Republished with updates till July 2018

In Simple words, Deferred Tax Liability is a Provision for Future Taxation.

This is in stark Contrast to Provision for Taxation. Provision for Taxation is basically a provision for Current year Taxation.

Deferred Tax Liability arises due to timing difference in the value of Assets as per Books of Accounts and as per Income Tax Act.

The derivation of the Book Profits (BP) is done from the accounting or financial statements prepared in accordance with Companies Act, 2013 and Taxable Profits (TP) is calculated based on provisions of the Income-tax Act, 1961.

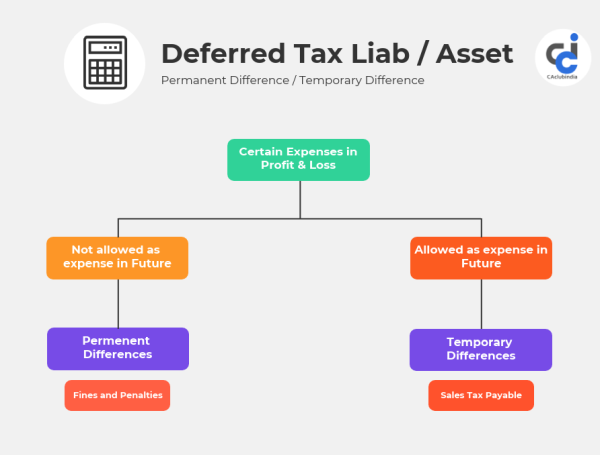

Difference between the BP and TP arises because of various items which are specifically allowed and disallowed for taxation purposes. The difference between the books and the taxation income or expense is known as Timing difference which can be classified either as:

1. Temporary Difference – All the differences between BP and TP capable of reversal in subsequent period.

2. Permanent Difference – All the differences between BP and TP which are not capable of reversal in subsequent period.

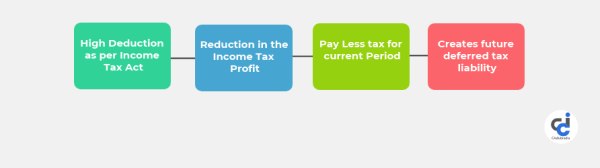

Depreciation is the main reason for difference in the profits as per books of Accounts and Taxable profits as per Income Tax Act. Both Income Tax Act and Companies Act prescribe different rates of Depreciation for different categories of Assets.

Let me illustrate with a simple example. Suppose a Company purchases a Wind Turbine Generator (Windmill). The Depreciation which can be claimed in the Books of Accounts in as per Companies Act is let's say 20% (assumed). The Depreciation as per Income Tax Act is 80% for Windmill.

Now a Windmill is purchased for Rs. 10,00,00,000/- (10 Crores). The Depreciation Claimed in the First year is:

| Value of Windmill: | 10,00,00,000/- | |

| Depreciation as per Books of Accounts: | 10,00,00,000 X 20%= | 2,00,00,000/- |

| Depreciation as per Income Tax Act: | 10,00,00,000 X 80%= | 8,00,00,000/- |

| DIFFERENCE |

|

| DEFERRED TAX LIABILITY @ 30.9% | -1,85,40,000/- |

(Deferred Tax Liability is created at the highest Marginal Rate of Tax i.e. 30.9%)

What is the Meaning of Creating this Deferred Tax Liability of Rs. 1,85,40,000/- (One Crore eighty five lakhs forty thousand)

It simply means that the company will definitely have a tax Liability of that much in the future years. This is because in the years to come the Depreciation as per Income Tax Act will be lesser that the Depreciation as per Books of Accounts. Hence in these years the Company will have to create a Deferred Tax Asset

For clarity the Following Table is provided. Let's take the figures in Lakhs for Easier Understanding:

Let Windmill Value be Rs. 100,000/-

| Year | 1 | 2 | 3 | 4 | 5* | TOTAL |

|

Dep as per IT Act (80% OF WDV) |

80,000 | 16,000 | 3,200 | 640 | 160 | 100,000 |

|

Dep as per Books (20% SLM) |

20,000 | 20,000 | 20,000 | 20,000 | 20,000 | 100,000 |

| DIFFERENCE | 60,000 | -4,000 | -16,800 | -19,360 | -19,840 | 0 |

| DTL/DTA @ 30.9% | 18,540 | -1,236 | -5,191.20 | -5,982.24 | -6,130.56 | 0 |

Note * In year 5 as per Income tax act let's assume the entire Remaining Balance is written off

