Guidelines for replacement of existing Rs 500 and Rs 1000 notes with new notes and to understand the procedure of scheme and relevant provisions of Income Tax.

1) In terms of Gazette Notification No 2652 dated November 08, 2016 issued by Government of India, Rs. 500 and Rs. 1,000 denominations of Bank Notes of the existing series issued by Reserve Bank of India (hereinafter referred to as Specified Bank Notes) shall cease to be legal tender with effect from 9th November, 2016, to the extent specified in the Notification.

Objective

With a view to curbing financing of terrorism through the proceeds of Fake Indian Currency Notes (FICN) and use of such funds for subversive activities such as espionage, smuggling of arms, drugs and other contrabands into India, and for eliminating Black Money which casts a long shadow of parallel economy on our real economy, it has been decided to cancel the legal tender character of the High Denomination bank notes of Rs.500 and Rs.1000 denominations issued by RBI till now. This will take effect from the expiry of the 8th November, 2016

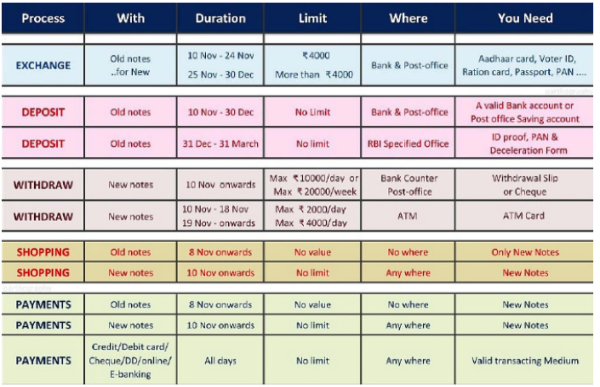

2) Withdrawal from ATMs would be restricted to Rs. 2,000 per day per card up to November 18, 2016. The limit will be raised to Rs. 4,000 per day per card from November 19, 2016 onwards.

3) Limit on amount to be exchanged during November 10, 2016 to December 30, 2016

One can exchange upto Rs. 4,000 per person in cash irrespective of the size of tender and anything over and above that will be receivable by way of credit to bank account.

4) For those who are unable to exchange their Old High Denomination Bank Notes or deposit the same in their bank accounts on or before December 30, 2016, an opportunity will be given to them to do so at specified offices of the RBI on later dates along with necessary documentation as may be specified by the Reserve Bank of India.

5) Bank Branch for exchange of old bank notes:-

One can go to any branch of any bank. In that case one has to furnish valid identity proof for exchange in cash. (Valid Identity proof is any of the following: Aadhaar Card, Driving License, Voter ID Card, Pass Port, NREGA Card, PAN Card, Identity Card Issued by Government Department, Public Sector Unit to its Staff). Please also carry original identity proof for verification.

6) Should one go to bank personally or can one send the notes through representative?

In case it is not possible for a person to visit the branch then the person may send representative with an express mandate i.e. a written authorization. The representative should produce authority letter and his / her valid identity proof while tendering the notes.

7) Limit on amount of cash withdrawn against cheque:

One can withdraw cash against withdrawal slip or cheque subject to ceiling of Rs. 10,000/- in a day within an overall limit of Rs. 20,000/- in a week (including withdrawals from ATMs of Rs. 2000/4000 per day) upto 24th November 2016, after which these limits shall be reviewed.

8) If any person right now not in India, what should he/she do?

If the person has Specified banknotes in India, he/she may authorize in writing enabling another person in India to deposit the notes into his/her bank account. The person so authorized has to go to the bank branch with the Specified bank notes, the authority letter given by the person and a valid identity proof (Valid Identity proof is any of the following:

Aadhaar Card, Driving License, Voter ID Card, Pass Port, NREGA Card, PAN Card, Identity Card Issued by Government Department, Public Sector Unit to its Staff)

9) If any person is NRI and hold NRO account, can the exchange value be deposited in my account?

NRI can deposit the Specified banknotes to his/her NRO account.

Time limit of the Scheme

Time limits for deposit /exchange/withdrawal in tabular form is as given below

10) How much cash can be deposited

The person who maintains/is required to maintain books of accounts, the cash appearing in books of account as on 08-11-2016 can be deposited without any limit. Books should be updated upto 08-11-2016 and only cash available as per books can be deposited. Any amount deposited in bank should be corroborated with evidence through books or cash flows, where there are no books. However if the source is unexplainable then as per instructions it will be taxed @30% along with penalty @200% i.e. total tax liability could be 90% of unexplained cash. The department may raise question on amount deposited exceeding Rs. 2.5 lacs during November 10, 2016 to December 30, 2016.

11) Whether all cash available as on 08-11-2016 needs to be deposited

If all cash is in denomination of 500/1000 then all cash needs to be deposited or exchanged upto the value of Rs. 4,000. However the cash available in denomination of 100 or less can be kept as cash.

12) Whether cash needs to be deposited in one account

The amount can be deposited in all bank accounts. There is no condition to deposit all cash in one bank account.

13) Amount to be reported by Banks in AIR to income tax department

As per the provision of rule 114E:

Normally in AIR the amount deposited in saving bank account Rs. 10 lacs or more annually needs to be reported by bank to income tax department. Further in current account, amount deposited/withdrawn exceeding Rs. 50L needs to be reported.

However as per the statement (Tweet) given by Mr. Hasmukh Adhia, the income tax department may seek the information for deposit of cash exceeding Rs. 2.5 lacs during the period November 10, 2016 to December 30, 2016. The income tax department may raise queries and ask for explanation on such deposit. The tax liability could be as explained above.

14) Is there any restriction for cash sale before 08-11-2016 or after 08-11-2016

As per provisions of rules 114B to 114E, the seller is required to mention the PAN number on sale invoice exceeding Rs. 2 lacs. If the buyer is not having PAN then Form 60 needs to be taken and Form 61 needs to be filed with the department. Further as per the provisions of Section 206C – TCS needs to be collected @1% on cash sale exceeding Rs. 2 lacs.

Further as per provision of rules 114B to 114E, if cash are received from any person exceeding Rs. 2 lacs per year then the detail needs to be reported to income tax department in Form 61A.

Cash sale from 09-11-2016 onwards cannot be against notes 500/1000 as these are not legal currency except for specified seller.

The seller who is liable to tax audit will be required to maintain the person wise detail (including Name, Address and PAN/Form 60 ) of cash sales for computing the threshold limit of Rs. 2 Lakh received from such person.

15) Provisions related to cash purchase

As per the provisions of Section 40A(3) of the Income Tax Act, cash purchase exceeding Rs 20,000 will not be allowable as business expenses. Therefore cash purchases can be made upto Rs 20,000 per invoice in day.

Notification No 2652 dated November 08, 2016 is enclosed for ready reference. Please also find enclose herewith FAQs issued in respect of withdrawal of Legal Tender Character of the existing Bank Notes in the denominations of Rs. 500/- and Rs. 1,000/-.

Disclaimer: The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. The observations of the author are personal view and the authors do not take responsibility of the same and this cannot be quoted before any authority without the written permission of the author.

Regards,

CA Neeraj Kumar

CA Deepak Arya

Parveen Goyal

Recommended read : Probable reason why Rs 2000 note are being issued

CAclubindia

CAclubindia