1. IFRS 2 applies to all share-based payment transactions, which are defined as follows:

• Equity-settled, in which the entity receives goods or services as consideration for equity instruments of the entity (including shares or share options)

• Cash-settled, in which the entity receives goods or services by incurring a liability to the supplier that is based on the price (or value) of the entity's shares or other equity instruments of the entity

• Transactions in which the entity receives goods or services and either the entity or the supplier of those goods or services have a choice of settling the transaction in cash (or other assets) or equity instrument.

2. Outside the scope

• Cash/assets provided in terms of a Long Term Incentive which are not based on the fair value of group equity instruments are outside IFRS 2 scope - they are typically IAS 19. 'Other long-term employee benefits'

• Transactions in which the entity acquires goods as part of the net assets acquired in a business combination to which IFRS 3 Business Combinations applies

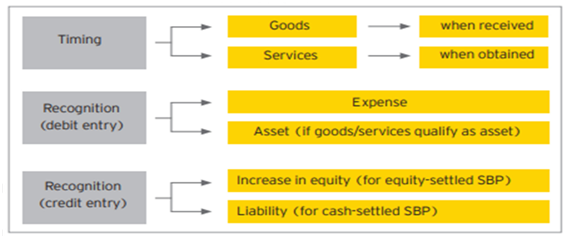

3. RECOGNITION

• Recognise the goods or services received or acquired in a share-based payment transaction when the goods are obtained or as the services are received.

• Recognise an increase in equity for an equity settled share-based payment transaction.

• Recognise a liability for a cash-settled share based payment transaction.

• When the goods or services received or acquired do not qualify for recognition as assets, recognise an expense.

(Source: EY)

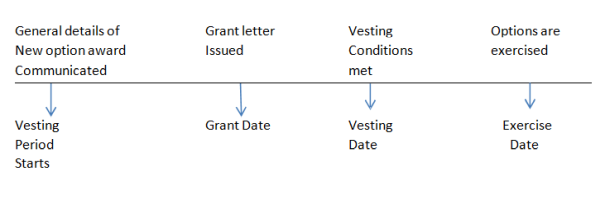

4. Grant Date

IFRS 2: "the date at which the entity and another party (including an employee) agree to a share-based payment arrangement, being when the entity and the counterparty have a shared understanding of the terms and conditions of the arrangement"

5. CLASSIFICATION

Equity settled: settled in equity instruments of the entity (or another entity in the group)

Cash settled: settled in cash, based on the price (or value) of the entity's shares

Settlement alternatives:

- Counterparty (e.g. LTI participant) has choice:

• Treat as compound instrument

• Measure debt and equity as separate parts

- Company has choice:

• Treat as equity-settled unless past practice or policy is to settle in cash.

6. MEASUREMENT

A. Equity Settled

Transaction with employees

• Measure fair value at grant date of equity instrument

• Fair value is never measured

• Recognised Assets or Expenses over vesting period Transaction with non-employee

• Measured at fair value of goods or services which are obtained or received.

• If the fair value of the goods or services received cannot be estimated reliably, measure by reference to the fair value of the equity instruments granted.

B. Cash Settled

• Measure the liability at the fair value at grant date.

• Fair value shall be re measure at each reporting date, if any differences transfer to Profit and loss account.

• Liability is recognized over the vesting period.

C. Choice of Settlement

Counterparty (e.g. LTI participant) has choice:

• Treat as compound instrument

• Measure debt and equity as separate parts

Company has choice:

• Treat as equity-settled unless past practice or policy is to settle in cash.

7. Valuation

Equity settled:- Measured at fair value at grant date.

Cash settled:- Fair value of Liability incurred.

8. Group settled share-based payments (IFRS Para 43C)

The entity receiving the goods or services will recognise the transaction as equity-settled only if:

• The awards granted are its own equity instruments; or

• It has no obligation to settle the transaction

In all other circumstances, the entity will measure the transaction as cash-settled.

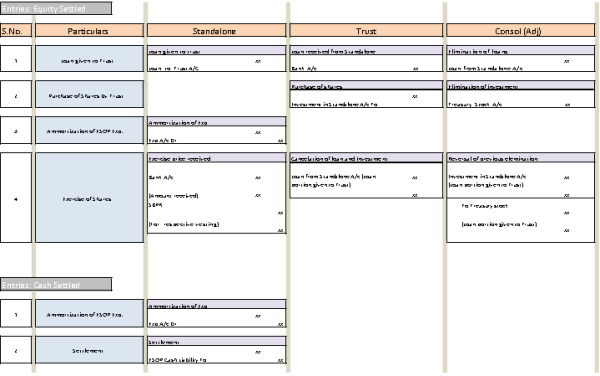

9. Practical application

SBPR-Share Based payment reserve A/c

CAclubindia

CAclubindia