Part A - Rationale for Introducing the 'Banning of Unregulated Deposit Schemes' Ordinance

Introduction

Making money has never been easier than it is today. However, the same does not transcend the ease with which one can lose it. By deceitfully employing the stratagem of a path breaking investment scheme, countless gullible investors have fallen prey to this misrepresentation.

In this regard, the combination of an uncertain legal recourse and an overburdened law enforcement machinery could neither protect, nor secure justice to the victims of such dubious schemes. To plug in this lacunae, the 'Banning of Unregulated Deposit Schemes' Ordinance (hereinafter referred to as 'Ordinance') was promulgated by Hon'ble President of India, Shri Ram Nath Kovind.

Scope

The preamble describes the enactment as 'An Ordinance to provide for a comprehensive mechanism to ban the unregulated deposit schemes and to protect the interest of depositors and for matters connected therewith or incidental there to'.

In other words, the scope of the Ordinance can be segregated into 2 parts, namely:

a. Fraudulent default in repayment of dues1 (vis-à-vis Regulated Deposit Schemes)

b. Wrongfully inducing another person to:

o Invest in an Unregulated Deposit Scheme2, or;

o Become a member or a participant of an Unregulated Deposit Scheme3.

The justification for introducing this ordinance has been constantly defended as being bona fide and legitimate, however, its drafting sings to a different tune. In the authors' opinion, the Ordinance deals with an unchartered territory of deposit regulation. Therefore, at this nascent stage, any evaluation of the Ordinance should primarily confine itself to the synergy between the law itself and the spirit of the law.

Through its submission, the authors intend to provide a constructive critique on the following 2 aspects:

• Effectiveness of this Ordinance in tackling the problems associated with Unregulated Deposit-making

• Unintended consequences of introducing the Ordinance

Background

In the present legal scenario, various deposit related activities are governed by the following Institutions:

• Non-Banking Financial Companies (NBFCs) are under the regulatory and supervisory jurisdiction of the Reserve Bank of India (RBI)

• Chit Funds and Money Circulation Schemes are under the domain of State Governments;

• Housing Finance Companies come under the purview of National Housing Bank (NHB);

• Collective Investment Schemes come under the purview of the Securities and Exchange Board of India (SEBI)

• Deposit taking by companies other than NBFCs are regulated by Ministry of Corporate Affairs (MCA).

However, several companies/ institutions have been exploiting regulatory gaps to dupe financially illiterate investors of their hard earned savings. In January 2019, Law Minister Ravi Shankar Prasad had said that the CBI had lodged about 166 cases in the past four years related to chit funds and multi-crore scams, with the highest numbers reported in West Bengal and Odisha4. Further, in fiscal year 2017-18 a total of 63 companies involved in Ponzi activities were being scrutinized by the Serious Fraud Investigation Office5. Thus, a stringent law against such gross misconduct is the need of the hour.

To tackle this menace, Finance Minister Arun Jaitley in his 2016-17 Budget Speech, suggested the need for a Central Legislation that would tackle the problem of illegitimate deposit taking schemes. Subsequently, a Standing Committee on Finance as well as an Inter-Ministerial Group were constituted to study the issue and give their recommendations. The main agenda for these committee's was to ensure that all relevant aspects of deposit taking are brought under the watchful eyes of the law.

Consequently, the Banning of Unregulated Deposit Bill was introduced in the Lok Sabha in the on July 18, 20186. Being a Money Bill, the Bill did not see the light of the day in the Rajya Sabha in the same session of the Parliament. This resulted in the incumbent Cabinet to push for an Ordinance until the Bill receives an assent from the Upper House.

'Ponzi Scheme' Decoded

To appreciate the nuances of the Ordinance, it is imperative to understand the modus operandi adopted by fraudulent deposit taking institutions.

Etymology

Meaning

Structure

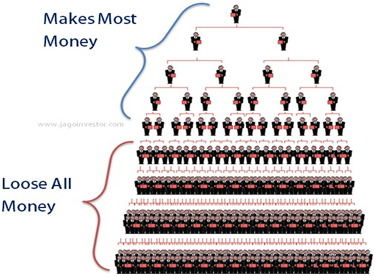

The structure of a Ponzi Scheme draws its foundation from a Multi-Level Marketing/ Pyramid Selling structure. The controversy in adopting such a structure arises if the organization adopts the following structure:

• Existing distributors are encouraged to recruit new distributors who are paid a percentage from their new recruits' sales.

• These new distributors must recruit new members who would also get a percentage of their new recruits' sales.

