Rectification has become easy since switchover to online but it has its own limitation. In this article

I will be covering almost every point related to rectification in terms of:

Online request for rectification.

Required information before filing a rectification application.

Mistakes committed while filing a rectification.

Need for a proper system at your office place to avoid mistakes at each level of filing i.e.

1) Filing of Income Tax Return

2) Response to intimation u/s 143(1)

3) Reply to Order u/s 154

Also, I would cover issues related to refunds and notice u/s 245 which is being sent by ITO frequently to most of the assessee.

Online Request for Rectification:-

Online rectification can be only carried out if the return is filed ONLINE.

Generally, CPC sends an intimation u/s 143(1) to almost every assessee. The reason for same being:

Interest computed u/s 244A (in case of refund)

Even if there is difference of Rs 1 in Income computation between assessee and CPC , CPC sends an intimation ( Though the tax computation does not change)

Interest recomputed u/s 234A, 234B, 234C.

Tax credit mismatch is one of the major reasons for intimation u/s 143.

PRE Requisite for Online Rectification-:

CPC Communication number ( which is clearly mentioned in intimation u/s 143(1)

Form 26 AS : It s my observation after going through lot of intimations, that the system in CPC generates tax credit mismatch intimation by directly comparing data with Form 26AS.

PROCEDURE :

To file your Rectification, you should be a registered user in e-Filing application. Below listed e the steps to file Rectification.

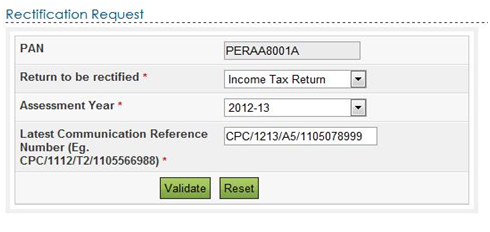

Step 1 Login to e-Filing application and GO TO My Account Rectification Request.

Step 2 Select Return to be rectified as Income Tax Return from the drop down available.

Step 3 Select the Assessment Year for which Rectification is to be e-Filed. Enter the Latest Communication Reference Number (as mentioned in the CPC Order)

Step 4 Click Validate

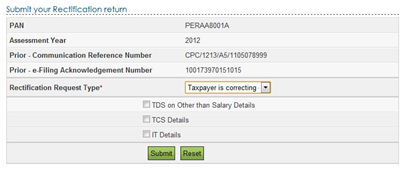

Step 5 Select the Rectification Request Type .

Step 6 On selecting the option Taxpayer is correcting data for Tax Credit mismatch only , three check boxes TCS, TDS, IT are displayed. You may select the checkbox for which data needs to be corrected. Details regarding these fields will be prefilled from the ITR filed. User can add a maximum of 10 entries for each of the selections. No upload of any ITR is required.

What if Entries are more than 10 Then Following step needs to be done exactly after 5th Step.

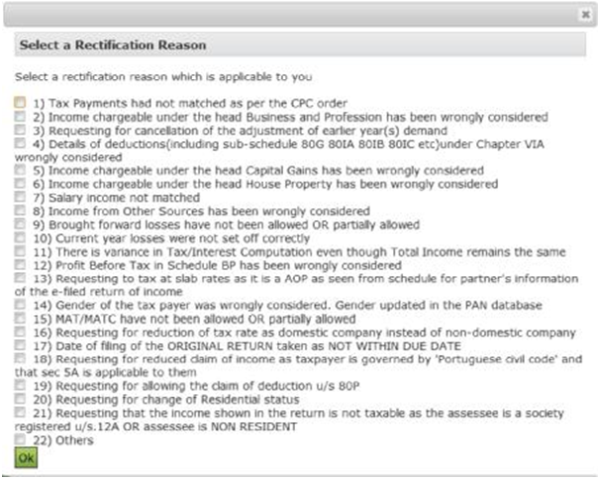

On selecting the option Taxpayer is correcting Data in Rectification , select the reason for seeking rectification. In this case the 1st option i.e Tax payment had not matched as per CPC order. Here XML is uploaded since the data is big.

Mistakes committed while filing Rectification Request:

1) Mentioning of proper Communication number.

2) In case of communication no, each intimation or order which is generated has a unique Communication no and the rectification request is always a reply to the latest order or intimation. It so happens that intimation is raised and subsequently order is also passed for same A.Y , it is important to mention the CPC no of latest communication from CPC.

3) Rectification should not be filed for change in Income. For change in Income one should file a revised return.

4) What happens if you Filed a Rectification for change in Income Ans: Mostly the Rectification Rights transfers from CPC to Jurisdictional A.O and all processing of further rectification has to be submitted to your Jurisdictional A.O in hard copy. Reason for it is that Rectification facility is to correct mistake and not to put forward new claims.

Proper System At office place to avoid any errors:

1) Filing of Income Tax Return

Especially in case of refund return one needs to re verify Address and Bank Account Details.

Matching Form 26 AS data with return data. It s clearly established by CPC in past few years, especially from when Online Return has started, that one needs to consider Form 26 AS as more important.

For Example: At times the client gets you his Form 16/16A and you fill data as per Form 16. If the data does not match with Form 26 AS , then the assessee will surely get an intimation from CPC.

What to do in such case

It is better to file return as per Form 26 AS. Then in that case the client needs to ask the organization to revise their TDS return or check where the mistake is and rectify it. If the organization rectifies their mistake, the client can subsequently file a revised return. The other option could be to submit the form 16/16A as the case may be with the Jurisdictional A.O and claim for the credit , which infact is a lengthy process since it takes a lot of time to process through hard copy submission.

