Introduction of Negative List - Changes in Service Tax law effective 01.07.2012

1. INTRODUCTION

1.1 The Union Finance Minister announced implementation of a new system for taxation of services popularly known as the Negative List while presenting the Union Budget on 16 March 2012 for the fiscal year 2012-2013. The Govt. of India by clause No.143 to 145 of the Finance Bills 2012, had proposed constitutional amendment relating to the service tax law and accordingly said Bills has been received the assent of the president and as a result of which many changes has been taken place in the Finance Act, 1994 and related Service Tax Rules effective 1st day of July, 2012.

1.2 After the enactment of the Finance Bill 2012 on 28 May 2012, Notification was issued on 06 June 2012 notifying 01 July 2012 as the date for implementation of Negative List.

1.3 This would mark a paradigm shift from the way in which the services would be taxed w.e.f., 01 July 2012. That is to say, all services would be subject to service tax unless specified in the Negative List or are specifically exempted from the levy of service tax.

1.4 To implement such a significant change, series of notifications have been issued on 20 June 2012, inter alia, superseding old exemption notifications, introducing new exemptions, amending the manner of valuing services and to determine the import or export of services etc.

1.5 The Central Government has issued a total of sixteen new notifications numbering from 25/2012-ST to 40/2012-ST on 20th June, 2012. These notifications along with two further important notification issued on 29th Jun12 will assist in implementation of new regime of Service Tax based on negative list of services.

Note: All these notifications (dt. 20.06.2012 in particular) shall come into force on the 1st day of July, 2012.

1) 25/2012-ST 20.06.2012 Mega exemption notification

2) 26/2012-ST 20.06.2012 Abatement Notification … to be suitably read with 30/2012 ST 20.06.2012 for reverse charge mechanism

3) 27/2012-ST 20.06.2012 Exemption to services for the official use of foreign Diplomatic Mission

4) 28/2012-ST 20.06.2012 Place of Provision of Services Rules,2012

5) 29/2012-ST 20.06.2012 Exemption on property tax paid on immovable property

6) 30/2012-ST 20.06.2012 REVERSE CHARGE MECHANISM under sub-section (2) of Section 68 of Finance Act to be suitably read with 26/2012 ST 20.06.2012

7) 31/2012-ST 20.06.2012 Exemption to specified services received by exporter of goods

8) 32/2012-ST 20.06.2012 Exemption of services provided by TBI/ST 20.06.2012EP

9) 33/2012-ST 20.06.2012 Exemption to Small Service Providers

10) 34/2012-ST 20.06.2012 Rescinding of certain notifications

11) 35/2012-ST 20.06.2012 Rescinding of notification 32/2007-ST 20.06.2012

12) 36/2012-ST 20.06.2012 Amendment in Service Tax Rules, 1994

13) 37/2012-ST 20.06.2012 Seeks to amend Point of Taxation Rules, 2011

14) 38/2012-ST 20.06.2012 Amendment of Notification 28/2011-ST 20.06.2012

15) 39/2012-ST 20.06.2012 Notification under Rule 6A of Service Tax Rules

16) 40/2012-ST 20.06.2012 Special Economic Zones

17) 41/2012-ST dt. 29.06.2012 à grants rebate of service tax paid on the taxable services which are received by an exporter of goods and used for export of goods

18) 42/2012-ST dt. 29.06.2012 exempts Service provided by the Foreign Commission Agent to Indian Exporters for procuring order subject to fulfillment of certain conditions specified therein

19) 43/2012-ST dt. 02.07.2012 exempts the taxable services provided by the Indian Railways from the whole of service tax leviable thereon, w.e.f. 02.07.2012 up to and including the 30th day of Sep 2012 i.e., for 3 mths (July12 to Sep12)

1.6 Through this document we have made an effort to encapsulate all the relevant and key amendments that would impact the business and transactions. All implications mentioned in this note would be applicable w.e.f., 01 July 2012.

1.7 Hope you would find the document useful and relevant. We would be happy to receive your feedback / valuable advice to enable us to help perform better.

2. Definition of Service

2.1. For the first time since the introduction of service tax law, term ‘service’ has been defined under the Negative list regime to mean “any activity carried out by a person for another for consideration, and includes a declared service”.

2.2. Taxable service provided only in the Taxable Territory shall be taxed. Such determination is to be done in terms of Provision of Services Rules, 2012 (please refer to Chapter 7 of this Note). In this context, Taxable Territory has been defined to mean whole of India excluding state of J&K.