• Consequently, these fresh recruits, at the latter stages, are the main distributor's 'downline'. In other words, the initial recruiter is earning a significant commission from the entirety of sales made by his recruits and those recruited by him in this 'pyramid-like' sales chain hierarchy. There is no limit to his earnings.

• Therefore, only a select few members at the top of a pyramid are handsomely rewarded for their efforts while those at the bottom of the hierarchy are left high and dry.

To summarize this, a pyramid structure guarantees excessive returns to those at the higher ends of the pyramid at the behest of those at the lower end. Owing to the socio-economic demographics of a country like India, members at the lower rungs of a pyramid structure are usually those who have a negligible quantum of disposable income. Thus, rather than ensuring a substantial and secured returns to such investors, their savings are wasted in unscrupulous investments which guarantee negligible or zero returns. In a developing country like India, with widespread income inequality, encouraging investments in such a sector would be counterproductive.

Ponzi Schemes in India

With regard to such Ponzi Schemes, Justice Mridula Bhatkar of the Hon'ble Bombay High Court had aptly remarked 9,

'The motto of the company 'sell more, earn more' appears very attractive and innocuous. However, this motto is fully camouflaged. The company stands on a basic statement that people can be fooled. Thus, the true motto is 'sell more earn more' by fooling people. In fact it is a chain where a person is fooled and then he is trained to fool others to earn money. For that purpose, workshops are conducted where study and business material is provided with a jugglery of words, promises and dreams. Thus, the deceit and fraud is camouflaged under the name of e-marketing and business.'

"It has very grave and serious impact on the economic status and mental health of the people on a large scale. On considering parameters of section 438 of the Code of Criminal Procedure, I am not inclined to protect the accused. It won't be out of place to mention that such circulation is required to be stopped. It is necessary for the prosecution to take injunctive steps against this business activity, which is prima facie, illegal. Though by stopping this business, a large group of people may get financially affected, however, it will save larger groups of people from becoming prey of this activity10,"

A few Ponzi Schemes to have duped investors in India have been summarized herewith 11:

|

Scam |

Factual Summary |

|

Speak Asia Scam |

• Investors were asked to pay Rs. 11,000 and fill up online survey forms. • Returns worth Rs. 52,000 per annum were guaranteed to investors. |

|

• Additional Rewards for enrolling more people into the scheme. • Scammers made away with Rs. 2,276 crore from 24 lah investors. |

|

|

Saradha Group Chit Fund Scam |

• Named after a spiritual guru to bring goodwill to the organisation. • Built a huge brand value in the initial stages. • Returned almost 40% of the money deposited by the initial band of investors. • After its collapse, it caused an estimate loss of Rs. 200-300 Billion Rupees to 1.7 million investors. |

|

Amway Scam |

• Sale if actual products at a grossly overpriced rate. • Lured in depositors with promises of lucrative financial incentives in if they engaged more distributors • Money brought in by the new distributors was used to pay off the original distributors • Distributors eventually lost their money as no one was willing to take the expensive product off their hands |

|

City Limouzines Scam |

• Investors were informed that money would be used to buy stakes in popular cars. • Instead of buying the car, he would rent them and pay the seller huge returns. • Promised returns to the existing investors for bringing in new investors. • Used this to finance the cheques he paid out to his original investors. • More than 2,00,000 investors were tricked off in this Rs. 1,000 crore scam. |

One common thread in all of them is the adoption of a Pyramid Structure. Thus, while this business structure sounds ingenious, in reality it is rife with devastating consequences.

Expectations from the Ordinance and its Salient features

The Seventieth Report published by the Standing Committee on Finance clearly highlights the main problem to be addressed by an Ordinance of such nature. It endeavors to:

• Protect gullible investors who are being duped by such illicit schemes;

• Increase public faith in the deposit raising entities which are regulated and accountable to the Government or its Regulators.

In light of the aforementioned objectives, the Seventieth Standing Committee on Finance Report has cogently highlighted the salient features of Ordinance through which it hopes to curb the menace of illegitimate deposit making. They are as follows 12:

• Complete prohibition of unregulated deposit taking activity;

• Deterrent punishment for promoting or operating an unregulated deposit taking scheme;

• Stringent punishment for fraudulent default in repayment to depositors;

• Designation of a Competent Authority by the State Government to ensure repayment of deposits in the event of default by a deposit taking establishment;

• Delegating requisite powers and functions of the competent authority, including the power to attach assets of a defaulting establishment;

• Designation of Courts which would oversee repayment of depositors and to try offences under the Act;

• Listing of Regulated Deposit Schemes in the Bill, with a clause enabling the Central Government to expand or prune the list.

