PART 1 - BACKGROUND

1.1 Why new accounting standards are being introduced?

Need for a consistent accounting framework

Accounting bodies around the world are working towards having a consistent framework for financial reporting. This purpose of developing such a framework is to enable users of this information, particularly analysts and investors, to compare the performance and relative attractiveness of companies operating in different countries. A 'like-to-like' comparison will enable the users to make informed decisions regarding where to invest their or their clients' capital. The International Financial Reporting Standards ('IFRS') framework developed by the International Accounting Standards Board ('IASB') is a step towards achieving that goal. A number of countries, particularly in Europe, have already adopted the IFRS framework.

Currently, differences in the local accounting standards between countries make identification of investment opportunities difficult. Therefore, analysts are increasingly relying on IFRS financial statements to reveal investment opportunities globally. Arguably, companies which do not follow an 'IFRS-like' framework are at a relative disadvantage as analysts tend to overlook otherwise attractive investment opportunities due to a lack of understanding of the local accounting standards. Indian companies are expected to benefit by aligning themselves with IFRS to increase their financial competitiveness in the eyes of global investors. In summary, adoption of IFRS is likely to increase investment into the country.

Indian Accounting Standards (Ind AS)

With this objective of aligning the Indian accounting framework with IFRS, the Ministry of Corporate Affairs ('MCA') released a set of 39 accounting standards, referred to as 'Indian Accounting Standards' ('Ind AS') in February 2015. An amendment to the original notification was issued in March 2016, which clarified that Ind AS will be applicable to banks, insurers and most Non-Banking Financial Companies ('NBFC's'), an issue that was not adequately addressed in the earlier notification.

Each of these Ind AS mirror an accounting standard of the IFRS framework referred to as 'international standard' in this paper for ease of reference. Ind AS are not exact replicas of the international standards - the differences exist primarily because Ind AS restrict the choices available for accounting treatment compared to the corresponding international standard. As explained in the next section, adoption of Ind AS will not be mandatory for all companies but voluntary adoption by companies is possible unless prohibited. Chances are that solo entities with a net worth of less than INR 250 crores will have a choice whether to report under the existing Accounting Standards promulgated by Institute of Chartered Accountants of India ('ICAI') or voluntarily adopt Ind AS.

1.2 When will the Ind AS come into effect?

Ind AS will become applicable to companies in a phased manner starting from FY2016-17 and not all companies will be required to adopt them.

For companies other than banks, insurers, and NBFC's, Ind AS will be applicable as follows:

FROM 1 APRIL 2016 - will apply to any company with net worth of more than INR 500 crores as well as their subsidiaries, joint ventures, associates and holding companies.

FROM 1 APRIL 2017 - will apply to listed companies having net worth of less than INR 500 crores and unlisted companies of net worth more than INR 250 crores but less than INR 500 crores. Subsidiaries, joint ventures, associates and holding companies would also come under the ambit of Ind AS.

For banks, insurers and NBFC's:

FROM 1 APRIL 2018 - will apply to scheduled commercial banks (excluding Regional Rural Banks 'RRBs'), insurance companies and NBFC's having net worth of more than INR 500 crores. Subsidiaries, joint ventures, associates and holding companies would also come under the ambit of Ind AS.

FROM 1 APRIL 2019 - will apply to listed NBFC's having net worth of less than INR 500 crores and unlisted companies of net worth more than INR 250 crores but less than INR 500 crores. Subsidiaries, joint ventures, associates and holding companies would also come under the ambit of Ind AS.

1.3 Ind AS for employee benefits

There are primarily two Ind AS that directly relate to accounting and disclosures of employee benefit plans:

IND AS 19 EMPLOYEE BENEFITS: for accounting of employee benefits other than share based benefits

IND AS 102 SHARE BASED PAYMENTS: for accounting of share based benefits (e.g. ESOPs and SARs)

In this article, we restrict ourselves to Ind AS 19. Ind AS 102 is covered in a separate section of the original paper and is available on Numerica website.

PART 2 - IND AS 19: EMPLOYEE BENEFITS

2.1 What is going to change

As per the current accounting framework, accounting for all employee benefits, except share based benefits, is done as per the Accounting Standard ('AS') 15. For companies reporting under Ind AS, AS 15 will be replaced by Ind AS 19. While Ind AS 19 is a reflection of the most up to date version of IAS 19, AS 15 is based on a slightly older, but quite different, version of IAS 19 that existed prior to the 2011 amendments. The differences between AS 15 and Ind AS 19 are primarily of two types:

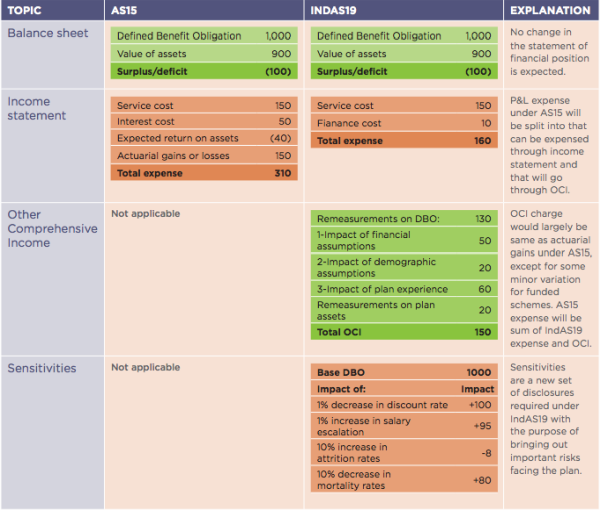

1. AS 15 actuarial gains and losses are referred to as 're-measurements' in Ind AS 19 and these no longer recognised in the P&L statement. Instead, they are recognised as 'Other Comprehensive Income' or OCI and charged to equity.

