This is a concept note on MIS, which attempts to cover many types of Business Models we normally see. Accordingly, to any particular organization, only some of the modules covered here would be relevant.

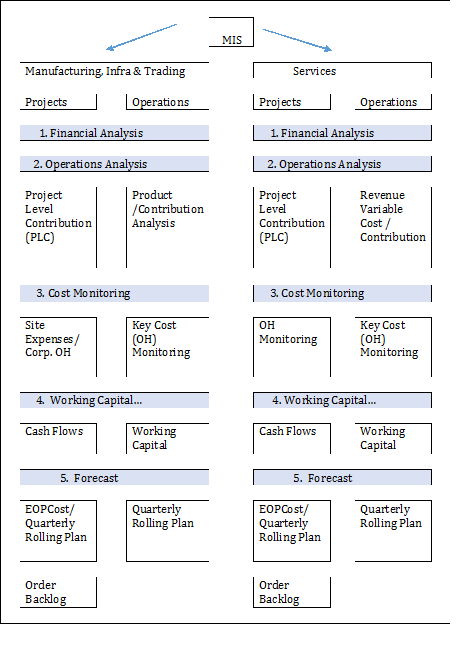

As you see in the chart below, an organization could be in Manufacturing, Infrastructure Business, in Trading or in Services. In each of these categories, they may be in Projects Business or in Operations, or in a combination of both. Companies may operate as different Lines of Business (LOBs) or operate as one unit.

First step in designing / upgrading MIS is to place your organization in one or more slots, based on the business model. Then look at the possible modules in which MIS could be organized. Where management is not aware as to what kind of MIS they should look for (which is the case with many organizations), it is the task of the concerned Manager, CFO or Consultant to set the expectations toward the need for meaningful, relevant and effective MIS, and attempt to develop such MIS.

Broadly MIS has 2 objectives:

- To assist top management in driving performance

- To help operating management in improving efficiencies.

Keeping these two objectives at the back of our mind let us see how we could proceed with our MIS.

This article is organized under the following 5 sub-headings:

- Financial Analysis

- Operations Analysis

- Cost (Overhead) Monitoring

- Cash Flows, Working Capital, ROI and Fixed Assets

- Forecasting (to set up short term goals for performance monitoring)

First let us look at the chart to place your organization in the slot relevant to its business model:

1. Financial Analysis:

This is common to all types of organizations.

Prerequisites:

Monthly Closing Checklist should be used for proper preparation of Monthly Accounts, and it should include all reconciliations, to validate the balances in the books and for a proper drill down of accounts for any analysis.

P&L and Balance Sheet:

Once you have a proper reconciled Trial Balance, you need to prepare P&L for the month, and cumulative to date, as well as Balance sheet as at the end of the month. If there is a Budget, broken down to monthly intervals, you could add a column for the Budget, otherwise or in any case add a column for the previous month. Identify balances of all significant accounts (any account which exceeds 10% of its total in the P&L or Balance Sheet) make them bold, add a Remarks column and offer explanation for movement over the previous month, and its main constituents even if there is no movement.

2. Operations Analysis:

From here we cover MIS, based on the specific business model of the organization.

Project Level Contribution (Infrastructure - Projects)

Ensure that Financial Accounting is properly structured with suitable Cost Codes, to generate Project-wise details of Revenue & Direct Costs & Indirect Costs at Site level, to generate PLC Report. This is relevant for a period, which is usually a quarter. If a Quarterly Rolling Plan has been prepared, ahead of a quarter, projecting anticipated PLC from each project, actual could be compared against such a projection. Consolidation of PLC of all projects in an organization sums up to match with the company level PLC, and acts as a good compensating control to Financial Reporting.

Product Contribution / Contribution Analysis:

For manufacturing / trading organizations, which are not into projects business, this is applicable. This could be at a Product Level or at LOB Level or at a company level, based on what type of structure is relevant. Sales minus Variable Cost is Contribution. Variable costs are usually direct material costs. Where power cost is significant and varies with level of activity, it could also be included in Variable cost. Direct Labor is also Variable Cost, though it behaves as a fixed cost in the short term.

Break Even Level, Current Level of operations as a percentage of B E Level, or Capacity as a percentage of B E Level are good indicators on vulnerability of operations tomove from profit to loss making situation and vice versa.

Project Level Contribution – Services Industry:

Most familiar example is Software companies which are into projects, on Fixed Price basis. Here Variable Costs are mostly manpower costs, and sometimes data Link charges which are substantial could get included. Travel for project execution is included. Contribution % is normally monitored at project level and is considered a norm across the industry.

Contribution Analysis – Services Industry:

Software companies which operate on T&M (Time and Material) assignments fall in this category. Here customer level contribution is usually monitored. Other companies which can fall into this category are event management companies, logistics companies and the like. However, in companies where variable cost is low, Contribution Analysis gets secondary importance in profit planning.

3. Cost Monitoring:

We mainly cover Overheads in this component of MIS.

Infrastructure – Projects:

Site Expenses which are indirect in nature (though included in PLC Report) could be monitored through this report. Head Office Expenses, Depreciation, Interest are important in this category. Usually these are compared against the budget. Where organizations do not follow budgeting as a tool for monitoring performance, a quarterly projection of such costs with actuals is useful.