2.3. The term activity has not been defined but a very wide and broad interpretation has sought to be provided. It has been clarified that ‘activity’ could be active or passive and would also include forbearance to act. In this context, agreeing to the ‘obligation to refrain from an act’ or ‘to tolerate an act or a situation’ has been declared to be a service. Therefore, it seems that there is a possibility that following could fall within the scope of service tax net w.e.f., 01 July 2012:

Assignment or novation of a contract for a consideration

Transfer of right to use all types of Intellectual Property (including software)

Agreeing to perform/non-perform in a certain way or manner … i.e., to say non-compete agreements etc.

Payment of fees to non-executive director

2.4. However, following have been clarified to be out of the ambit of term ‘service’

i) Any transaction in money or actionable claim

ii) Transfer of title in goods or immovable property (i.e. sale, gift etc.) or deemed sale as per article 366(29A). However, a dichotomy with regard to dual taxability of software seems to continue.

iii) Services provided under an employer-employee relationship

2.5. In view of the above, an undertaking may like to do an analysis of all revenue/expenses of its companies to ascertain the risk or exposure, if any, of certain transactions or activities falling under tax net on account of the introduction of Negative List.

3. Valuation of Service

Certain significant amendments have also been introduced in the valuation principles of services. Key amendments have been highlighted below:

3.1 Inclusions:

Amount realized as demurrage (or by any other name called) for provision of service beyond the period originally contracted or in any manner relatable to the provision of service.

3.2 Exclusions:

Interest charged or paid on delayed payments

Accidental damages due to unforeseen actions not relatable to provision of service

4. Key Exemptions

Following key exemptions have been provided from levy of service tax:

4.1 Services by way of transfer of a going concern as a whole or an independent part thereof.

4.2 Services received and provided between persons located in a non-taxable territory. For instance, design services provided by SAG to another foreign entity in respect of an Indian project, there should be no service tax implication on SAG. This is in line with current provisions.

4.3 Sub-contractor providing ‘works contract services’ to main contractor in respect of exempt ‘works contract services’. For instance, benefits of exemption for service provided to railway should also be available to sub-contractor - Please refer Para 9 for detailed analysis.

4.4 Benefits available to railways have also been clarified to be available to metro or mono rail - Please refers to Para 9 for detailed analysis.

4.5 Services by way of sponsorship of sporting events organized by specified organizations like national sports federation, association of Indian Universities etc.

5. Works Contract

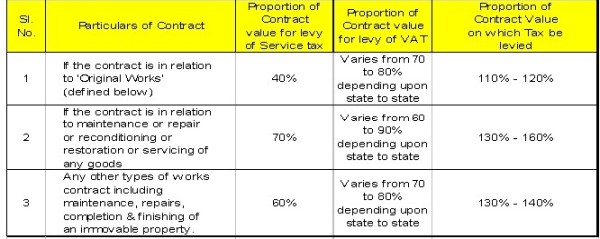

5.1 Composition scheme which permitted payment of service tax @4.94% on total value of contract has been dispensed with.

5.2 Deduction of specified proportion of contract value, depending upon nature of works contract, has been prescribed to discharge service tax.

5.3 Scope of works contract has been extended to even include repair, maintenance, renovation and alteration etc of any moveable or immovable property.

5.4 Following schemes of taxation would now exist as regards taxability of works contract:

5.4.1 Where actual value of property in goods transferred and services provided are determined then respective taxes would apply on the respective values of goods and service.

5.4.2 Where values are not determined as above, then following method should be followed:

5.4.3 In this connection ‘original works’ would mean

All new constructions

All types of additions and alterations to abandoned or damaged structures on land that are required to make them workable

Erection, commissioning or installation of plant, machinery or equipment or structures, whether pre-fabricated or otherwise

5.4.4 From perusal of table at Para 5.4.2 above, it seems that there would be double taxation on certain proportion of contract value of works contract wherein both VAT as well as service tax would be levied.

5.4.5 One of the significant impacts seems to be in case of CAMC’s or AMC’s wherein a comprehensive price is quoted for replacement of parts and spares as well as for provision of services. Further, it is understood that in most cases, it is practically not possible to ascertain the quantum of goods and items supplied.

5.5 Further, no CENVAT credit of specified duties paid in respect of Inputs used in or in relation to works contract would be available. There is no restriction in availing credit on capital goods and input service by the service provider and hence the service provider of the works contract can take credit on capital goods and input service.

