Purchasing a property in India is fast becoming a nightmare. We're not even going into the intricacies of the Real Estate market (the high prices, real estate bubble, liquidity crisis- all of this is for another post).

Say you managed to locate a property you like, have an agreement in hand. What about the taxes?

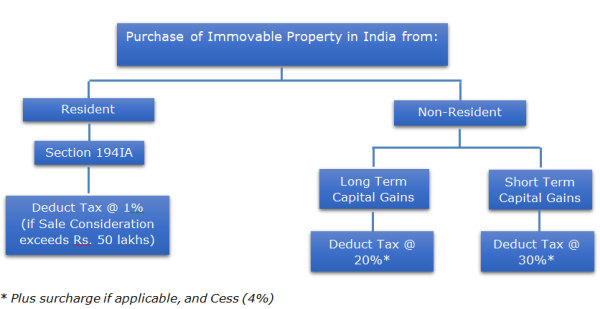

Let's deal with Income Tax first - TDS liability

Practical Considerations:

While the above chart explains the legislative provisions, the real world throws up some interesting propositions. Some of the practical issues faced by our clients in the past have included:

Section 194IA was introduced in 2012, what if the payment schedule of the property is as follows:

December 31, 2011 - INR 80 lakhs

July 24, 2019 - INR 5 lakhs

May 11, 2020 - INR 5 lakhs

Total - INR 90 lakhs

Should the assessee pay TDS? The assessee paid the major portion before the introduction of the aforesaid provision.

Quite often, developers have split the Purchase Consideration between land and building. What happens if the land is worth INR 40 lakhs and building worth INR 20 lakhs? In aggregate the total amount exceeds INR 50 lakhs, however considering the 2 agreements separately, the provisions of Section 194IA are not triggered. What happens in case of disputes where the tenant does not pay rent but does not vacate the property either?

If you buy a property from an NRI, you have to deduct tax at 20% or 30% (plus surcharge and cess) depending on whether it is short term capital asset or long term capital asset. How would you be able to determine what the seller's holding period is?

None of these have any defined answers and would depend on the facts of each specific case.

Frequently Asked Questions:

1. NRI purchases property on November 1, 2019 from a Resident Indian for a Sale Consideration of INR 70 lakhs. Are there any tax obligations for the NRI at the time of purchasing property?

In the above scenario, the sale consideration exceeds INR 50 lakhs. Therefore, as per Section 194IA of the Act, NRI will have to deduct tax @ 1% and deposit the same in the Government Treasury in the form of challan cum statement (Form 26QB) within 30 days from the end of the month of deduction of tax.

In addition, he has to produce a certificate of such tax deduction in the prescribed form to the Resident within 15 days from due date of furnishing the challan cum statement as above.

2. An assessee purchased a property worth INR 80 lakh from a Resident Indian on February 5, 2012. Is he required to deduct tax before making the payment to the Resident?

Section 194IA of the Act which provides for 1% deduction of tax is applicable w.e.f. June 1, 2013. Accordingly, in the above situation, the assessee is not liable to deduct tax before making the payment.

3. NRI purchases a property from a Builder in India on installment basis. The following is the payment schedule for the property:

- July 17, 2016 - INR 20 lakh

- October 2, 2016 - INR 35 lakh

- February 5, 2017 - INR 35 lakh

Is NRI liable to deduct tax on the aforesaid payments to the Builder?

In the above case, aggregate consideration payable by NRI exceeds INR 50 lakh. Therefore, NRI must deduct tax @ 1% on payment of each installment to the Builder (irrespective of the individual installment amounts not exceeding INR 50 lakh).

4. Will the assessee be required to obtain a Tax Deduction Account Number (TAN) for facilitating the tax deduction?

No, he is not required to obtain a TAN. He can facilitate tax deduction on the basis of his PAN, provided he is selling the property to a Resident Indian.

However, in case the NRI is selling the property to another NRI, he will have to obtain a TAN to deposit the amount of tax deducted by him.

5. What is the procedure for paying such tax deducted into the Government Treasury in the above case?

The assessee shall need to follow the below steps:

• Step 1: Fill in an online challan cum statement (Form 26QB) through which he can make an online payment.

• Step 2: A Challan Identification Number shall be generated once the payment has been successfully made.

• Step 3: Register himself on the TRACES website as a tax payer and generate Form 16B as a certificate for tax deduction.

• Step 4: Form 16B shall have to be shared with the Seller of the property.

Other things to keep in mind:

Coming to the GST liability - GST at 5% will have to be paid if the property is under-construction. If the property is fully constructed, there is no GST.

Last bit is the Stamp Duty and Registration fees. This varies from state to state. For eg., for a property purchase in Mumbai, Stamp duty is 5% and registration fee is INR 30,000.

In case you need any additional information, feel free to visit our website - https://www.thegalacticadvisors.com/ or write to us at support@thegalacticadvisors.com.

CAclubindia

CAclubindia