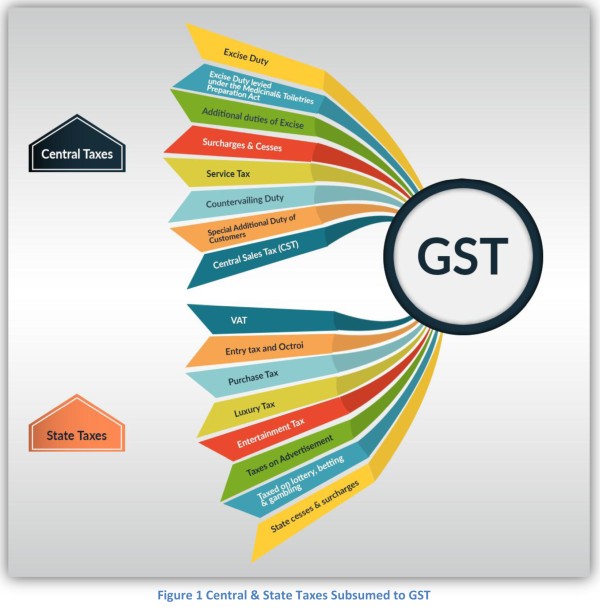

The Goods and Services Tax (GST) promises to bring a single unified tax regime for India, which will consolidate many different taxes into a single tax regime.

Some of the taxes to be subsumed into GST

- VAT

- Service Tax

- Excise

- Entertainment Tax

- Entry Tax

A single tax regime will bring predictability and lower operating costs for businesses because the GST will reduce the overall tax burden by reducing the impacts of cascading taxes and allow the cross-utilization of tax credits across the supply chain.

IT teams will be wondering what they will need to be doing from a planning and implementation stage to update and review ERP systems to be ready for the GST. Now these changes could be as simple as updating the version but in most cases it is not so simple. A change in an ERP requires a coordinated effort between tax, IT and other departments to ensure success. The on going challenge with the GST has been a situation where the implementation date and requirements keep shifting. Over the last several months, many projects have started to upgrade, fix and design new functions and processes in ERPs to prepare for the change. This continuous effort is costly and spends countless hours and so far systems are not yet ready for the GST because it is not clear what they need to be ready for.

While the general understanding of the tax and its impact on business have remained unchanged the implementation date has been missed several times slipping forward each time and with each change in the implementation date more small changes are introduced into the legislation. Parliament failed to vote on the model law in the recent legislative session and now it will be delayed until late January for implementation which means 1 April 2017 is a harder dead line to reach.

Generally speaking, the GST will require businesses to revisit the following areas in their ERP:

- Procurement or Materials modules

- Sales or supply chain modules

- Financial management modules

Each of these modules are impacted with the change to GST.

One of the challenges with the GST, will be a widening of the taxable basis because now the provision of almost any type of good or services is taxable. GST transitions the taxable event from sales, distribution, manufacture, and provision to simply the event of a supply.

When considering the number of rates which can apply to a supply there could be a reduction in the total number of rates and variations because the GST Council will approve all rate slabs. However, it remains to be seen what will occur because when VAT was introduced there were only three main rates: 12.5%, 4% and 1% but today there are a multitude of rates across the states along with different cesses.

Any change in rates is still a major ERP event because you have to create new tax codes, conditions and update information about products and materials.

Businesses which used to only be involved in the provision of certain types of supplies will make sure all their ERP processes are considering tax. It is important to spend time reviewing your existing process or business flows to understand where tax consequences could change. For example, in the case of the supply of goods between two units of the same business the change could be that it went from 2% CST on the sale to 18% IGST on the supply of the goods. [Can we have a graphic for this showing how a supply from MH to TG is 2% today but could be 18% when GST comes?] This change has impacts on how orders are taken, goods are received, materials and reporting for internal purposes and compliance reporting.

Specifically, for tax compliance, ERPs should produce data which can be used to create the appropriate entries into the GSTN for outward and inward transactions and make sure valid tax invoices can be created. The requirement to upload data to the GSTN pushes the requirement to create accurate tax specific data up the chain to the ERP rather than trying to fill in the data at a later point for compliance. ERPs need to capture the relevant data or can fill in missing data as the process runs through before the compliance begins. If a business attempts to create the data at the time of compliance this can lead to delays and mismatches with invoices which are already created.

Tax teams will need to either take on the responsibility and engage advisors depending on the complexity of the business to understand which business processes will remain the same, which can be optimized under the GST and which will no longer be relevant. These findings will need to be consolidated and presented across the organization. Then it will fall to a combination of Tax and IT to develop the implementation and testing plan, implement it and then test to ensure it is working.

All components of the ERP require maintenance and so as the GST stabilizes there will be an increased strain on Tax and IT teams to continuously update, test and re-visit scenarios as the business processes evolve after the GST. Any ERP migration strategy should include an increase amount of time for maintenance and re-evaluation until at least 18 months after the operation of the GST.

An alternative to this seemingly endless cycle of ERP design, build and test is a solution which centralizes the tax information in a central place. The advantages to a tax information system are it allows the tax system to provide the tax specific values back to the ERP. The ERP maintenance focuses on items ERPs excel at such as accounting, workflow and processing management; while the tax system takes over for the computation and compliance. When coupled to a billing system the tax system can provide a solution for all the tax-sensitive data which is separate from the ERP. Therefore, mission critical ERP tasks are not interrupted with governance, risk, and compliance changes.

CAclubindia

CAclubindia