PREFACE TO INTERNATIONAL FINANCIAL REPORTING STANDARDS

PURPOSE OF ISSUING PREFACE

a. Setting out objectives and due process of the IASB

b. Explain the scope, authority and timing of application of IFRS

c. Preface has been amended from time to time since its approval in the year 2002 by the IASB

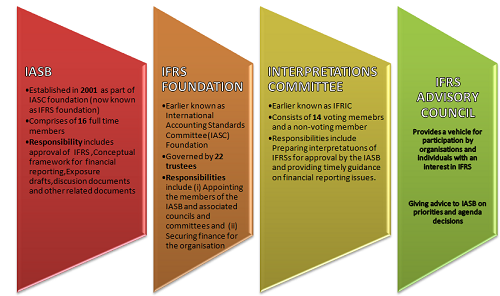

VARIOUS BODIES CONSTITUTED FOR GOVERNANCE OF IFRS

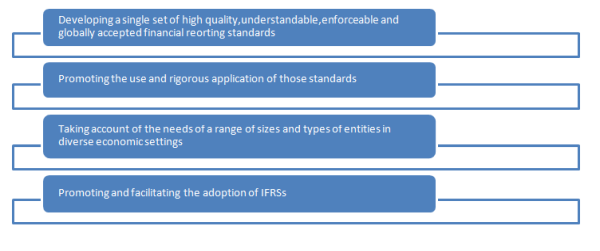

OBJECTIVES OF THE IASB

SCOPE AND AUTHORITY OF IFRS

a. In developing IFRSs, the IASB, works with national standard-setters to promote and facilitate adoption of IFRSs through the convergence of national accounting standards and IFRSs.

b. IFRSs set out recognition, measurement, presentation and disclosure requirements dealing with transactions and events that are important in general purpose financial statements. They may also set out such requirements for transactions and events that arise mainly in specific industries.

c. IFRSs are designed to apply to the general purpose financial statements and other financial reporting of profit-oriented entities. Although IFRSs are not designed to apply to not-for-profit activities in the private sector, public sector or government, entities with such activities may find them appropriate. The International Public Sector Accounting Standards Board (IPSASB) prepares accounting standards for governments and other public sector entities, other than government business entities, based on IFRSs.

d. IFRSs apply to all general purpose financial statements and hence useful to users making economic decisions

e. In the interest of timeliness and cost considerations and to avoid repeating information previously reported, an entity may provide less information in its interim financial statements than in its annual financial statements. IAS 34 Interim Financial Reporting prescribes the minimum content of complete or condensed financial statements for an interim period. The term ?financial statements? includes a complete set of financial statements prepared for an interim or annual period, and condensed financial statements for an interim period.

f. The IASB?s objective is to require like transactions and events to be accounted for and reported in a like way and unlike transactions and events to be accounted for and reported differently, both within an entity over time and among entities. Consequently, the IASB intends not to permit choices in accounting treatment. IASB has reconsidered, and will continue to reconsider with the objective of reducing the number of those choices.

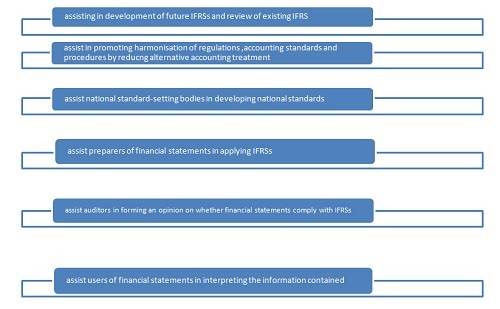

g. Interpretations of IFRSs are prepared by the Interpretations Committee to give authoritative guidance on issues that are likely to receive divergent or unacceptable treatment, in the absence of such guidance.

h. IAS 1 includes the following requirement:

An entity whose financial statements comply with IFRSs shall make an explicit and unreserved statement of such compliance in the notes. An entity shall not describe financial statements as complying with IFRSs unless they comply with all the requirements of IFRSs.

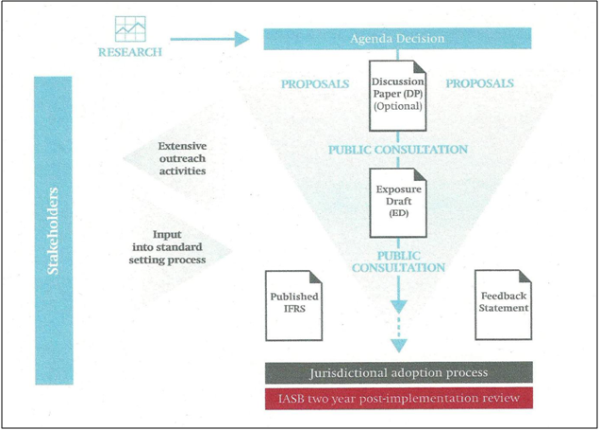

DUE PROCESS OF IFRS i.e. the Standard Setting Process

International Financial Reporting Standards (IFRSs) are developed through an international consultation process, the "due process", which involves interested individuals and organizations from around the world.

The due process comprises six stages:

1. Setting the agenda

2. Planning the project

3. Developing and publishing the discussion paper

4. Developing and publishing the exposure draft

5. Developing and publishing the standard

6. After the standard is issued

Timing of application of International Financial Reporting

Standards

IFRSs apply from a date specified in the document. The IASB has no general policy of exempting transactions occurring before a specific date from the requirements of new IFRSs. The IASB believes the fact that financial reporting requirements evolve and change over time is well understood and would be known to the parties when they entered into the agreement.

The Conceptual Framework for Financial Reporting

INTRODUCTION

a. The Conceptual Framework was issued by the IASB in September 2010. It superseded the Framework for the Preparation and Presentation of Financial Statements.

b. The IASB is currently in the process of updating its conceptual framework.

c. Financial statements are prepared and presented to external users by many entities around the world. Although such financial statements may appear similar from country to country, there are differences caused by a variety of social, economic and legal circumstances. These different circumstances have led to the use of a variety of definitions of the elements of financial statements: for example, assets, liabilities, equity, income and expenses. The International Accounting Standards Board is committed to narrowing these differences by seeking to harmonize regulations, accounting standards and procedures relating to the preparation and presentation of financial statements.

PURPOSE AND STATUS

This Conceptual Framework is not an IFRS and hence does not define standards for any particular measurement or disclosure issue. Nothing in this Conceptual Framework overrides any specific IFRS.

The Conceptual Framework deals with:

(a) the objective of financial reporting;

(b) the qualitative characteristics of useful financial information;

(c) the definition, recognition and measurement of the elements from which financial statements are constructed; and

(d) concepts of capital and capital maintenance.

CAclubindia

CAclubindia