‘Comb’ as everybody knows is used to untangle, arrange smooth out, straighten and neaten the hair by drawing the comb through it. Therefore, the ‘comb’, in the context of ‘Business combination’ is that, that regulates, examines and scrutinises to neaten and straiten the ‘world of business’ by bringing within the ambit of Ind. AS 103 on ‘Business Combination’.

What’s Business Combination?

It is a transaction or event where an acquirer obtains control of one or more business. ‘A business combination may be structured in a variety of ways for legal, taxation or other reasons, which include but are not limited to: (a) one or more businesses become subsidiaries of an acquirer or the net assets of one or more businesses are legally merged into the acquirer; (b) one combining entity transfers its net assets, or its owners transfer their equity interests, to another combining entity or its owners; (c) all of the combining entities transfer their net assets, or the owners of those entities transfer their equity interests, to a newly formed entity (sometimes referred to as a roll-up or put-together transaction); or (d) a group of former owners of one of the combining entities obtains control of the combined entity’(Appendix B B6)

What’s the scope of Ind. AS 103?

As per Par 2 of the Standard, to quote, it runs as follows:

“This Indian Accounting Standard applies to a transaction or other event that meets the definition of a business combination. This Indian Accounting Standard does not apply to:

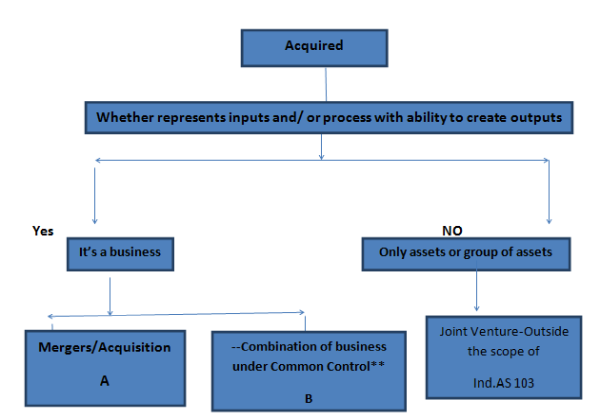

(a) the formation of a joint venture.

(b)the acquisition of an asset or a group of assets that does not constitute a business. In such cases the acquirer shall identify and recognise the individual identifiable assets acquired (including those assets that meet the definition of, and recognition criteria for, intangible assets in Ind. AS 38 Intangible Assets) and liabilities assumed. The cost of the group shall be allocated to the individual identifiable assets and liabilities on the basis of their relative fair values at the date of purchase. Such a transaction or event does not give rise to goodwill.

Appendix C deals with accounting for combination of entities or businesses under common control”.

How to account the assets or group of assets that are purchased with no business input or process?

If the assets or group of assets are purchased that has no business input or process; they are mere purchase of assets and accordingly accounted. Therefore, no goodwill or negative goodwill involved: and the assets will be in the books at their acquisition value. These are also outside the purview of the Ind.AS 103 but such activities will come under the umbrella of relevant Ind. ASs as applicable for the purpose of accounting.

The above is mapped out in the flow of the following diagram for easy understanding. A go through will be highly helpful.

**Appendix C deals with accounting for combination of entities or businesses under common control”

Before we proceed on what is Business combination under Ind.as 103, it is better to understand the basic difference between As 14 on ‘Accounting for Mergers and Ind. AS 103 on ‘Business Combination’ that it is highlighted to the extent possible in the Table –A, underneath).

Further, it is to be understood that there are a lot of cookies to be consulted- Ind. AS 103 on ‘Business Combination’, Ind. AS on 110 on ‘Consolidation of Financial Statements’, Ind. AS 27 on Separate Financial statements’ to ensure proper delivery/ compliance of Business Combinationunder common Control.

How Business combinations are accounted?

Accounting of business combination depends on whether the BC is by acquisitions/ mergers(A) or under common Control (B). The former is accounted by purchase methodand the latter by pooling of interest method.

