Notification No. 12/2013 – Service Tax

1. The exemption shall be provided by way of refund of service tax paid on the specified services received by the SEZ Unit or the Developer and used for the authorised operations:

Provided that where the specified services received by the SEZ Unit or the Developer are used exclusively for the authorised operations, the person liable to pay service tax has the option not to pay the service tax ab initio, subject to the conditions and procedure as stated below.

2. This exemption shall be given effect to in the following manner:

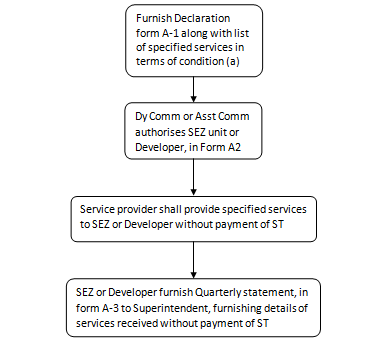

(a)The SEZ Unit or the Developer shall get an approval by the Approval Committee of the list of the services as are required for the authorised operations on which the SEZ Unit or Developer wish to claim exemption from service tax.

(b) The ab-initio exemption on the specified services shall be allowed subject to the following procedure and conditions, namely:-

SEZ or Developer shall furnish an undertaking that in case the specified services are not exclusively for authorised operation it shall pay to the government an amount that is claimed by way of exemption from Service tax and cesses along with interest as applicable on delayed payment of service tax under the provisions of the said Act read with the rules made there under.

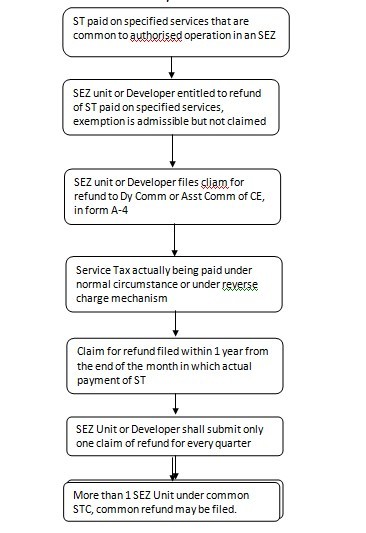

Refund of Service Tax

The refund of service tax on (i) the specified services that are not exclusively used for authorized operation, or (ii) the specified services on which ab-initio exemption is admissible but not claimed, shall be allowed subject to the following procedure and conditions, namely:-

Notwithstanding anything contained in this notification, SEZ Unit or the Developer shall have the option not to avail of this exemption and instead take CENVAT credit on the specified services in accordance with the CENVAT Credit Rules, 2004.

Case Law:

In Zydus Tech Ltd V. CST (2013) 30 Taxmann 183 (CESTAT) assessee was manufacturer of drugs. Assessee received various services of technical consultancy and testing. The services were in the list approved by Development Commissioner. However, the refund claim of input services was rejected on the ground that the services used for R&D before manufacture and not eligible as input services. It was held that manufacturing process of medicaments is not comparable to other products. Hence, trial manufacture and R&D of such drugs is for authorized operations of manufacturer, thus it was eligible for refund.

CAclubindia

CAclubindia