Manufacturing /Trading: Other than Projects – Key Cost Monitoring:

We could also call this Top 10 Cost monitoring. There is no “one size fits all solution” but this area offers significant scope for monitoring costs. Looking at each cost item on “zero” basis, introducing Commitment Control, reporting Discretionary Costs on monthly basis, Departmental Budgeting and reporting actuals against budget, relating costs to KPIs like cost per sqft, cost per employee, cost per seat, yield per unit of input are some of the ways in which these costs could be reported for monitoring.

Cost Monitoring – Services Industry:

Overheads monitoring here is similar to what has been covered under Manufacturing / Trading.

4. Cash Flows, Working Capital, ROI and Fixed Assets:

Distinction between Manufacturing and Services is significant to the extent factors which influence Working Capital and relative magnitude may be more in the case of the former. Similarly, while projecting Cash Flows, in the case of Projects Business, it may be convenient to work at project level.

Cash Flows:

For Start Ups and SMEs, tendency is to mix up long term funds with short term working capital and vice versa. If we can design reports which highlight such instances, it will be very useful.

In large companies in projects business, where a good ERP is in use, since milestones relating to procurement, construction, billing and collections are in the system, it is possible to derive and project cash flows on a continuous basis, to predict shortfalls or surplus cash situations.

Working Capital Monitoring:

Age-wise Analysis of Inventory, WIP, Finished Goods, Receivables is well known as an MIS Report. But more than history, projecting movement up to next 3 months and expediting actions to monitor working capital is more effective. Thus, in the case of non-moving inventory, we should pick up high value items and check with operating personnel on when are the items likely to be used, and recommend decisions like retaining in stock, scrapping, or giving discounts as appropriate. For receivables monitoring one of the useful reports is tagging a customer or a group of customers to Sales Personnel setting collection targets and reporting Receivables Sales person-wise.

Return on Investment:

In some organizations which operate as LOBs, it is useful to identify Capital Employed (Fixed Assets and Working Capital) under each LOB, and see PBT as a percentage of Capital Employed. Even in organizations which operate as one entity, comparing ROI of different periods is useful.

Fixed Assets:

Investment in Fixed Assets is usually not covered in MIS. But Capex Planning justification for acquiring assets, and post-acquisition analysis of the benefits is useful. Other important aspects relating to Fixed Assets are review of Capacity Utilization and Idle Time Analysis. Random verification of a few fixed Assets each month and tracing them to the FA Register is useful to know quality of Fixed Asset Record and related controls.

5. Forecasting:

Prompting Operating managers to Forecast on key performance parameters, in the short run, getting their commitment, providing resources required if any, and making them accountable for results, is perhaps the most effective way of monitoring performance.

Infrastructure – Projects – End of Project Cost Estimate:

In the case of projects, two kinds of costs are incurred. They are:

- Direct Material & Labour costs which are related to output and

- Period based costs like Site Expenses.

At the commencement of a project, Cost Estimate under the above categories is made. After that, Purchase Orders are finalized and released according to project schedule. During the course of the project execution, taking Purchase Orders released as commitments made, and reviewing balance to commit for completing the project, it is possible to estimate total cost for completion in this category of costs. Similarly, in the case of Period Costs like Site Expenses, any delay in the project completion date (or even completing ahead of schedule) can be used for projecting the cost to complete in this category of costs. Thus it is possible to estimate EOP cost during project execution, which is a very useful report to the management.

Infrastructure – Projects – Quarterly Rolling Plan:

In Projects Business, visibility on what is feasible for execution is usually available only for a short period, say a quarter. Quarterly Rolling Plan is a bottoms-up plan, by projecting from the milestones of each project at the beginning of a quarter as to what could be achieved during the ensuing quarter. Consolidating the data relating to all projects under execution, a Quarterly Rolling Plan (of stretch targets) of Revenues and Cost is prepared. Such a plan is also used for taking stock of resources like funds, material and manpower and suitable procurement actions are taken. At the end of the quarter, actual performance is compared with the Quarterly Rolling Plan, and next Quarter’s plan is firmed up.

For Manufacturing Companies which are into Operations as well as for Services Industry, Quarterly Rolling Plan is relevant.

Order Backlog – Pipeline Report:

This report is relevant for all companies in Projects Business. Some of the large construction companies even declare Order Backlog in their corporate communications.

In the planning exercises of these companies, they take stock of Order Backlog on hand, project what they are likely to bag during the plan period, and execute, to ensure that adequate order backlog is always available. This report may influence the company’s pricing strategy.

By using the information relating to projected contribution from each of the orders in the pipeline, these companies even make Earnings Estimate.

For a company in Projects Business, with 3 Divisions, Order Backlog movement, projected in their Budget could be as under:

|

Division-> |

A |

B |

C |

Total |

|

Quarter 1 |

||||

|

Opening Backlog |

||||

|

Order Booking Plan |

||||

|

Order Execution Plan |

||||

|

Closing Backlog |

||||

|

Quarter2 |

Concluding Remarks:

Organizations in the New Economy are growing fast on the strength of their intangible assets. These are assets in the form of Customers, Employees, Vendors, Channel Partners, as well as the organizational strategies, Policies, internal Processes and leadership. While the last cannot be put in MIS, its impact would get reflected in the growth of other intangible assets, which could be suitably planned through effort based milestones, monitored and reported through meaningful MIS.

Thank you for your attention.

For more articles from me, please read my book “Translating Operations into Money – Cases in Business Management” available for online purchase at Amazon.in or Flipkart. You could also visit www.operationstomoney.com , to know more about my book.

CAclubindia

CAclubindia