GST has its own system which can calculate the difference between the GSTR 3B and GSTR1 or GSTR 3B and GSTR 2A.

It's a inter link system which can automatically find the difference in any Return and help GSTIN to find out the individual for the same.

It’s an easy and simple task to reconcile your returns you have to just keep in mind what amount of tax liability you had created and paid in GSTR 3B and what amount of input tax credit(ITC) you had claimed in GSTR 3B.

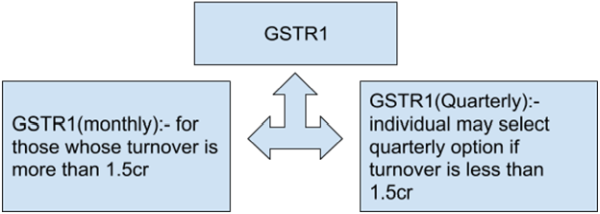

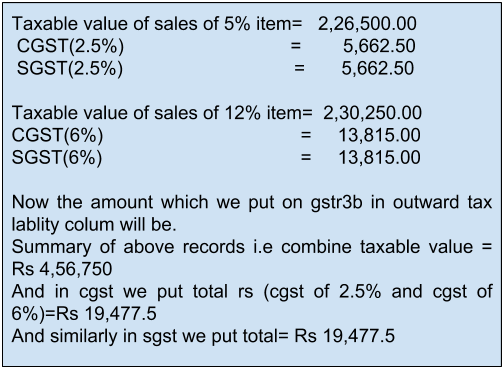

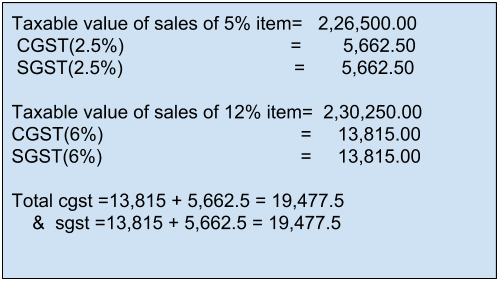

GSTR1 (Monthly): it’s easy to match your monthly GSTR 1 with your monthly GSTR 3B. GSTR 3B consist of summary report of your monthly sales and monthly purchase. To do matching with GSTR 1 you only have to consider your outward sales value which you had entered in GSTR 3B. For example from 1st Sep, 2018 to 31st dec 2018. You had a sales of rs 4,56,750(taxable value) this value consist of two or more gst rate items suppose 5% and 12% so now suppose out of rs 4,56,750. Rs 2, 26,500 are of 5% and balance is of 12%.

So taxable value

Now in GSTR 1 (monthly)

We have to put details of sales with invoice no.

If you had a B2B sales, then put along with buyers gst no.

If you had a B2C large invoice i.e. invoice having more than rs 50,000 in value. Use buyers pan card details.

If you had B2C small invoice then you can fill the total value of taxable amount for example:-

******See this will automatically match with your GSTR 3B

In case you are filing GSTR 1(quarterly) then similarly above define GSTR 3B will be calculated three times after that all process is same and your GSTR 1 will definitely match with your GSTR 3B.

Consequence of not filing or not matching of GSTR 1 and GSTR 3B:

Practical Consequences: Credit of taxes paid by the recipient to the Supplier shall be available to the recipient only if the Supplier has furnished the details of the same in the GSTR 1 and paid the requisite monthly taxes to the Government. Also the recipient can take credit only after he accepts the credit in GSTR 2 which shall happen after the Supplier has disclosed about the recipients share of GST in his GSTR 1. Hence if one of them does not file the return then the Input Tax Credit shall not be available and this shall lead to break in Input Tax Credit chain. Also if the Supplier does not file the returns, the recipient won't be able to take the Input Tax Credit and hence would restrain from doing business with that particular Supplier.

Late fee of rs 100 will be incurred from due date till filing date max fine upto rs5000.

Govt. can scrutinize your portal or can hold an audit on your business.

Penalty for GSTR 3B rs50 in case of any liability or in case of nil return rs 20 from due date till the date of filing return. Fine extended to rs 5000 each cgst and sgst.

GSTR 2A:

It’s auto populated system in which seller after completing his GSTR 1 it get automatically appear in the buyer’s portal under GSTR 2A. You can check your purchase in this head.

It’s easy to match your purchase of GSTR 3B with GSTR 2A

Suppose you are filling your GSTR 3B in which you had claimed input tax credit (ITC) of rs 78,750 under cgst and rs 78,750 under sgst. Before filing check your GSTR 2A whether total amount you want to claim is matching with GSTR 2A or not.

You can also proceed without checking it may be possible that you are filing your return earlier than your buyer.

This how you can easily check and match your GSTR 1, GSTR 2, GSTR 3B.

CAclubindia

CAclubindia