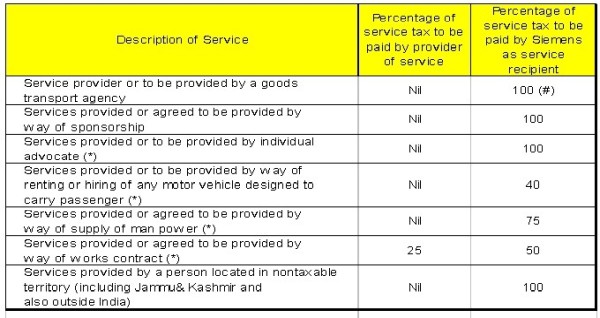

6. Reverse Charge

6.1 Provisions of Section 68(2) are proposed to be amended to empower the Government to also notify the extent and proportion of service tax that needs to be discharged by the person made liable to pay service tax.

6.2 Tabulated below are relevant service transactions towards which service tax needs to be paid under reverse charge basis:

(#) Service tax needs to be paid only on 25% of the invoice Value subject to specified conditions being fulfilled

(*) Services should be provided by an individual, HUF, partnership firm (whether registered or not) including association of persons to a company registered under the Companies Act, 1956 or a business entity registered as a body corporate.

6.3 For the purpose of works contract service, where both service provider and service recipient are liable to pay tax, then each of the persons has the option to choose such method of valuation which might be independent of the other

7. Place of Provision of Services Rules, 2012 (‘PPSR’)

7.1 These Rules will determine the place of provision of service and will supersede Export and Import Rules w.e.f., 1 July 2012.

7.2 As a thumb rule, PPSR provides that ‘place of provision of service’ shall be the location of the service recipient. However, where location of service recipient is not available in the ordinary course of business, it shall be the location of the service provider.

7.3 Certain exceptions have been carved out to the above general principle and the relevant ones have been outlined below:

|

Sl No. |

Scenario/ Situation |

Place of provision of Service |

|

1 |

Where services are provided in respect of goods that are required to be made physically available by the service receiver to the service provider (in order to provide service) |

It will be the place where services are actually performed. Relevant for CAMC’s, installation & Commissioning services. |

|

2 |

Services relating to immovable property |

Place where immovable property is located or intended to be located. Relevant for civil works contract. |

|

3 |

Services relating to events |

Place where the event is actually held |

|

4 |

Services where both provider and recipient of services are located in the taxable territory |

Place of location of the service provider |

|

5 |

Intermediary services |

Location of the service provider |

7.4 With regard to S. No 1 above, please note that said rule shall not apply in case of goods which are temporarily imported into India for repairs, reconditioning or re-engineering for re-export. That is to say, in such a scenario, place of supply should be the location of recipient and should therefore qualify as export if the consideration is received in FE.

7.5 With regard to S No 5 above, please note that ‘Intermediary; has been defined as a broker, agent etc who arranges or facilitates a provision of a service between two persons. Therefore this could impact transactions where SL acts as an intermediary for SAG to canvass certain service business and earns a service fee or any other consideration.

8. Export & SEZ

8.1 The definition of export has been re-defined whereby it states that provision of any service provided or agreed to be provided shall be treated as export when the following five conditions are satisfied:

Provider of service is located in the taxable territory

Recipient of service is located outside India

Place of provision of service is outside India in terms of PPSR

Payment for such service is received in convertible FE

Rebate of service tax or duty paid on input services or inputs on providing such services is still available.

8.2 The procedures for claiming service tax refund/exemption for any services provided to an SEZ, has remained unchanged, the benefit of refund of CENVAT credit on input and input services should be claimed by the service provider.

8.3 Exemption to services provided to SEZ shall continue (subject to the condition that Form A-1 is provided by the SEZ customer). In addition, service provider shall be entitled to avail full credit of CENVAT credit in respect of inputs or input services used for providing services to SEZ.

Procedural tips (w.e.f., 01.07.2012) …

1.Earlier, all ‘taxable services’ whenever provided or proposed to provide first time, needs to be endorsed in the registration certificate for the reasons all services were having different classification numbers (more than 120 in numbers), but now there in only one head / classification i.e. 65B(44) of the Finance Act, 1994.

Since w.e.f., 01/07/2012, the definition of ‘Service’ has been changed there is therefore absolute need to amend the existing service tax registration certificate with new service tax code – i.e., “Service” as defined by Section 65B(44) read with Section 65B(51) of the Finance Act, 1944.”