In case of Income from other sources, we show Income from FD and income from saving bank A/c and claim deduction u/s 57. Some software s are so designed that they take the exact amount as shown under Income from saving bank A/c to Deduction u/s 80 TTA. If in this case the net effect of Income from other sources is negative or Deduction claimed under sec 80TTA is more than it, then the assessee will surely get an intimation u/s 143(1).

Example: Suppose Income from Saving Bank is Rs 10000, Interest on FD is Rs 100000 and any expense claimed under section 57 is Rs 105000. Here maximum deduction under 80TTA would be Rs 5000 and any amount claimed more than that would result in intimation.

2) Response to Intimation u/s 143(1)

More or less for every small reason an intimation is raised by CPC and I have tried to cover as much as possible. I have already covered few in the start of the article and will be covering few more in relation to refund in respective head of information.

3) Reply to Order u/s 154

Replying to order u/s 154 is done in same lines that of intimation . The process is also as same like intimation u/s 143(1). One of the most important factor to take care while replying is that any subsequent rights might get transferred to A.O/AST and things have to be sorted out at ITO.

Note: The transfer of right totally depends on the reply and to the extent the mistakes have been corrected. There is no specific reason as to CPC transferring case to A.O.

Refunds and Issue Related to Refunds:

There are few pre-requisites in connection with refund processing if the refunds are not issued due to some reason. I will also be covering reasons as to why Refunds are not issued.

Pre-requisities:

1) Latest Communication number

2) Refund Sequence number (intimation or order)

3) Bank Account number, Name of the Bank And IFSC code

4) Address of the assessee

What happens in the following situation

1) Cheque Expired :- In this case Refund Re-issue Request needs to be send.

Step 1 Login to e-Filing application and GO TO ---- My Account ----- Refund Re-Issue Request.

Step 2 Fill The proper A.Y in which the refund exists, CPC communication no, Refund Sequence no

Step 3 Once the initial data is integrated, then Bank A/c details and other details related to refunds are to be filled

Step 4- An acknowledgment number is generated which can be checked at

My Request List ------ Refund Re-Issue Request

2) Wrong A/c no and ECS refund is issued: In this case the process is identical to the above process

3) Wrong A/c no and Cheque is Issued: When cheque is issued and wrong A/c no is given the process kind of becomes difficult. Reason being when cheque is issued the system at CPC is updated as refund issued. Hence in this case refund re-issue request is not possible. There are 2 options in such cases:

1st option is that one needs to write to the Income tax asking to change the A/c no along with the copy of cheque. On the refund cheque the address of issuer bank is there, but this method is something theoretical and I have never tried it in my whole working life.

2nd Option and the option I have tried is to wait for expiry of cheque, you wont get any Interest on the amount of the refund though. Once the cheque expires then within 5-10 working days the CPC updates the system online and you can again proceed with the first process of cheque expired, this time mentioning details correctly.

4) Wrong Address:- If a wrong address is integrated in Income tax return, then there is high possibility your cheque will return and you will be informed about the same through Email or Text message. One needs to follow the same Process as in Option 1.

5) Refund Stuck, No Intimation Received and New Intimation can t be Requested: This is a very unique case, but does happen when you change your accountant/ C.A and forget to integrate new email id and phone number to which communication is sent. It so happens that intimation containing information about CPC no and refund sequence number is sent to old or invalid email ID or one cannot get access to it. In such case Request for intimation u/s 143(1), this option under head my account can be accessed and details can be received.

For some reason it so happens that one cannot request intimation u/s 143(1) due to earlier request still pending with CPC.

(Note: This happens due to system errors which have not been solved even now).

In this case the assessee does not have any information so as to file Refund reissue request.

The only option that is left is to call the CPC cell which looks after refunds request and ask them to put a system request for intimation from their side.

(Note: This request cannot be seen in my request list, hence there is no proof for the request. But my personal experience is you receive the intimation or order in your registered email-id in 5-7 working days)

Intimation u/s 245:

I will say this is the talk of the town as most of the assessee have been showered with this letter from the ITO on a regular basis. This is auto generated mail from CPC and send at interval of 45-60 days asking to respond to the tax demand. Issue is not the letter but the list of demand outstanding and a subsequent refund adjustment that is done against the demand.

( Note: One needs to understand that the demand raised u/s 245 is only the actual demand and no interest or penalty accumulated till date have been integrated)

The demand raised u/s 245 can be found online under

My Pending Action ------- Response to outstanding tax demand after logging into income tax site.

The demands raised is a combination of old demand (offline return) and new demand (online returns). There are lot of demand amongst those that an assessee feels have already been sorted out manually by approaching the Jurisdictional A.O, still the same was listed amongst the demand in Intimation u/s 245. The reason being is that when system changed and all things started getting integrated on Online portal from manual working, lots of demand which were sorted earlier were still listed online.

How to solve the demands listed in Intimation u/s 245

Online demands whose rectification rights is still with CPC can be solved as explained above in the article. In case of offline demand , there is a procedure listed in the intimation u/s 245 itself on how to respond to outstanding tax demand and nullify it. My personal experience has been inspite of submitting online the demand still stands due to unknown reasons.

Another way to approach this situation is the old way of dealing with it. You need to visit the Jurisdictional A.O and submit the required documents with them and ask them to remove the demand from the system. IF one goes through the outstanding demand list, at times you may find a green arrow pointed adjacent to the demand amount. When you click on it a pdf file is downloaded and a computation sheet is uploaded by your A.O. It is not a notice but the computation of ITO to arrive at the demand. Incase the assessee has the computation sheet he can take that calculation as a base to submit the required working to the A.O.

If reply is not given within 30 days, it is possible that any upcoming refund would be adjusted with the demand outstanding. In that case, to get refund back the assessee need to nullify the demand of the A.Y with which the refund is adjusted and then put a request for the refund.

Please Note: At few places inputs have been taken from Income Tax E-filing Website.

CAclubindia

CAclubindia