ITR forms have been made available for filing on both Online and Java/excel utility.

Below are the key changes that one should keep in mind before filing ITR 1.

1. ITR 1 Applicability:

For individuals being a resident other than not ordinarily resident having Income from Salaries, one house property, other sources (Interest etc.) and having total income upto Rs. 50 lakhs.

2. Non-applicability of ITR – 1 to non-residents:

Non-residents and individuals who are resident but not ordinarily so (RNOR) will now have to file ITR-2/3/4, as applicable.

3. Individual who want to carry forward the loss under the head income from house property is not eligible to file this return.

4. Mandatory requirement to quote Aadhar number or Aadhar Enrolment id (with date and time) in PART A General information Tab.

5. New tab has been provided for declaring amount of late fees under newly introduced section 234F which is payable in case of late filing of ITR.

6. The return will be treated as Defective return in case amounts not matching with Form 16, Form 26AS, etc.

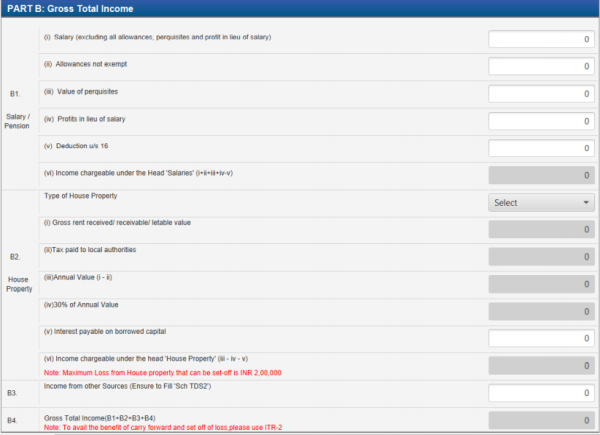

7. Breakup of salary is required to be given:

Details of salary like allowances not exempt, perquisites, profits in lieu of salary and deductions under section 16 are to be provided now.

8. Breakup of Income from House Property:

Details relating to house property income, like tax paid to local authorities, annual value, 30% of annual value, interest payable on borrowed capital are to be provided now.

9. verification column:

In verification, it is mandatory to clear the capacity.

I further declare that I am making this return in my capacity as -

- Himself / Herself could be used if the individual himself/herself is verifying.

- In case the same is being verified by another person, you could say ‘Power of attorney holder’ or ‘Authorised Signatory’

10. Required Document: FORM 16

The author is an upcoming Chartered Accountant, at present working as an Article Assistant in Hyderabad. He is a vivid researcher and regular contributor on Taxation and can also be reached at cavinayreddy@icai.org

CAclubindia

CAclubindia