GST Law from a Constitutional Perspective

Definition of GST

Article 366(12A)

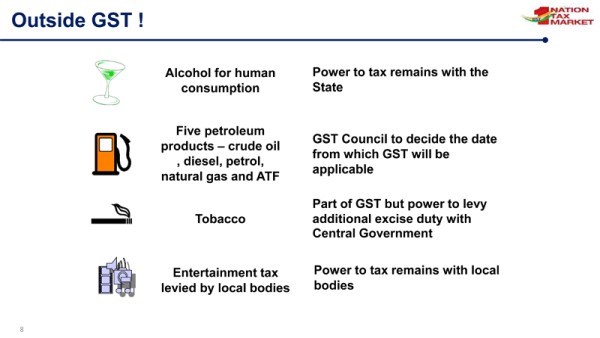

'Goods and services tax' means any tax on supply of goods, or services or both except taxes on the supply of the alcoholic liquor for human consumption

'Goods and Services tax' law while having unique principles, has significant elements of prior Central and State laws; and is also inspired by VAT/GST legislation of EU, Australia, Malaysia etc. along with International VAT/GST guidelines of OECD.

Bill passed by Rajya Sabha on 03.08.2016 & Lok Sabha on 08.08.2016

Notified as Constitution (101st Amendment ) Act, 2016 on 08.09.2016

Key Features:

- Concurrent jurisdiction for levy & collection of GST by the Centre & the States - Article 246A

- Centre to levy & collect IGST on supplies in the course of inter-State trade or commerce including imports - Article 269A

- Compensation for loss of revenue to States for five years on recommendation of GSTC - Clause 19

- GST on petroleum crude, high speed diesel, motor spirit (commonly known as petrol), natural gas & aviation turbine fuel to be levied from a later date on recommendations of GSTC

GST Council - Constitution (Article 279A of the Constitution)

- Chairperson - Union FM

- Vice Chairperson - to be chosen amongst the Ministers of State Government

- Members - MOS (Finance) and all Ministers of Finance / Taxation of each State

- Quorum is 50% of total members

- Decision by 75% majority

- States - 2/3 weightage and Centre - 1/3 weightage

- Council to make recommendations on everything related to GST including laws, rules and rates etc.

To read the full article: Click here

CAclubindia

CAclubindia