To summarise the general understanding, these deferred taxes are given effect to in the financial statements through Deferred Tax Asset and Deferred Tax Liability in the following manner:

|

Serial. No. |

Profit Status |

Current Scenario |

Future Scenario |

Final Effect |

|

1. |

BP greater than the TP. |

Pay lower tax now |

Pay higher tax in future |

Creation of Deferred Tax Liability (DTL) |

|

2. |

BP is lower than the TP. |

Pay higher tax now |

Pay lower tax in future |

Creation of Deferred Tax Asset (DTA) |

CONCLUSIONS:

1. In Year 1 Deferred Tax Liability amounting to Rs. 18,540/- has to be created. This means that in Year 1, the company has postponed its tax Liability of Rs. 18,540/- to the Future years. This Liability will come back to the company one day or the other. (Unless 80 IA is claimed)

2. In Year 2, as you can clearly see the Depreciation as per Books has gone up. This means that Depreciation as per IT act will be lesser as a result the profit as per IT Act will be more and as a result the company has to pay Rs. 1236/- more tax during this year.

3. Thus in the remaining years the company will have Deferred Tax Assets And the Deferred Tax Liability created in the first year will be reversed in the subsequent 4 years.

4. Thus when the WDV of Assets as per Books and WDV as per IT Act both become ZERO, there is neither Deferred Tax Liability nor Deferred Tax Asset as there is no timing Difference

Deferred Tax is purely an accounting Concept. AS 22 - "Accounting for Taxes on Income deals with Deferred Tax.

The following are the Accounting treatment and Tax treatment of Deferred Tax:

ACCOUNTING ENTRIES:

| P&L A/c Dr | 18,540.00 | ||

| To Deferred Tax Liability A/c | 18,540.00 |

(Being Deferred Tax Liability created in Year 1 at the Maximum Marginal Rate of Tax)

Deferred Tax is shown under Provisions in Balance Sheet.

| Deferred Tax Asset Dr | 1,236.00 | |

| To P & L A/c | 1,236.00 |

(Being Deferred Tax Liability Reversed in Year 2)

Finally at the end of Year 5 the Balance Sheet will be thus:

|

PROVISIONS: Deferred Tax Liability |

18,540 |

Rs.Ps | |

| Less: Reversed upto year 4 | 12409.44 | ||

| Reversed in year 5 | 6130.56 | 18,540 | 0 |

TAX TREATMENT:

|

INCOME FROM BUSINESS: Net Profit as per P&L A/c |

XXX | |

| Add: Deferred Tax Liability | XXX | |

| Less: Deferred Tax Asset | XXX |

Note: As Deferred Tax Liability is a Provision, it should be disallowed as an expense. Also deferred tax asset should be deducted from Income.

As seen from the above, deferred tax liability/asset does not affect tax computation.

Important Case Law:

There are controversies if deferred tax liability debited to P&L should be added to the Book Profits for the purpose of MAT calculation u/s 115JB. Kolkata Tribunal in Balrampur Chini’s case has held that the deferred tax liability should not be added back whereas the Chennai Tribunal in Prime Textiles Ltd’s case has held otherwise.

The view taken by Kolkata Tribunal in Balrampur Chini’s case was referenced and hence upheld in the case of M/S. Indo Rama Synthetics Ltd. vs DCIT, New Delhi on 31 January, 2018.

An issue that comes up consistently is that whether MAT credit can be considered as a deferred tax asset per AS 22?

According to AS22, deferred tax asset and deferred tax liability arises due to the difference between BP & TP and do not rise on account of tax expense itself. Minimum Alternate Tax (MAT) does not give rise to any difference between BP & TP. Therefore, in accordance with AS 22, it is not appropriate to consider MAT credit as a deferred tax asset.

PURPOSE: The Purpose of DTA/DTL: More appropriate presentation of financial statements and to make the various stakeholders aware of the tax situation of the company.

It may be noted that 80-IA (Section 80 IA of IT Act) exemption may be availed for Windmill. That is if the company starts to claim 80-IA benefit after 5 years (80-IA benefit can be claimed in any 10 Assessment years out of 15 A.Y's after buying windmill), then there will be more benefits to the company as the Income in the first 5 years will be low and the company can claim business loss as there will be huge Depreciation as per IT.

PART II: In the next part, I will explain the how deferred tax should be computed if 80-IA exemption is availed for Windmill having useful life of more than 5 years. Also I will explain the other items which cause a difference in profits as per Books and IT Act. Also I will explain how to deal with brought forward losses.

Deferred Tax Calculator:

https://www.incometaxindia.gov.in/Pages/tools/deferred-tax-calculator.aspx

CAclubindia

CAclubindia