2. The following declaration is to be given by the Rent-a-cab service provider to enable the recipient of services to pay ser-tax on reverse charge basis (w.e.f., 1.7.2012 … as per point of taxation Rules) on car hiring services by considering the 60% abatement. I.e., if the service bill for car hire charges is Rs.100 then considering 60% abatement (subject to the declaration so given below in the bill of the service provider), the recepient need to pay ser-tax on the 40% à i.e., 12.36% of 40%

Declaration è “CENVAT credit on inputs, capital goods and input services, used for providing the taxable service, has not been taken under the provisions of the CC Rules, 2004.”

3. In relation to Rent-a-cab service, on reverse charge basis, the recipient of service need to pay service tax only on 25% of the invoice Value subject to specified conditions being fulfilled … as under;

[ Pls note that à earlier the condition of obtaining declaration from Goods Transport Agency was done away with but in the new proposal effective 01.07.2012 it has again been brought back. This means now the recipient need to obtain a certificate from transporters to this effect. [Draft declaration given as under]

[ON LETTER HEAD OF THE TRANSPORTER / SERVICE PROVIDER]

To,

M/s. ABC LTD … the recipient of services

(Address….)

Dear Sir,

I/We, (name of the signing person) on behalf of ______________________________

a) I/We have not taken any CENVAT credit of excise duty on inputs or capital goods or CENVAT credit of service tax paid on any input services, for the purpose of providing taxable service in relation to GTA services / ………….services under the provisions of the CENVAT Credit Rules, 2004.

b) I/We undertake not to avail the aforesaid credits or benefits for the period mentioned above.

c) I/We undertake to indemnify the service recipient against any payment of liability or loss of credit arising out of our non-compliance of this declaration.

For XYZ Transport Company LTD

SERVICE PROVIDER

Authorized Signatory

Place & Date ____________________

Note: The above undertaking should be obtained on quarterly basis beginning from Oct 2012 more specifically for the period July to Sept 2012 in case service provider has not provided declaration on consignment note to this effect.

4. What does a service provider need to indicate on the invoice when he is liable to pay only a part of the liability under the partial reverse charge mechanism?

The service provider shall issue an invoice complying with Rule 4A of the Service Tax Rules 1994. Thus, the invoice shall indicate the name, address and the registration number of the service provider; the name and address of the person receiving taxable service; the description and value of taxable service provided or agreed to be provided; and the service tax payable thereon. As per clause (iv) of sub-rule (1) of the said rule 4A ‘’the service tax payable thereon’ has to be indicated. The service tax payable would include service tax payable by the service provider.

5. Would service tax be leviable on processes which do not amount to manufacture or production of goods?

Yes. Service tax would be levied on processes, unless otherwise specified in the negative list, not amounting to manufacture or production of goods carried out by a person for another for consideration. Some of such services (intermediate production process as Job-work that was earlier classified under BAS) relation to processes not amounting to manufacture are exempt as specified in entry no. 30 of Exhibit

6. Would service tax be leviable on processes on which Central Excise Duty is leviable under the Central Excise Act, 1944 but are otherwise exempted?

No. If Central Excise duty is leviable on a particular process, as the same amounts to manufacture, then such process would be covered in the negative list even if there is a central excise duty exemption for such process. However if central excise duty is wrongly paid on a certain process which does not amount to manufacture, with or without an intended benefit, it will not save the process on this ground.

7. Would non-compete agreements be considered a provision of service?

Yes. By virtue of a non-compete agreement one party agrees, for consideration, not to compete with the other in any specified products, services, geographical location or in any other manner. Such action on the part of one person is also an activity for consideration and will be covered by the declared services.

8. Would labour contracts in relation to a building or structure be treated as a works contract?

No. Labour Contracts do not fall in the definition of works contract. It is necessary that there should be transfer of property in goods involved in the execution of such contract which is leviable to tax as sale of goods. Pure labour contracts are therefore not works contracts and would be leviable to service tax like any other service and on full value.

9. Would contracts for repair or maintenance of motor vehicles be treated as ‘works contracts’? If so, how would the value be determined for ascertaining the value portion of service involved in execution of such a works contract?

Yes. Contracts for repair or maintenance of moveable properties are also works contracts if property in goods is transferred in the course of execution of such a contract. Service tax has to be paid in the service portion of such a contract.

10. Is the reverse charge applicable on services provided and complete before 1.7.2012 though payments were made after 1.7.2012?

For any service whose point of taxation has been determined and whole liability affixed before 1.7.2012 the new provisions will not apply. Merely because payments are being made after 1.7.2012 will not add any additional liability on the service receiver in respect of such services.

/p>

CAclubindia

CAclubindia