A. Mergers/Acquisitions (Vide A of the forgoing Map)

Accounting of Business Combination under Ind. AS 103 is “Acquisition Method” forall BCs other than under common control and that are accounted under purchase method.

---Net assets taken over including intangible assets and contingent liabilities to be recognised at fair value if certain specified criteria are met (Para 18-19 of Ind. AS. 103). It should be noted that ‘the acquirer shall recognise as of the acquisition date a contingent liability assumed in a business combination if it is a present obligation that arises from past events and its fair value can be measured reliably’ that’s contrary to Ind.AS 37 on ‘ Provisions, Contingent Liabilities and Contingent Assets’.

-- Reverse acquisition is accounted for assuming the legal acquirer is the acquiree.

---BC transactions under common control are accounted under pooling of interest method..

Applying the acquisition method comprises four steps that are-

(1) Identifying the acquirer

(2) Determining the acquisition date

(3) Recognising and measuring identifiable assets acquired, liabilities assumed and any non-controlling interest in the acquire

(4)Recognise and measure the consideration transferred for the acquire

(5) Recognising and measuring excess or shortfall paid as relative to fair value of assets--.

Initial Accounting of BC:

If initial accounting of BC could be done only on provisional measurement at the end of the reporting period, adjustments to provisional measurement based on new information as to facts and circumstances that existed at the acquisition date are allowed within one year of the acquisition date retrospectively as if the adjustments have been made at the acquisition date except to correct error under Ind.AS 8.

BC achieved in stages:

If the acquirer enhances the equity interest in the acquiree to achieve control, the previous previously held is re-measured at acquisition date fair value any resultant gain or loss is recognised in Profit and loss.

Date of acquisition is the date on which acquirer obtains control of the acquired entity

Acquisition related costs are accounted as expenses in the period they are incurred and related services received such as follows:

a) Cost of maintaining an acquisitions department

b) Cost of internal staff who work on the deal

c) Cost of investigation

d) Incentives to of potential targets employees to remain with company post acquisition

e) Issue costs for debt or equity

f) Direct costs related to acquisition like consultant fees, rating fee etc.

How to measure Goodwill?

Goodwill is the difference between

A) -the considerations transferred + the amount of any non-controlling interest in the acquiree and + the acquisition-date fair value of any previous equity interest in the acquire

Over

b) -over the fair value of the identifiable net assets acquired.

Goodwill is recognised as an asset but not amortised but tested for impairment or more frequently if there is a scent/symptom of impairment.

How to deal with Bargain Purchase?

However, in case of bargain purchase, where (b) is in excess of (a) above, the acquirer shall recognise the resulting gain in other comprehensive income on the acquisition date and accumulate the same in equity as capital reserve, unless there is no clear evidence for the underlying reason for classification of the business combination as a bargain purchase, in which case, it shall be recognised directly in equity as capital Reserve.

Contingent consideration:

In a BC, contingent consideration is measured at fair value at the date of acquisition and that is considered for computation of Goodwill /capital Reserve arising on BC. Subsequent changes in contingent consideration are not to be adjusted in Goodwill except for period adjustments. Subsequent accounting depends on whether contingent consideration is equity or financial asset/ liability. If classified as equity, not to be re measured; in the case of the other two, are recognised in P&L

Restatement of previous period:

The financial information in the financial statements is to be restated as if the BC has taken place from the beginning of the previous period except where BC occurred after that date whence prior period is restated from that date.

Aggregation of retained earnings

The balance of the retained earnings of both transferor and transferee appearing in the financial statements are aggregated. The identity of the Reserves of the transferor is to be maintained.

Difference,if any, between the amounts as share capital issued plus any additional consideration in the form of cash or assets and the amount of share capital of the transferor should be transferred to capital reserve and to be presented from other capital reserves with disclosure of its nature and purpose.

Non-controlling interest: at the date of acquisition an entity may elect to measure on transaction by transaction basis the Non-controlling interest (a) fair value or NCI proportionate share of the identifiable net asset of the acquiree.

