A. Meaning

- Streamline all the different types of indirect taxes and implement a “single taxation” system. This system is called as GST (GST is the abbreviated form of Goods & Services Tax).

- GST is a comprehensive tax levy on manufacture, sale and consumption of goods and services at a national level.

- GST is a system which will convert the country into a unified market by replacing all indirect taxes with one tax i.e. bringing all indirect taxes under a single umbrella.

B. Integration

- Our GST model, as we all know, will have two lines of taxes across the supply chain with credits across these lines of GST.

C. Basic Purpose

- Single umbrella Tax Rate: GST will replace a number of indirect taxes being levied by union and state governments under a single umbrella.

- Removal of Cascading Effect: The current tax system contains many distortions that result in substantial tax cascading and inefficient production and consumption structures, which hinder economic growth. GST would remove these distortions, paving the way for a higher GDP.

D. Features of GST

- Comprehensive Base: It shall apply to supply (as defined in the Act) of all goods and services except alcoholic liquor for human consumption and petroleum and petroleum products.

- Revenue Neutral Rate of GST: It is the rate at which tax revenue will remain same, despite allowing input tax credit and other factor. Therefore in GST regime it is an adjusted rate at which revenue of the government would be same as comparison with the present tax structure.

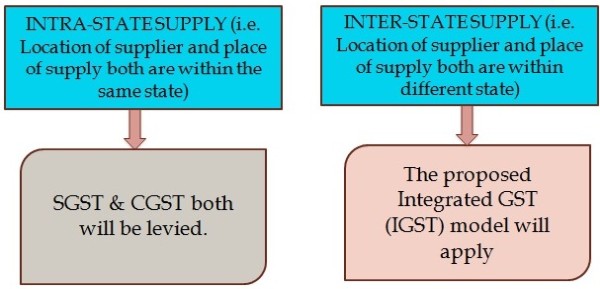

- Place of Supply: GST is expected be levied only at the destination point, and not at various points (from manufacturing to retail outlets).

- PAN Linked TIN No.: Each taxpayer would be allotted a PAN-linked taxpayer identification number with a total of 13/15 digits. This would bring the GST PAN-linked system in line with the prevailing PAN-based system for Income tax, facilitating data exchange and taxpayer compliance.

E. Impacts of GST

- GST is expected to lead to a GDP growth addition of 2 percentage points, other things being equal.

- GST will impact the entire value chain of operations, namely procurement, manufacturing, distribution, warehousing, sales, and pricing. It will also trigger the need to relook at internal organization and IT systems.

- Taxpayers will also benefit with GST, as they will no longer have to grapple with multiple State taxes or complicate their accounting practices to comply with numerous tax laws.

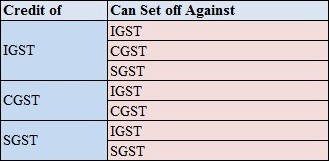

- Set off Rules under GST: Since the Central GST and State GST are to be treated separately; taxes paid against the Central GST shall be allowed to be taken as input tax credit (ITC) for the Central GST and could be utilized only against the payment of Central GST. The same principle will be applicable for the State GST.

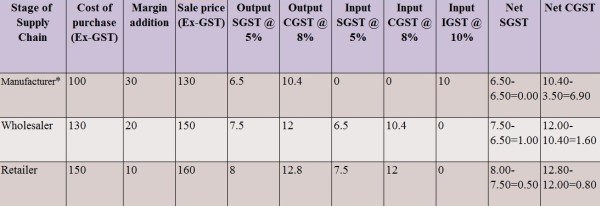

F. Illustration for GST Model:

The Illustration shown below indicates how GST will work assuming IGST rate is 10%, CGST rate is 8% and SGST rate is 5%.

*It is assumed that goods have been purchased Inter-state and sold Intra-state.

CAclubindia

CAclubindia