Rule 42 of the Central Goods and Service Tax Rules, 2017 determines the manner for the calculation of ITC on input and input service to be reversed.

To understand the rule, first determine the following for a tax period say July 2017:

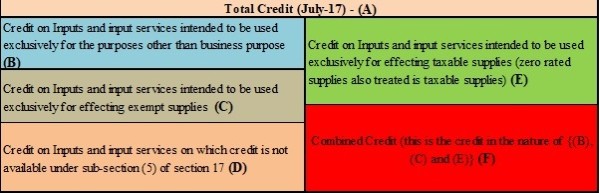

- Total input tax involved on inputs and input services in a tax period.

- Credit on Inputs and input services intended to be used exclusively for the purposes other than business.

- Credit on Inputs and input services intended to be used exclusively for effecting exempt supplies.

- Credit on Inputs and input services on which credit is not available under sub-section (5) of section 17.

- Credit on Inputs and input services intended to be used exclusively for effecting taxable supplies (zero-rated supplies also treated as taxable supplies).

- Turnover of exempt supplies during the tax period.

- Total turnover during the tax period.

The different credit component can be seen in the below diagram:

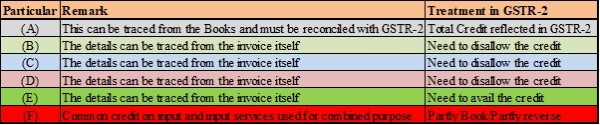

From the above chart it is quite clear that:

Treatment of the said credits in the form GSTR-2 is given below:

Invoice level details must be inserted in the form GSTR-2 for (B) to (E).

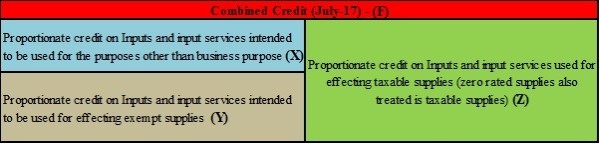

The combined credit can be bifurcated into the below components:

From the above it is clear that (X) and (Y) are the amounts that need reversal and the same shall be calculated in the following manner:

The reversal of the same can be done by way of adding in the output liability of the same tax period. Hence (X) and (Y) shall be added to the output liability of that particular tax period.

Yearly activity:

The reversal of credit must be done for each tax period i.e. on monthly basis. And also on yearly basis.

If the sum total of credit reversal of each tax period exceeds the yearly combined amount then the difference shall be taken as the credit before the September of the following year. OR

If the sum total of credit reversal of each tax period falls short of the yearly combined amount then the difference shall be added to the output tax liability in any tax period before the September of the following year.

This calculation shall be done for each tax component i.e. CGST, SGST, and IGSTfor each tax period.

CAclubindia

CAclubindia