjustment of claimed Refund |

|

7 |

GST RFD-07 |

Show cause notice for reject of refund application |

|

8 |

GST RFD-08 |

Payment Advice issued to banks |

|

9 |

GST RFD-09 |

Order for Interest on delayed refunds |

|

10 |

GST RFD-10 |

Refund application form for Embassy/International Organizations |

Time period for filing refund:-

It is recommended that a period of 2 year from the relevant date may be allowed for filing refund application.

|

S. No. |

Situation for claiming refund |

Relevant date |

|

1 |

Mistakenly excess payment of tax |

Date of Payment |

|

2 (a) |

Export of goods under rebate or refund of accumulated input credit of duty/tax when goods are exported |

Date on which "Let Export order" given by proper officer. |

|

(b) |

Export of services under rebate or refund of accumulated input credit of duty/tax when services are exported |

Date of BRC |

|

3 |

Finalization of provisional assessment |

Date of Finalization order |

|

4 |

Refund of pre-deposit amount deposited at the time of filing appeal or when appeal is decided in favor of the appellant |

Date of communication of appellate authority order in favor of taxpayer |

|

5 |

Payment of duty / tax during investigation but no or less liability arises at the time of finalization of investigation / adjudication |

Date of communication of adjudicating order or order related to completion of investigation. |

|

6 |

Refund of tax payment on purchases made by Embassies or UN bodies |

Date of payment of GST |

|

7 |

Credit accumulation due to output being tax exempt or nil-rated |

Date of providing service (normally the date of invoice) |

|

8 |

Credit accumulation due to inverted duty structure i.e. due to tax rate differential between output and inputs |

Last day of the financial year |

Documents required for claiming refund:-

For claiming refund there are several documents which are required so that refund application should be minimal but adequate. Below given the list of documents required;

1. All payment of taxes are done electronically and all the B2B invoices are uploaded on the portal hence there are following documents which are not called during refund:-

- Copy of proof of payment of tax i.e, challan copy etc.

- Copy of invoice

- Documents evidencing export as it will be verified vide ICEGATE.

2. A certificate from a chartered accountant may be called for evidencing that the tax burden has not been passed on to buyer under the principle of "Unjust enrichment".

3. Any other documents as prescribed by the refund sanctioning authority.

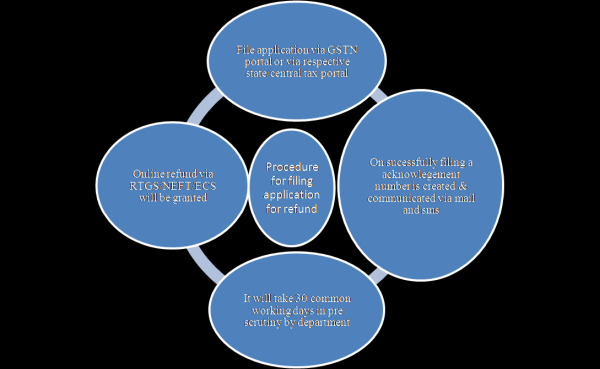

Procedure for claiming refund:-

It is recommended that state government will deal with SCGT refund applications and central government will deal with CGST and IGST refund applications.

Procedure to be followed in this regard shown under through a diagram:

General points on procedure of claiming refund:-

- In some case if refund is not found legal or correct than a SCN may be issued to the applicant.

- In case refund application is found in order but not satisfy the principle of unjust enrichment than amount will transfer to consumer welfare fund.

- It is also recommended that there should no refund in case the amount is less than Rs. 1000.

- Relevant authorities may adjust the refund amount against demand amount due from assesses.

Time Limit for granting refund & interest in case of delay:-

As per the GST Law the time limit for granting refund will be 90 days from date of system generated acknowledgement of refund.

In case refund is not granted in prescribed time limited than a interest @ 6% p.a is recommended and the period for interest will be started from the last day on which refund should be granted.

Hope you will find it useful.

Please like and share my Facebook page named as acumenadvisors.

The author can also be reached at advisorsacumen@gmail.com.

CAclubindia

CAclubindia