Real estate industry is one of the most important pillars of the Indian economy. Real estate industry contributes between 6- 8% to India's Gross Domestic Product (GDP) and it stands second after IT industry in terms of employment generation.

With multiple taxes applicable previously like Service tax and VAT, with GST coming into the picture, indirect taxation in this sector is wholly revamped.

Construction services other than those specifically exempted are chargeable to tax under GST.

Real Estate sector generally comprises of 4 types of transactions:

a. Supply of real estate property before completion (either commercial or residential purpose).

b. Supply of real estate property after completion (commercial/ residential)

c. Supply of land (agricultural/residential/commercial)

d. Supply of rights arising out of land (such as TDR)

We will discuss GST impact on all the above transactions.

Taxable event in case of construction services:

As per clause b of paragraph 5 of Schedule II of CGST Act, 2016, the following shall be treated as Supply of service:

'Construction of a complex, building, civil structure or a part thereof, including a complex or building intended for sale to a buyer, wholly or partly, except where the entire consideration has been received after issuance of completion certificate, where required, by the competent authority or after its first occupation, whichever is earlier.

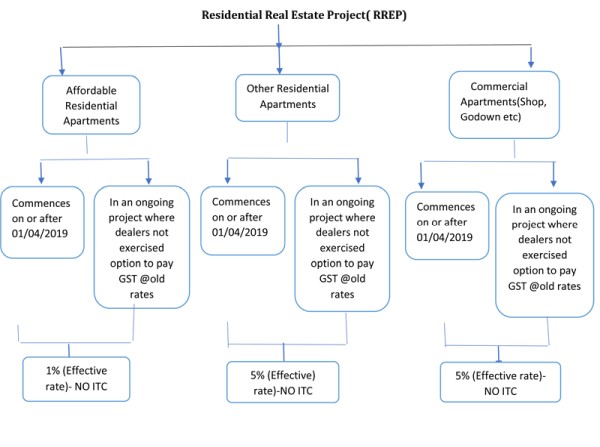

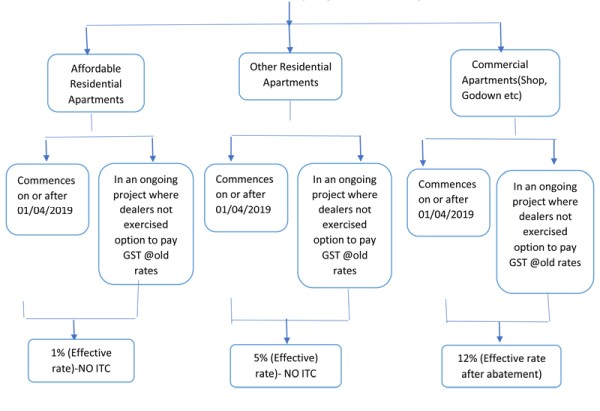

Rate of GST on construction services upto 31st March 2019

The following are GST rates for under construction projects upto 31st March 2019:

1. GST @12% was leviable (after 1/3rd deduction towards land value) on supply of flats before completion.

2. Concessional rate of 8% was applicable for units qualifying for Affordable Housing.

After considering the various difficulties faced by Real estate dealers, the GST council in its 33rd and 34th council meetings held, various notification were issued to give relief to real estate dealers:

The list of notifications relating to this sector

|

Notification No |

Particulars |

Effective from |

|

3/2019 (CTR) |

Changes in GST rates |

1st April 2019 |

|

4/2019 |

Exemption to TDR, FSIand land premium |

1st April 2019 |

|

5/2019 |

RCM for TDR, FSI and land premium |

1st April 2019 |

|

6/2019 |

Time of Supply for JDA |

1st April 2019 |

|

7/2019 |

RCM for 80% criteria |

1st April 2019 |

|

8/2019 |

Rate of RCM |

1st April 2019 |

|

16/2019(CT) |

Changes in GST Rules (Rule 41, Rule 42, Rule 43) |

1st April 2019 |

|

ROD 4/2019 |

Credit attributable to be determined based on carpet area |

1st April 2019 |

The new rates are as follows:

Construction in a Real Estate Project (Other than RREP)

Important definitions in the new scheme of taxation:

1. RREP- shall mean a Real Estate Project

b. is not more than 15 percent

c. of the total carpet area of all the apartments in real estate project.

