Introduction

With the world turning into one global entity, trade and commerce has increased leaps and bounds. Along with the benefits it carries, there are many complex issues which need to be addressed. One of these issues is tax evasion and base erosion. Transnational Enterprises arrange their transactions in a way to evade tax or disguise the transactions to reduce their tax liability. This results in loss of revenue for the countries where such enterprises are based. To curb such practices Transfer Pricing Regulations were introduced in the year 2002. Chapter X of Income Tax Act, 1961 (hereinafter referred as the Act) contains the provisions for Transfer pricing.

International Transactions

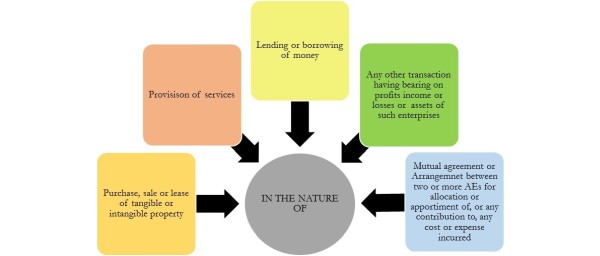

To invoke the provisions of Chapter X, it is obligatory to prove the existence of an international transaction. Therefore it is necessary to understand the crux of the definition of International transaction. As per section 92B of the Act, international transaction means a transaction between two or more associated enterprise, either or both of whom are non-residents in the nature of :-

Let us analyze the definition of International transaction.

It is a transaction: The word transaction has been defined under section 92F of the Act. It entails that the term transaction includes an arrangement, understanding or action in concert, irrespective of whether it is formal or in writing or whether or not it is intended to be enforceable by legal proceedings.

- Whether a verbal arrangement which is not

legally enforceable is capable of amounting to transaction or arrangement?

YES (R. v. Dairy Produce Quota Tribunal for England and Wales)

- Whether a pure reimbursement of expense to AE not involving any profit mark-up would be a transaction and consequently an international transaction?

YES (Stream international Services Pvt Ltd v. ADIT (IT)[2013]Mumbai Tribunal)

-Whether a framework agreement whereby foreign folding company is granted call options to acquire shares for consideration paid by foreign holding co. is a transaction and consequently an international transaction?

YES (Vodafone India Services Pvt Ltd .v. Asst CIT [2014])

- The transaction needs to be between two or more associated enterprises (AEs)( as defined under Section 92A) or deemed to be between 2 or more AEs under the provisions of Section 92B (2).

- Either or both of these associated enterprises should be Non-residents:- When the assessee and the AE are both residents for the purpose of taxation, transaction between them cannot be regarded as international transaction. Therefore it is necessary for a transaction to fall within the purview of section 92B (1) which means that both the sub-sections of Section 92B of the Act operate jointly. (The concept of deemed AE shall be dealt later in this article)

-Whether a transaction wherein an assessee company and company providing management services to it were both residents in India shall be considered as an international transaction? NO (Astrix Laboratories Ltd v. Asst CIT [2015] Hyderabad Tribunal)

-Whether a transaction wherein payments were made by the assessee Indian Agent of foreign TV channels to Indian residents by way of advertisements and public advertisements are international transactions? NO (CIT V. NGC TV Network (India) Pvt Ltd [2014])

-Whether the assessee (WOS of USA company) rendering installation and commissioning services to Indian customers and there was no agreement between Indian customers and the parent company amounts to international transaction? NO (CIT V Stratex Networks (India) Pvt Ltd [2013])

The transactions can be in the nature of different type of transactions as illustrated above.

Deemed International Transaction (Section 92b (2) of the Act)

The amendment made by the Finance Act 2014 has introduced a concept 'Deemed International Transaction' which will bring in a new era of litigation. This has widened the horizons of transfer pricing provisions beyond imagination and has turned it into an umbrella legislation covering almost all the international and specified domestic transactions. Now, the transactions between an enterprise and a person other than an associated enterprise (independent third party) shall be deemed to be an international transaction entered into between associated enterprises in the following circumstances:

- Existence of a prior agreement in relation to the relevant transaction between such other person and the associated enterprise ; or

- The terms of the relevant transaction are determined, in substance, between such other person and the associated enterprise.

Therefore it can be clearly asserted that transactions between two resident entities are brought within the purview of International transactions on fulfilment of two conditions laid down in section 92B (2) of the Act. However it has been clear from the approach of tax authorities that not only the agreements/arrangements will is a determining factor for the applicability of the provisions of deemed transaction but also the actual conduct of the transacting parties will be taken into consideration.

However it is necessary that at least one of the associated enterprises is a non-resident because if both the enterprises are non-residents then the Chapter of Transfer Pricing shall apply only if income of one of the non-residents is assessable under the Indian Income Tax.

Landmark Case law

Kodak India Private Limited Vs Addl. Commissioner of Income-tax [2013] (Mumbai tribunal)

Facts:

- Eastman Kodak Co. USA entered into an agreement with Carestream Inc, USA for sales of its medical imaging business stream on global basis.

- Pursuant to this agreement, Kodak India entered into an agreement with Carestream Health India Private Limited ('Carestream India') for sale of its medical imaging business.

- Terms and consideration of sale were independently determined by Indian companies without any influence by agreement between overseas holding companies.

- During the course of assessment proceedings, TPO treated the transaction of sale of imaging business segment by Kodak India to Carestream India as 'deemed international transaction' under Section 92B (2) of the Act and proceeded to make upward adjustment for the same.

- This adjustment was made by TPO without application of any of the method specified under Section 92C of the Act.(computation of ALP)

- When the assessee approached the DRP, it upheld the order of the TPO.

- Aggrieved by the order of the DRP & TPO, Kodak India filed an appeal before the Mumbai Tribunal.

Judgment of the Mumbai Tribunal

After hearing arguments of both the parties, Mumbai Tribunal held that transaction of sale of imaging business by Kodak India to Carestream India cannot be considered as 'deemed international transaction' on the ground that:

- Both the transacting entities are domestic entities which are resident in India;

- Even though the transaction of sale of imaging business segment in India is in consequence of global agreement between overseas holding companies, there was no prior agreement and/ or terms and conditions for sales were not dictated by non-resident agreement; and

- TPO has not applied one of the method specified under Section 92C (2) read with Rule 10B, while arriving at the amount of TP adjustment.

Aggrieved by the order of the Mumbai Tribunal, the tax department approached the Bombay High court. Key question of law before consideration of Bombay HC was 'whether provisions of section 92B (2) are applicable to sale transaction between two domestic companies?'

Judgment of Bombay High Court

Bombay HC noted that Revenue authorities have accepted the observations of the Tribunal on two counts:

(1) Terms of sale of business were independently determined by Indian entities without any influence by global agreement and

(2) Assessee had reasonably determined the arm's length price, while Revenue Authorities had not used one of the prescribed methods and hence, matter cannot be remanded back for determination of arm's length price.

Based on these factual aspects, Bombay HC held that appeal under consideration is academic in nature since there would not be any adjustment on Kodak India even if question is answered in favour of tax department and hence, Bombay HC dismissed the appeal filed by tax department without providing any ruling on the question of law.

Conclusion

The definition of International Transaction has gained utmost importance under the transfer pricing provisions as the preliminary requirement to invoke the provisions of Chapter X (of Income Tax Act,1961) is to prove the existence of an 'International Transaction' and this makes it essential to understand the meaning of International transaction.

CAclubindia

CAclubindia