Part B - Implications of the Ordinance after its Promulgation

Consequences of the Ordinance

The Ordinance will have huge implications for Ponzi schemes operating in India. Having discussed the rationale for introducing this Ordinance, it is time to analyze its implications.

Date of Applicability of the Ordinance - Retrospective or Prospective

Issue

The Ordinance was promulgated on 20th February, 2019. After its introduction, one of the major things to have puzzled many is what happens to 'unregulated deposits ' outstanding in the books of just before the ordinance was promulgated.

Authors' Interpretation

Section 1(3) of the Ordinance states that 'It shall come into force at once'. Which means the Ordinance will be applicable from the 21st of February 2019 (the day when it was notified in the Official Gazette of India). Additionally, section 3 of the Ordinance clearly states that 'On and from the date of commencement of this ordinance - unregulated deposits schemes shall be banned'. The above mentioned sections indicate that the aforementioned ordinance has a prospective effect. In simpler terms, deposits on or before 20th February, 2019 will not fall within the ambit of this legislation.

Recommendation

Finance Ministry officials have informally assured that the ordinance will not be retrospective. However, considering the propensity of the Central Government to enforce legislations retrospectively, an explicit clarification from the Central Government would be welcome. In the interim, it would be worthwhile for deposit takers to ensure that they are complying with all other central and state laws in respect of deposits taken on or before 21st February, 2019.

Regulatory mechanisms created by virtue of the Ordinance

While the government has adopted a muscular, hard line approach towards Ponzi scheme operators, it requires an efficient mechanism to address the grievances of depositors and initiate legal proceedings against fly by night operators.

The regulatory entities envisaged under this ordinance are as follows:

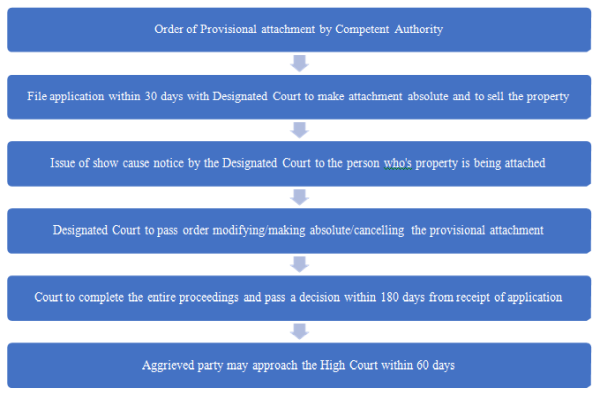

Flow of Work under the Ordinance

Like the Insolvency and Bankruptcy Code, the Ordinance too seeks to cut out red tape and ensure time bound resolution of litigation. Thus, one of the major hallmarks of the investigation and prosecution procedure under this ordinance is the fact that it is obligatory upon the designated courts to ensure disposal of cases within 180 days of receipt of application.

A salient description of the procedure to be followed for disposal of cases is provided hereunder:

Ramifications of the Ordinance on Political Funding

The Electoral Bond Scheme, 2018 has helped political parties garner over Rs. 222 crores in FY 2017-18. With an even higher quantum expected in FY 2018-19. Thus, it is imperative to analyze the possible implications of the Ordinance on political funding.

Exclusions

Section 2(4)(i) of the Banning of Unregulated Deposit Schemes Ordinance, 2019 goes on to exclude the following amounts from the definition of a 'deposit':

• Amounts accepted by political parties u/s 29B of Representation of People Act, 1951

• Deposits made under Section 34 of the Representation of People Act, 1951

Electoral Bond

Before dwelling further, the author would take the liberty to reiterate the meaning an 'electoral bond'. An 'electoral bond' is designed to be a bearer instrument like a Promissory Note. It is similar to a bank note payable to the bearer on demand, free of interest. An electoral bond can be purchased by any citizen of India or a body incorporated in India with a KYC-compliant account. Donors can donate the bonds to their party of choice which can then be cashed in via the party's verified account within 15 days.

Relevant Provisions of the Representation of People Act, 1951

Section 29B of the Representation of People Act, 1951 allows a political party to accept any amount of contribution voluntarily offered to it by any person or company (other than a Government company). Section 34 of the aforementioned legislation requires an electoral deposit to be furnished by a poll candidate.

Author's Interpretation

A brief perusal of the Gazette which notified the Electoral Bonds Scheme 201813 should leave the readers fairly confident that it is squarely covered within the first exclusion criteria (i.e. Voluntary political contributions u/s 29B). Relevant Portion from the Gazette has been provided herewith - '13. Tax treatment.- - Tax Act, 1961.'