2. Meaning of Carpet Area:

The term carpet area shall have the same meaning as assigned to it under clause (k) of Section 2 of RERA Act, 2016 which reads as below:

a. the term carpet area means -

b. the net usable floor area of an apartment

c. excluding-

d. the areas covered by external walls;

e. area under service shafts;

f. exclusive balcony/veranda; and

g. exclusive open terrace area;

h. but including area covered by internal partition walls.

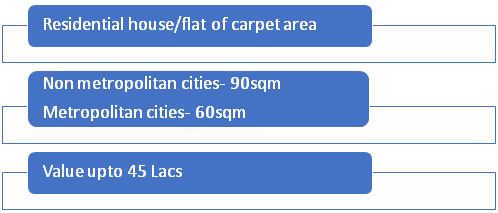

3. Affordable Residential Apartments:

4. Meaning of Ongoing Project:

A project which satisfies the following conditions, can be called a Ongoing Project

Commencement certificate issued on or before 31.03.2019 by-

a) Chartered Engineer,

b) A licensed surveyor of respective local body

Completion certificate has not issued or first occupation has not taken place on or before 31.03.2019

Apartments being constructed under the project have been partly or wholly booked on or before 31st March 2019.

Construction shall be considered to have started on or before 31/03/19

a) the earth work for the site preparation for the project has been completed AND

b) excavation for the foundation has started on or before 31st March 2019.

Now there are two options for Real Estate Dealers.

The biggest question is whether to opt for new scheme or to continue with old scheme for ongoing projects

The analysis of both the options is given below:

|

Old scheme |

|

|

Project consists of 10 flats |

|

|

Each Flat costs |

25,00,000.00 |

|

ITC available in credit ledger |

27,00,000.00 |

|

Flats sold before OC |

7 |

|

Flats sold after OC |

3 |

|

Value of supply liable to GST (25 lacs x 7) |

1,75,00,000.00 |

|

Intra State tax liability @ 12 % |

21,00,000.00 |

|

Balance available |

6,00,000.00 |

|

Exempted sales i.e., flats sold after OC (25 lacs x 3) |

75,00,000 |

|

Total Turnover |

2,50,00,000 |

|

ITC to be reversed due to exempted sales under Rule 42 i.e. 27lacs x 3flats / 10 flats. |

8,10,000.00 |

If new scheme is adopted for ongoing projects, then additional cash flow will be:

a. ITC for that project is to be reversed along with interest

b. Regular tax liability @ 1%/5% resp.,

Therefore, it may be concluded that, in case of ongoing projects, based on inflow and outflow of tax, old scheme of tax rates is suggestable.

New scheme of tax rates

In case of new projects started on or after 01.04.2019, the GST implications will be as follows:

|

New Scheme |

|

|

Project consists of 10 flats |

|

|

Each Flat costs |

25,00,000.00 |

|

ITC available in credit ledger |

0 |

|

Flats sold before OC |

7 |

|

Flats sold after OC |

3 |

|

Value of supply liable to GST |

1,75,00,000.00 |

|

Intra State tax liability @ 1 % |

175000 |

|

Balance available |

0 |

|

Exempted sales i.e., flats sold after OC |

75,00,000 |

|

Total Turnover |

2,50,00,000 |

|

ITC to be reversed due to exempted sales under Rule 42 |

No reversal since no ITC was utilised to discharge tax liability |

Conditions applied for a RREP/REP to get benefit of GST rates of 1%/5%:

Reverse ITC based on carpet area (Annexure I and Annexure II) for supply of construction services- whose time of supply falls on or after 01.04.2019.

In case of JDA, builder liable to pay tax for supplies made to land owner and land owner is eligible to take ITC of such tax.

80% of value of inputs and input services - other than TDR, Electricity, HSD, Motor Spirit, and Natural Gas- only from registered supplier.

Inputs & Input services from registered supplier<80% RCM tax @ 18%*(80% value- Actual value).

If cement is purchased from URD then tax shall be paid under RCM at the rate applicable to it. Tax to be paid in the month in which cement is received.

Inward supplies from RD & URD- - - Project wise- - - submit in prescribed form- - by end of quarter following the FY.

The tax liability on the shortfall purchases from URD - to be paid in month of June following the end of the financial year.

RCM Goods and services shall be deemed to have been purchased from registered suppliers.

Total ITC to be shown as - Ineligible ITC in GSTR- 3B (every month).

