Introduction

To summarise in a few words, DVR shares are merely the same shares of a company, having, mutatis mutandis, all the rights and privileges that are vested in the ordinary shares of the Company, except as to voting and in some cases, dividends.

The Difference

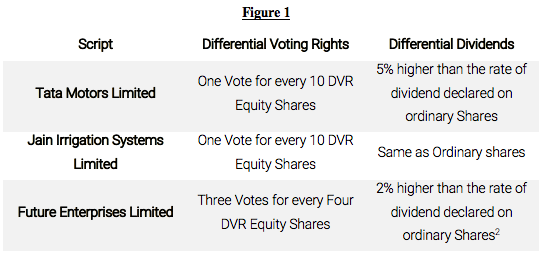

In India, a company can only issue DVR, a.k.a. Differential Voting Rights, shares that offer fewer voting rights than ordinary shares of the same company. The holders of the equity shares with differential rights enjoy all other rights such as bonus shares, rights shares etc., which the holders of ordinary equity shares are entitled to.

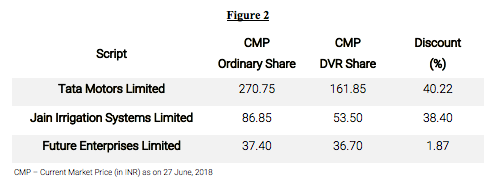

Historically, the discount between the ordinary shares and DVR shares of public limited companies in India has been between 35- 45%. However, as shown in figure 2, this discount has narrowed considerably for Future Enterprises Limited in recent times.

Returns

Since the listing of DVR shares, ordinary shares of Tata Motors Limited have given a return of approximately 763%, whereas its DVR shares have only returned 185%. Similarly, for Jain Irrigation Systems Limited, the ordinary shares have returned -32.96% whereas the DVR shares have yielded 2.6%.

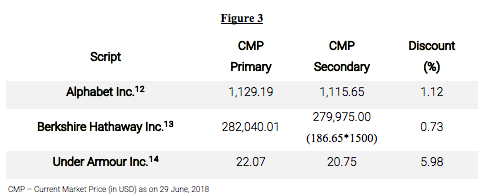

Ideally, the movement in the two shares, i.e. ordinary share and DVR share, should mirror each other. However in India, on an average, only 63.83% of the returns of DVR shares is explained by returns of the ordinary shares. In the US, returns of Alphabet Inc’s Class A stock explains 98.14% of the returns of the Class C stock, where Alphabet Inc’s Class A share has gained 2027% and its class C share has given a return on 2002%

A possible explanation for this mismatch is that the DVR stocks of Indian listed public companies are not understood and tracked by Investors.

Legal Framework

The regulatory environment in India requires fulfillment of certain strict requirements, with a high bar for corporate governance, to issue shares with differential voting rights.

For instance, under the 2014 rules, the shares with differential rights cannot exceed twenty-six percent of the total post-issue paid up equity share capital including equity shares with differential rights issued at any point of time. Similarly, to issue DVR shares, the company should have a consistent track record of distributable profits for the preceding three years of such issue. A company should also not have been penalised by any sectoral regulators such as SEBI, RBI, etc.

Moreover, various provisions of the Companies Act 2013 protect the rights of shareholders belonging to a different class. For instance, Section 48 states, inter alia, that the rights attached to the shares of any class may be varied with the consent in writing of the holders of not less than three-fourths of the issued shares of that class or by means of a special resolution passed at a separate meeting of the holders of the issued shares of that class. Therefore, it can be inferred that the shareholders of the DVR shares, in effect, have an absolute vote in cases where any of the rights of such shareholders are varied.

Valuation

If the primary reason for the voting share premium is the expected value of control, in general, there are two ways by which we can value DVR shares. First, we can use the empirical findings on the voting share premium in markets and arrive at a reasonable value for voting rights. Second, it can be said that the voting right premium is an extension of the expected value of control and that estimating that value should allow us to quantify the premium.

The expected value of control is the product of the probability of control changing the value of changing management at a firm:

Expected value of control = Probability of management changing * Value of management change

Where, Value of management change = Optimal firm value-Status quo value

As regards difference in voting rights, Damodran (2008) states that:

- The difference between voting and non-voting shares should go to zero if there is no chance of changing management/control

- Other things remaining equal, voting shares should trade at a larger premium on nonvoting shares at badly managed firms than well-managed firms

- Any event that illustrates the power of voting shares relative to non-voting shares is likely to affect the premium at which all voting shares trade

- Other things remaining equal, the smaller the number of voting shares relative to nonvoting shares, the higher the premium on voting shares should be

According to Nenova (2003), the value of control-block votes is expected to decrease with the strictness of the legal environment. In particular, such strictness includes better general investor protection, higher quality of law enforcement, and stricter takeover laws.

Global Scenario

In a comparative study of voting premiums across 661 companies in 18 countries, it was found that the median value of control block votes varies widely across the countries, ranging from less than 1% in the US to 25% or greater in France, Italy, Korea, and Australia.

Lease, McConnell, and Mikkelson (1983) found that voting shares in the United States trade, on average, at a relatively small premium of 5- 10% over non-voting shares. They also found extended periods where the voting share premium disappeared or voting shares traded at a discount to non- voting shares.

The legal environment is the key factor in explaining differences across countries and the voting premium is smaller in countries with better legal protection for minority and non-voting stockholders and larger for countries without such protection.

Only recently, with the increase in dual-class structures in the technology sector worldwide, Singapore and Hong Kong have allowed companies with dual-class share structures to list on their respective stock exchanges.

Conclusion

The regulatory framework in India protects the rights of the dual class shareholders, as well as the minority shares. For example, in the United States, Berkshire Hathaway Inc. Class A equity shareholders can convert their shares into class B equity shares, having fewer voting rights. However, under the Indian Law, a company cannot convert its existing equity share capital with voting rights into equity share capital carrying differential voting rights and vice versa.

Considering the strict corporate governance requirements for Companies to list dual-class shares in India and the various laws protecting the rights of DVR shareholders against hostility, it can be argued that the discount of 35- 45% for DVR shares is a bit excessive. This might be partly explained by the fact that these shares are not understood and tracked by Investors, and that we might see the discount narrowing once there is more awareness about the features of such shares in the market.

Disclaimer: The views expressed here are solely those of the author in his private capacity and do not in any way represent the views of SKI Capital Services Limited. The research is not intended to be an investment recommendation. The author has financial interest in the Indian entities mentioned in this report.

CAclubindia

CAclubindia