Thus, it would be fair to conclude that the Government has kept all political funding including electoral bonds beyond the purview of this ordinance.

Implications for Businesses as well as salaried Individuals

After the Ordinance was promulgated, many experts were of the opinion that the ordinance might end up preventing businesses from taking unsecured loans or even salaried people from taking loans for their personal reasons. The Department of Financial Services in a series of tweets clarified that 'Banning of Unregulated Deposit Ordinance-2019, exempts Individual, Firm, Companies & LLP etc. for taking any loan and deposit for their course of business as per section 2(4) e,f,l and other provisions.14' It also went on to clarify that this ordinance was promulgated to prevent illegal operators from running Ponzi schemes and defrauding gullible investors.

However, notwithstanding the assurances given by the finance ministry, a look at the bare text should convince its readers that a deeper study is required. While a layman's take on this ordinance might be that there are only two types of deposits - regulated and unregulated, a careful reading of the bare act points to an interesting lacunae. With regard to regular business practices, there does exist a third category of deposits wherein:

i) The deposits received are neither regulated;

ii) Nor are they solicited as a business.

Hence, such deposits do not fall within the ambit of a regulated or unregulated deposit as defined by the Ordinance. In other words, there are three types of deposits envisaged under this ordinance -

a) Regulated Deposit Scheme;

b) Unregulated Deposit Scheme;

c) Deposits which are neither of the two.

This third category of deposits has led to some interesting complications. Some of them have been discussed hereunder:

Personal Loans for personal exigencies

Since these loans are not solicited as a business - it fits into the third category as explained above. This ordinance only penalizes unregulated deposit schemes and is completely silent on the third category of deposits. The government has clarified that the loan received is covered within the definition of a deposit. Hence individuals are not likely to face regulatory heat over the same.

(Note - A loan taken by an individual/firm from its /partner's relatives for any purpose lies outside the ambit of this ordinance.)

An individual businessman/ Firm/ LLP/ HUF which regularly takes unsecured loans from money lenders as well as investors

A loan is prima facie a deposit but the ordinance gives certain exclusions. They are as under

- 'an amount received in the course of, or for the purpose of business and bearing a genuine connection to such a business including -

i) Payment/ Advance/ Part Payment for provision of Goods and Services

ii) Advance is received for sale of immovable property if advance is adjusted against sale

iii) Security Deposit for contract performance

iv) Advance for supply of long term capital goods projects15'

Thus, the question which ought to arise is whether a non-corporate or an LLP which raises debt is also a deposit taker. The government's stand on the issue is - since such transactions are excluded from the definition of deposit, it is an amount received in the course of business.

Issue

A careful reading of the section could give rise to some unintended complications. The exclusion mentions that the amount should be received in the course of business and it should bear a genuine connection to the business. In this regard, for an individual engaged in manufacturing/trading/ consultancy - debt based finance would hardly create any genuine connection with its business model.

Authors' recommendation

In light of the same, there is a need for the legislature to segregate advances received by a business into two parts, namely:

i) Trade Advances - Advance payments or Progress payments from customers which are linked to the business model and have an operational connotation; and

ii) Debt Finance - Financing which has less to do with a business' operational activity and more with an entity's capital structure.

Ensuring regulatory compliance by businesses

In respect of a business which is regularly funding its business operations using unsecured loans, it can be said that it is receiving deposits as a business. In such cases, non-corporates regularly raising funds from private investors and money lenders are likely to face regulatory heat in the days to come. Moreover, such businesses will have to comply with Section 10 and intimate the government via. the designated information utility about their business model and any other particulars as may be sought.

Authors' recommendation

In order to protect hounding of businessmen who are entering into genuine transactions, a legislative change from the government's end should be welcomed. It would ensure that only Ponzi scheme operators would be hit and there will be no unintended collateral damage.

Impact on Real Estate Developers who regularly raise deposits to fuel their operations

Section 2(4)(l)(i) specifically excludes advances for immovable property from the definition of deposit if the advance is adjusted against immovable property in the event of sale. This not being the case when a real estate developer raises deposits, it would be possible for one to contend that these deposits are indeed covered by the definition of deposits under this ordinance.

Also, if the real estate developers are raising deposits from retail investors and the public at large, it could be said that the same is solicitation by way of a scheme or a business.

Interpreting the Ordinance in this manner could have significant ramifications for the real estate sector which has already been hit hard by structural reforms like GST and RERA.

Allowability of Partner Loans

Another interesting controversy which this ordinance has stoked is whether loans given by partners to their firms / LLPs are deposits or not.

