Over the past two years, there were many concerns surrounding the Indian IT sector. The key amongst them have been slowdown in tech spending in big markets like the US and Europe, the appreciating rupee, and the Satyam scandal. Clients slashed IT budgets and renegotiated vendor contracts. Billing rates fell, thus impacting profitability. Business from the banking, insurance, and financial services (BFSI) segment was the worst hit.

Despite these odds, Indian IT companies showed resilience. They managed to cut costs and improved productivity and efficiency. Companies like TCS and Infosys reported their best margins ever in FY10. All in a period when these companies were expected to perform badly.

This is a lot of information to digest. So, how have the stock markets factored all of this in? How have these stocks fared during this period and where are they headed? Let's study in some detail.

P/E valuations for the pack

In order to understand the performance of IT companies' stocks over the past three years, we have analysed the way their P/E (price to earnings) valuations have behaved.

Everything remaining constant, a stock trades within a particular band. This is based on the stock's underlying company's fundamental value and growth potential. However, significant news or fundamental changes within the sector or the company will cause the P/E band to move either up or down. Policy changes, unexpected financial results, as well as internal problems or restructuring can also make prices move within different P/E bands.

Let's now study how the P/E bands of India's leading IT companies - Infosys, TCS, and Wipro - have behaved over the past three years.

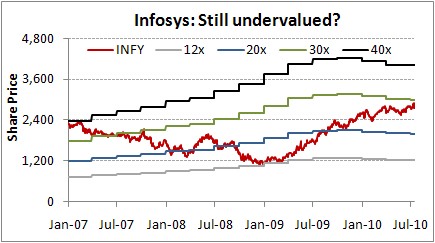

Infosys: As can be seen from the chart below, Infosys's stock was trading within a P/E band of 30-40 times at the start of 2007. This was when the company was doing pretty well, growing in excess of 25%. Since then, and after the global crisis struck the industry, the stock moved down into a lower P/E range of 20-30 times. This was during the period between July 2007 and June 2008. Post the collapse of Lehman Brothers, and the death knell for the global financial industry, the stock moved into an even lower range. It started trading within its lowest P/E range of 12-20 times.

Since then however, the stock has moved up significantly in line with the recovery in tech spending and its own business. It is now trading within the 20-30 P/E range. And it is still below the valuations it commanded way back in 2007! The company recently announced its 1QFY11 results. It even upgraded its revenue guidance for the year.

|

|

and highest P/E traded at within the last 3.5 years (upper band 40x and lower band 11x) ; the middle bands (20x and 30x) have been adjusted based on the above |

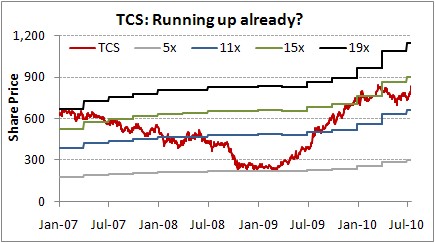

TCS: India's and Asia's largest IT services company, TCS has always been trading at a discount to Infosys. The company followed similar trends to the former in terms of P/E as well. Since 2007, the stock quickly slipped from its high P/E band of 15-18 times to 11-15 times. It fell even lower to the 5-11 times for a long period in 2009. However in the past one year, the stock has been an outperformer. It has jumped up around 117% in the last 12 months. This is due to its positive financial performance. Net profits grew significantly in FY10, even with muted sales growth. The company also significantly improved margins and operating efficiency. The stock has crossed its P/E band of 5-15 times, and is now poised to cross the 19 times barrier.

|

|

and highest P/E traded at within the last 3.5 years (upper band 18x and lower band 5x); the middle bands (11x and 15x) have been adjusted based on the above; the EPS has been adjusted based on its 1:1 bonus issue - Ex date 16th June 2009 |

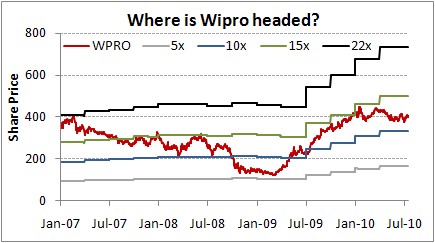

Wipro: Compared to the movement seen in Infosys and TCS, Wipro has been a laggard. One of the reasons for the same is its presence in other businesses including consumer products and lighting. The company saw a similar pattern of stock price movement as its peers. The stock has also had a good run so far, running up almost 80% in the last one year. It is currently within the 10-15 times P/E band. Currently it has not shown any movement towards its higher band of 15-22 times (which it was trading at during the early part of 2007).

|

|

and highest P/E traded at within the last 3.5 years (upper band 22x and lower band 5x) , the middle bands (10x and 15x) have been adjusted based on the above; EPS has been adjusted based on its 2:3 bonus issue - Ex date 15th June 2010 |

Conclusion

We believe that the Indian IT sector is fundamentally strong. Companies are waking up to the fact that they need to provide higher end services. There will continue to be strong volume growth from North America, despite some interim pressure in Europe. Spending by the Indian government on ramping up operations through IT services will also benefit these players. The Asia-Pacific region will be a major growth driver. Pressure on billing rates and rising attrition will still be the key issues for the industry.

As far as these companies' stock market valuations are concerned, we believe these are reasonable and not really attractive. The next stage of run up in their stock prices will largely depend on how sustainable is the recovery in their earnings.

CAclubindia

CAclubindia