B. Business Combinations between entities that are under common control

For BCs between entities that are under common control, there is specific guidance included in Ind. AS 103 (Appendix C). Such business combinations are accounted for, using the pooling of interests method. Under the pooling of interests method:

Pooling of Interest Method

Business Combination transactions between entities under Common control should be accounted under ‘pooling of interest method’---- The assets and liabilities of the combined entities are reflected at their carrying amounts. No adjustments are made to reflect fair values nor are new assets and liabilities recognised. The only adjustments warrantedare to harmonise accounting policies. IFRS 3 does not apply to Combination of business or entities under common control but Ind. AS 103 includes transactions transfer of subsidiaries or business between entities within a group.

The following Table highlights the differences between AS 14 on Accounting for mergers and Ind. AS103 on Business Combination.( Table-A)

|

Sr.No |

Under Ind.AS |

Under Indian GAAP |

|

1 |

Scope: when an acquirer obtains control of one or more business except where --Purchase of only assets or group of assets that has no business input or process --formation of joint Venture But Ind. As 103 gives guidance on common control transactions. |

There is no comprehensive standard dealing with all BCs. Guidance for amalgamation is available in AS 14. As 15 deals with investment in subsidiaries; AS 10 deals with demerged unit acquired in a slump sale |

|

2 |

Date of acquisition is the date on which acquirer obtains control of the acquired entity. |

With reference to legal mergers, the appointed date as agreed to in the Scheme of amalgamation. The effective date is the date of filing the Court Order sanctioning amalgamation. If the appointed date precedes the effective date, the amalgamation is accounted on effective date with effect from appointed date. |

|

3 |

Acquisition accounting is based on substance. --All BCs other than under common control are accounted under purchase method. Net assets taken over including intangible assets and contingent liabilities to be recognised at fair value if certain specified criteria are met.Para 18-19 of Ind. AS 103) ---BC transactions under common control are accounted under pooling of interest method. |

Based on legal form under Indian GAAP.Under amalgamation,the purchase of identifiable assets and liabilities are accounted either at fair or book value.Para 12 of AS 14 |

|

4 |

Reverse acquisition is accounted for assuming the legal acquirer is the acquiree. |

Indian GAAP is silent on that. |

|

5 |

Goodwill:Prohibits amortisation of goodwill but to be tested for impairment. Para B63 (a) of Appendix B of Ind. AS 103 |

Under Indian GAAP goodwill arising out of amalgamation in the nature of purchase is amortised to P&L over a period not exceeding five years unless longer period is justified.Para 19 of existing AS 14 |

|

6 |

Bargain gain:Ind. AS 103 requires bargain gain on purchase arising on business combination to be recognisedin other comprehensive income and accumulated in equity as capital reserve, unless there is no clear evidence for the underlying reason for classification of the business combination as a bargain purchase, in which case, it shall be recognised directly in equity as capital reserve.Para 34 of Ind.AS 103 |

Under AS 14 the excess amount is treated as capital reserve.Para 17 of the existing AS 14. |

|

7 |

Contingent consideration in a BC is measured at fair value at the date of acquisition and that is considered for computation of Goodwill /capital Reserve arising on BC. Subsequent changes in Contingent consideration are not to be adjusted in Goodwill except for period adjustments. Subsequent accounting depends on whether contingent consideration is equity or financial asset/ liability. If classified as equity, not to be re measured; in the case of the other two, are recognised in P&L. |

- - |

A first-time adopter--how to go about?

“A first-time adopter may elect not to apply Ind. AS 103 retrospectively to past business combinations (business combinations that occurred before the date of transition to Ind. ASs). However, if a first-time adopter restates any business combination to comply with Ind. AS 103, it shall restate all later business combinations and shall also apply Ind AS 110 from that same date. For example, if a first-time adopter elects to restate a business combination that occurred on 30 June 2010, it shall restate all business combinations that occurred between 30 June 2010 and the date of transition to Ind. ASs, and it shall also apply Ind. AS 110 from 30 June 2010.”