Section 2(4)(e) specifically excludes contributions towards capital by partners of a firm / LLP and Section 2(4)(f) excludes loans received from relatives of partners from the definition of 'Deposits'. Thus, the whole ordinance is silent on the issue of partner advancing loans to their respective firms / LLPs.

Partner loans are certainly not similar in character to/ synonymous with capital contributions. Section 13 of the Indian Partnership Act clearly separates the two. Additionally, it will be difficult to fit loans into the exclusion criterion of 'amount received in the ordinary course of business and bearing a genuine connection to the business'. Thus, partner loans might end up falling within the ambit of deposits as envisaged under this audience.

In such a case, partner loans will neither be regulated (as they are not listed under the First Schedule) nor unregulated (not being solicited as a business since partners are usually a small group of people). Hence partner loans would fall in the third residual category of deposits.

While there is no penalty for deposits other than regulated deposits, it will be advisable for such firms to furnish the details of their businesses to the Central Government appointed information utility to ensure compliance with Section 10 of the ordinance.

Authors' Recommendations for the proposed Act

In case the Ordinance fructifies into an Act, the authors hope that the Act shall take into consideration the following recommendations:

• Incorporate a clarification regarding the applicability of this ordinance

• Incorporate transitional provisions to deal with deposits received before the promulgation of this ordinance

• Varied interpretations of the word 'business' can cause inconvenience to entities which regularly raise debt. Thus, the Government must provide an express definition of the word 'business' as envisaged by the Ordinance/ Act.

• Incorporate an amendment whereby partner loans will be excluded from the definition of deposits.

• Companies are already required to file an MCA E-Form called 'DPT-3' which furnishes details about the deposits received by them. Requiring entities to intimate the government about its deposits under this Act is mere repetition. Therefore, the government must grant exemption to entities reporting their deposits under form 'DPT-3'.

Conclusion

The Banning of Unregulated Deposit Ordinance, 2019 is a well-intentioned and much needed legislation to ensure that fly by night operators are prosecuted and gullible investors are not defrauded. At the same time the government should be willing to walk the tight rope on ease of doing business and avoid being high handed towards the needs of genuine entrepreneurs.

To conclude, with some amendments directed towards preventing any unintended collateral damage, this ordinance and the proposed Bill can serve as a potent tool in India’s crusade against Ponzi schemes.

1 Section 4 of Banning of Unregulated Deposit Scheme Ordinance, 2019

2 Section 5 of Banning of Unregulated Deposit Scheme Ordinance, 2019

3 Section 5 of Banning of Unregulated Deposit Scheme Ordinance, 2019

4 Chitranjan Kumar, Modi government passes ordinance to ban unregulated deposit, Business Today, (February 22, 2019) https://www.businesstoday.in/current/economy-politics/modi-government-passes-ordinance-to-ban- unregulated-deposit/story/321422.html

5 PTI, Ponzi schemes: SFIO lens on 63 companies this fiscal, Economic Times (December 25, 2017) https://economictimes.indiatimes.com/news/politics-and-nation/ponzi-schemes-sfio-lens-on-63-companies-this- fiscal/articleshow/62239685.cms?from=mdr

6 PRS Legislative Research, https://www.prsindia.org/billtrack/banning-unregulated-deposit-schemes-bill-2018

7 U.S. Securities and Exchange Commission, What is a Ponzi Scheme (October 09, 2013) https://www.sec.gov/fast-answers/answersponzihtm.html#PonziWhatIs

8 Image taken from: https://www.jagoinvestor.com/2012/10/how-multi-level-marketing-schemes-work.html

9 Malckolm Nozer Desai vs The State Of Maharashtra on 06 May 2016 (Bom HC)

10 Ibid.

11 Scroll Staff, 5 Pyramid Schemes India fell for, The Scroll (January 03, 2014) https://scroll.in/article/603226/5- pyramid-schemes-india-fell-for

12 Standing Committee on Finance Seventieth Report, Page 9 (January 2019)

13 Ministry of Finance, Electoral Bonds Scheme 2018 (28 March 2018) http://pib.nic.in/newsite/PrintRelease.aspx?relid=178142

14 Department of Financial Services, Twitter Feed (23 February 2019) https://twitter.com/dfs_india/status/1099337800745287681?lang=en

15 Section 2(4)(l) of the Banning of Unregulated Deposit Scheme Ordinance, 2019

The authors can also be reached at asdatar9898@gmail.com and pranav333bafna@gmail.com

CAclubindia

CAclubindia