REMOVAL OF AUDITOR

PROCESS TO REMOVAL OF AUDITOR UNDER COMPANY ACT- 2013

In my last Article I gave the procedure for Appointment of Auditor under Companies Act- 2013. Under my this article am trying to give procedure for Removal Auditor.

The Ministry has taken a big step by notifying 183 major sections of Companies Act, 2013 w.e.f. 01.04.2014 out of which the provisions relating to Audit & Auditors is of utmost importance for all the Chartered professionals out there. This article contains the provision relating to Removal of Auditors. Section- 140 of Companies Act talks about Removal of Auditor: - This section corresponds to Section 225 of the Companies Act. The Section seeks to provide for the provisions for removal of auditor before the expiry of his term.

The Board of Directors of the company has no power to remove an auditor (Individual or Firm) appointed by the company in General meeting before the expiry of his term.

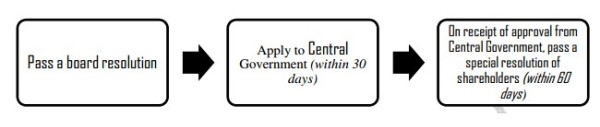

Removal by Special Resolution and previous approval of the Central Government: [Sec 140(1)]:

Sub-Section (1) provides that the removal of an Auditor before the expiry of his term requires-

• The previous approval of Central Government (CG). Form of Application will be made in form-ADT-2. Form ADT-2 and shall be accompanied with fees as provided for this purpose under the Companies (Registration ffices and Fees) Rules, 2014. [Rule 7(1) of the Companies (Audit and Auditor) Rules, 2014} (Attached in form GNL-2).

• The auditor appointed under section 139 may be removed from his office before the expiry of his term only by a SPECIAL RESOLUTION of the company,

• Before taking any action, the auditor concerned shall be given a Reasonable Opportunity Of Being Heard.

• The application to Government shall be filed within 30 days from the date of resolution of the Board along with fees;

• The company need to hold General Meeting (EGM) within 60 (Sixty) days of the approval of Central government.

The auditor may be removed by the company before the expiry of his term. However, the removal of the auditor will require the following steps:

• Removal of Auditor by Special Resolution will be considered as Special business for Section-102.

• Here, a long-term relationship is built for 5 years, since removal before 5 years would be considered as removal before the expiry of his term. And for removal before the expiry of an auditor’s term requires strict formalities to be followed.

Example: M/s ABC & Co. is an auditor of Tata Ltd. Company wants to remove M/s ABC & Co. in December, 2017. Company has to obtain previous approval of CG & also has to follow other procedures prescribed

u/s 140(1)

Form ADT – 2:

Form ADT – 2 require following information:

• Details of the application clearly indicating the grounds for seeking removal of auditor.

• Whether the accounts have been qualified during last three years (if yes, give details)

• Details of opportunity given to auditor concerned for being heard

• Whether any civil or criminal proceedings are pending between the company and the concerned officers. Yes / No. If yes, give complete details.

• Date of appointment of the concerned auditor and SRN of notice of his appointment and period for which the auditor was appointed.

• Whether any special notice has been received for removal of auditors. Yes or No. If yes, the date of receipt of notice and the percentage of capital held by the members giving such notice or percentage of the number of members in case of company limited by members.

• Whether all due audit fee has been paid to the concerned auditors. If no mention the amount of arrears.

• Details of other services been rendered by such auditors to the company.

• Pendency of Audit i.e, number of financial years for which audit is pending.

• Stage of accounts of the company for each of such financial year i.e, yet to be approved by the Board or approved by the Board but yet to be handed over to auditors or approved by the Board,handed over to auditors but audit not yet completed or audit completed, draft report not yet given by the auditors.

• Whether there is any dispute with regard to the Books of Accounts in the possession of auditors but not delivered back to the company. Yes or No.

Resignation by Auditor:-

Compliance by Auditor After Resignation : The auditor who has RESIGNED FROM the company shall file within a period of 30 days from the date of resignation, a Statement in the Form No. ADT-3 (Attached in GNL-2) with the company and the ROC, indicating the reasons and other facts as may be relevant.

• In case of other than Government Company, the auditor shall within 30 days from the date of resignation, file such statement to the company and the registrar.

• In case of Government Company or government controlled company, the auditor appointment under sub-section (5) of section 139, shall within 30 days from the resignation, file such statement to the company and the Registrar and also file the statement with the Comptroller and Auditor General of India (CAG).

The form and content of the statement to be filed by the retiring auditor shall be prescribed by way of rules. The onus to file such statement containing relevant facts and reasons for resignation is on the resigning auditor and any contravention of sub section (2) is punishable with monetary fine which could be minimum Rs. 50,000 and Maximum Rs. 5 lakh.

Form ADT – 3 require following information:

1. Category of Auditor Individual Firm:

• Income Tax PAN of auditor or auditor’s firm

• Name of the auditor or auditor’s firm

• Membership Number of auditor or auditor’s firm’s registration number

• Address of the auditor or auditor’s firm

• City

• State

• Pin code

• Email id of the auditor or auditor’s firm

2. Reasons for resignation

3. Whether letter of resignation is attached Yes/No

4. Any other facts relevant to the resignation

MCA’S LATEST MOVE:

MCA vide general circular dated 4 April 2014 has clarified that the financial statements (and documents required to be attached thereto), auditor’s report and board’s report in respect of financial years that commenced earlier than 1 April 2014 will be governed by the relevant provisions/ Schedules/ Rules of the Companies Act, 1956. ICAI vide announcement dated 8 April 2014 has also stated that the auditor’s report pertaining to financial year commencing on or before 31 March 2014, would be in accordance with the requirements of the Companies Act, 1956 even if that financial year ends after 1 April 2014, e.g., where the financial year of a company is 1 January 2014 to 31 December 2014, the auditor’s report would be in accordance with the Companies Act, 1956. As a corollary to MCA’s general circular, the Companies Act, 2013 Act would apply only to the financial years commencing on or after 1 April 2014, e.g., the auditor’s report in respect of the financial year ended 31 March 2015 would need to be issued in accordance with the provisions of the Companies Act, 2013.

(References: The Companies Act, 2013, the Companies Act, 1956, draft Rules on Chapter X ‘Audit and Auditors’, the Companies (Audit and Auditors) Rules, 2014, MCA General Circular 08/2014 dated 4 April 2014, ICAI clarification on MCA circular, ICAI Code of Ethics and PIB press release).

Disclaimer: The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Though utmost efforts has made to provide authentic information, it is suggested that to have better understanding kindly cross-check the relevant sections, rules under the Companies Act, 2013. The observations of the author are personal view and the authors do not take responsibility of the same and this cannot be quoted before any authority without the written consent of the author

SUGGESTIONS, COMMENTS AND QUERIES SOLICITED

Regards,

CS Divesh Goyal

ACS-35817

CAclubindia

CAclubindia