The following table addresses different situations that the first time adopter of Ind. AS regime to find a way how to go about:(Table B){ For details visit Ind. AS 101/103)

|

Sr. No |

Different situations |

How to go about? |

|

1 |

If a first-time adopter restates any business combination (As per paragraph C1 of Ind.AS 101) |

To comply with Ind. AS 103, it shall restate all later business combinations from that date and shall also apply Ind. AS 110 from the same date. |

|

2 |

Ind. AS 21, on the Effects of Changes in Foreign Exchange Rates |

An entity need not apply Ind. AS 21, on the Effects of Changes in Foreign Exchange Rates, retrospectively to fair value adjustments and goodwill arising in business combinations that occurred before the date of transition to Ind. ASs and it shall treat them as assets and liabilities of the entity. |

|

3 |

When an entity is to apply Ind.AS 21on The Effects of Changes in Foreign Exchange Rates, retrospectively to fair value adjustments and goodwill? |

May apply when arising in either: (a) all business combinations that occurred before the date of transition to Ind. ASs; or (b) all business combinations that the entity elects to restate to comply with Ind. AS 103. |

|

4 |

If an entity becomes a first-time adopter later than its subsidiary (or associate or joint venture) (Paragraph D17 of Ind. AS 101) |

The entity shall, in its consolidated financial statements, measure the assets and liabilities of the subsidiary (or associate or jointventure) at the same carrying amounts as in the financial statements of the subsidiary (or associate or joint venture), after adjusting for consolidation and equity accounting adjustments and for the effects of the business combination in which the entity acquired the subsidiary.” Thus, in case where the parent adopts Ind. AS later than the subsidiary then it does not change the amounts already recognized by the subsidiary. |

|

5 |

Ind. AS requires allocation of losses to the non-controlling interest, which may ultimately lead to a debit balance in non-controlling interests, even if there is no contract with the non-controlling interest (NCI) holders to contribute assets to the Company to fund the losses. Whether this adjustment is required or permitted to be made retrospectively? |

A combined reading of paragraphs C4(k) of appendix C and B7 of Appendix B of Ind. AS 101 implies that in case an entity elects not to restate past business combinations, the previous GAAP carrying value of NCI is not changed other than for adjustments made (re- measurement of the assets and liabilities subsequent to the business combination) as part of the transition to Ind. AS. |

|

6 |

Is any adjustment required to goodwill arising on business combination on first time adoption of Ind. AS if an entity elects not to restate past business combinations? |

As per paragraph C4(g)/(h) of appendix C, in relation to cases where entity elects not to restate past business combinations, the carrying amount of goodwill or capital reserve in the opening Ind. AS Balance Sheet shall be its carrying amount in accordance with previous GAAP at the date of transition to Ind. ASs (i.e. no adjustment shall be made including for amortisation or write-off of goodwill in the previous GAAP and subsequent resolution of contingency affecting purchase consideration) except for certain adjustments which include* |

*(i) As per paragraph C4(c)(i), the first-time adopter shall derecognize an intangible asset recognized under the previous GAAP which does not meet the recognition criteria of intangible assets as prescribed under Ind. AS 38, and increase goodwill/decrease capital reserve, as the case may be, to the extent of carrying value of previously recognized intangible asset.

(ii) As per paragraph C4(f), the first-time adopter shall recognise an additional intangible asset that was not recognised earlier in accordance with the previous GAAP, in the opening Ind. AS balance sheet with a corresponding decrease in goodwill / increase in capital reserve.

(iii) Regardless of whether there is any indication that the goodwill may be impaired, the first-time adopter shall apply Ind. AS 36 in testing the goodwill for impairment at the date of transition to Ind. ASs and in recognising any resulting impairment loss in retained earnings.