2. Disclosure requirements have increased with an intent to bring out the state of risk management affairs. Amongst other things, a key requirement is to disclose the sensitivities of the plan liabilities (i.e. Defined Benefit Obligation, or DBO) to significant actuarial assumptions.

2.2 How will Ind AS 19 affect you

In order to understand how your company will be affected, it will help to analyse the changes in a bit more detail. Illustrative disclosures for a hypothetical gratuity plan under Ind AS 19 and AS 15 are shown below to bring out the key differences:

To summarise, the transition to Ind AS 19 will bring benefits and concerns for the reporting company.

Financial position will remain unchanged

It is going to be all good news on the financials, primarily because of two reasons:

1. For most companies, the balance sheet will remain the same as under AS 15. As explained above, the methodology for setting assumptions or valuing the liabilities is broadly unchanged.

2. Since the actuarial gains and losses (now called re-measurements) are recognised outside the income statement, the expense in respect of benefit schemes is expected to remain quite stable each year. Earlier under AS 15, a slight change in discount rate could lead to a significant impact on the income statement. Under Ind AS 19, the impact of such changes will be recognised in OCI rather than the income statement.

New disclosures would require better risk management

The disclosure requirements, however, have increased significantly and the most important one being that related to sensitivities. There are other qualitative disclosures related to risk identification and management.

Comparison with global peers will demand a higher quality of disclosures

Another implication of reporting under Ind AS 19 would be that the disclosures will possibly undergo a higher level of scrutiny by the auditors, analysts and investors, who would expect the quality of reporting to match with other global companies. The responsibility for correct and complete reporting rests with the Board of Directors of the reporting enterprise and companies will need to get comfortable that the actuarial workings and disclosures suffice the requirements of Ind AS 19. This is a huge ask from non-actuarial personnel to assess and validate the work of professional actuaries by themselves, but a variety of methods are employed by companies around the world for achieving this. For example, using external auditors specialised in auditing actuarial reports, getting occasional second opinions from other actuaries and getting trained on spotting issues.

2.3 What you need to do

If you do adopt Ind AS 19, either mandatorily or voluntarily, there isn't much more that you will need to do compared to what you are doing already for AS 15. The only additional exercise that you will need to get involved in would be to get the financials of the immediately preceding period, prior to adoption, restated under Ind AS 19 so that prior period comparatives can be reported for the first year of adoption. There are two possible scenarios here:

1. If you are adopting Ind AS 19 for FY16-17, you will need to get the AS 15 numbers for FY15-16 restated as per Ind AS 19. It is advisable to get the restatement done ahead of time as all the information required to restate the numbers for FY15-16 should be already available with your actuary.

2. If you are adopting Ind AS 19 for FY17-18 or later, you will need to get two sets of actuarial reports from your actuary for FY16- 17 or for the year preceding the adoption. Again, this shouldn't mean that you need to do anything extra or provide more information to your actuary as both sets of reports can be prepared using the same data that you already provide for AS 15.

If your company is listed in India or have been reporting employee benefits liabilities on a quarterly basis, you may have to get the prior period comparatives for each quarter of the prior year.

2.4 Implications for companies reporting under IAS 19

Many Indian companies, particularly those with parent entities headquartered in Europe, also account for their employee benefit schemes under IAS 19. This is in addition to the Indian GAAP reporting, which so far has been under AS 15. With the adoption of Ind AS 19, the Indian and international GAAP disclosures are expected to be better aligned.

The most important difference between Ind AS 19 and IAS 19 relates to the selection of discount rate for actuarial valuation. IAS 19 says that the discount rate could be based on the yields available on AA-rated corporate bonds and government bonds should be used if a deep liquid market for corporate bonds does not exist. Ind AS 19, on the other hand, specifically prescribes the use of Government of India bonds only in selection of the discount rate.

Most Indian companies reporting under IAS 19 have already been basing their discount rates on Government of India bonds as the corporate bonds market is not deemed to be very liquid in India. Therefore, a company could be able to use the results of Ind AS 19 valuation to report under IAS 19 too, and vice versa, as long as any differences in the period of reporting are allowed for.

The author is a qualified actuary and a partner at Numerica Actuarial Consulting LLP, a Numerica Group entity. He has been involved in the providing employee benefits consulting services and other matters through Numerica to a number of corporates in India, UK and USA.

CAclubindia

CAclubindia