(iv) Correction of any errors discovered on transition to Ind. AS In line with paragraph C4(j), the carrying amount of goodwill in the consolidated financial statements may undergo a change if an entity that was not previously classified as a subsidiary shall now be classified as a subsidiary on transition to Ind. AS

If an acquisition is classified as an asset acquisition instead of business acquisition, then the goodwill recognised, if any, on such asset acquisition is derecognised.

In case of change in classification of an investee from a subsidiary to an associate or vice versa, the goodwill value does not undergo a change as compared to the previous GAAP carrying values. Ifthe past business combinations are restated;then the goodwill is recomputed in line with Ind. AS 103.

Appendix C to Ind. AS 101 provides the detailed consequences in case a first-time adopter does not apply Ind. AS 103 retrospectively to a past business combinations that may be visited upon.

Acquisitions leading to merger land in one legal entity. Entities under common Controlretain their separate identities. As has been spelt out earlier, the former is accounted by purchase methodand the latter by pooling of interest method. In earlier dispensation under Indian GAAP, there is no comprehensive standard dealing with all BCs;modus operandi for amalgamation is available in AS 14. As 15 deals with investment in subsidiaries; AS 10 deals with demerged unit acquired in a slump sale. Though Appendix Cof Ind.AS 103 on Business combination of entities under common control in Para 2 means ‘transferor of an entity or business which is combined into another entity’ as a result of a business combination, the subsidiaries have to perforce retain separate legal existence in India under the Companies Act, therefore, ‘combined to one’ apparently means ‘common control’. Though the Ind. AS has taken upon itself to give the Guidance to entities under common control in the above said Annexure Cto the Ind.AS 103, they have to be nonetheless consolidated as per Ind.AS 110 on ‘Consolidated Financial Statements’ as prescribed in Para 4 of Ind. AS 110.

For a recollection/ to fresh up:

An entity shall apply Ind.AS 1 on ‘Presentation of Financial Statements’ in preparing and presenting general purpose financial statements in accordance with Indian Accounting Standards (Ind. ASs). In other words, the Standard presents the required layout for the preparation of general purpose financial statements that are coordinated and harmonized in Ind. AS compliance Schedule III (Exposure Draft).

In addition to this, the Ind. AS regime taken upon on its shoulders to make available Ind. AS 27 on ‘Separate Financial Statements’ that are presented by a parent (i.e an investor with control of a subsidiary or an investor with joint control of), or significant influence over, an investee), in which the investments are accounted for at cost or in accordance with Ind. AS 109, on ‘Financial Instruments’. Ind. AS 27 shall be applied in accounting for investments in subsidiaries, joint ventures and associates when an entity elects, or is required by law, to present separate financial statements. But, under Indian dispensation, it is required/ mandatory both for compliance of law as well to comply with various tax laws.

Ind. As 103 on ‘Business Combination’ gives necessary ware- withal in the form of guidance in the appendix C on accounting for combination of entities or businesses under common control” that has been dealt with precisely earlier.

On the top, Ind. AS 110 on ‘Consolidated Financial Statements’ has a major role to play to establish principles for the and preparation of consolidated financial statements when an entity controls one or more other entities that will be handled by a separate article.

2016 is a leap year. India is going to usher in towards Ind.AS regime for the year commencing from April 2016 in respect of specified companies as prescribed to start with. No doubt, Indian entities will leap with confidence to Ind. AS to catch up with International Financial Reporting Systems as per the road map realising the fact there could only one integrated world economic order in the years to come.

Vide Notification Dated 24.07.2020, the following amendments have been made in Ind AS 103:

1. Business must include inputs and substantive processes applied to those inputs which have the ability to create output contribute to the ability to create output.

2. Change in definition of “Output” – It, now, focuses on goods and services provided to customers.

3. Omission of the ability to substitute the missing inputs and processes by the market participants.

4. Addition of “OPTIONAL CONCENTRATION TEST”.

5. Omission of Para B10 and insertion of Para B12A to B12D in Appendix-B.

CAclubindia

CAclubindia