Two rates for discharging RCM liability:

For cement- 28%

Transitional Effects with adoption to New scheme from Old scheme for Ongoing projects

1. Major relief after introduction of GST is availability of ITC on all the inputs used in the supply of Construction services.

2. Major input in Construction sector is Labour and Cement purchase. Most of the suppliers of cement and labour are unregistered.

3. It can be managed in the old scheme with unregistered suppliers. But if new scheme is adopted 80% of the total Inputs should be from registered suppliers only. This will be a burden to Builder.

4. And No ITC is allowed, entire tax liability is to be discharged in cash only, so there will be huge cash flow.

5. If new scheme is availed, for supply of flats in ongoing projects on or after 01.04.2019, ITC reversal to be done along with interest.

The following are the scenarios where ITC is available or not.

|

Sl No. |

Project |

Particulars |

Impact on ITC |

Refer |

Remarks |

|

1 |

Ongoing(RREP/REP) |

Old scheme |

ITC available |

Section 171 |

Sale of units after completion will trigger reversal (As per Rule 42 & 43 of CGST Rules) |

|

2 |

Ongoing(REP) |

New scheme |

ITC reversal will trigger |

Annexure I and II of Not. No. 3/2019 |

Sale of units after completion will trigger reversal (As per Rule 42 & 43 of CGST Rules) |

|

3 |

Ongoing(RREP) |

New scheme |

ITC reversal will trigger |

Annexure I and II of Not. No. 3/2019 |

Refer Rule 42(5) of CGST Rules |

|

4 |

New(REP) |

New scheme |

ITC reversal will trigger |

Rule 42/ 43 of CGST Rules |

Sale of units after completion will trigger reversal( As per Rule 42 & 43 of CGST Rules) |

|

5 |

New(RREP) |

New scheme |

ITC not available |

NA |

NA |

# RREP- Residential Real Estate Project

# REP- Real Estate Project (not residential)

Amended CGST Rules with respect to Input Tax Credit reversal for Construction Services.

Where the goods or services or both are used by the registered person partly for effecting taxable supplies including zero- rated supplies and partly for effecting exempt supplies the amount of credit shall be reversed to the extent of exempt income by following the rules prescribed below:

Rule 42- Manner of determination of input tax credit in respect of Inputs and Input services and reversals thereof

Let us assume that,

- T= Input tax credit on inputs + services

- T1= Input tax credit of inputs used other than business

- T2= Input tax credit on exempt supplies

- T3= Input tax credit on 17(5) supplies

- Input tax credit in Electronic Credit Ledger (C1)= T- (T1+T2+T3)

- T4= Input tax credit on taxable supplies incl. zero rated supplies

** In case of supply of services as per Sch- 2 para 5 clause b, ITC = 0

- Common Credit(C2)= C1- T4

- Credit on Exempt supplies = C2 x E/F (E= Exempt supplies , F= Total Turnover)

** In case of supply of services as per Sch- 2 para 5 clause b,

- Credit on Exempt supplies = C2 x E/F (E= Carpet area of Apartment {exempt from tax + not exempt from tax, but booked after OC}, F= Aggregate Carpet area).

- D2= C2 x 5% ( In case business not relevant)

- Reverse D1 & D2

- Eligible ITC C3= C2- (D1+D2)

Calculate the credit reversal for year ending to both normal supplies and the supplies made under Sch- 2 para 5 clause b

- If actual credit reversed > credit reversal arrived as per Rule 42, then claim as credit in his return till the next September return.

-

If actual credit reversed < credit reversal arrived as per Rule 42, then reverse including interest from April of next year till payment.

In case of supply of services as per Sch- 2 para 5 clause b, calculate for each ongoing project and for the projects on or after 01- 04- 2019 on which no transition of ITC is availed.

Calculate ITC for commercial portion as per above method in each project other than residential real estate project

C3 from 01- 04- 19 till completion.

The amount of final eligible common credit on commercial portion in the project

C4= C3 x carpet area of apartments not booked till OC/ Total commercial carpet area.

If C3> C4, then clam as credit in his return till Sept return.

If C3< C4, then reverse including interest from Apr till payment

Rule 43- Manner of Determination of Input Tax Credit in respect of Capital Goods and Reversal

Let us assume that,

T= Total credit on Capital Goods.

T1= Credit on goods used for non business purpose, which will not be credited in Electronic credit ledger(ECL).

T2= Taxable supplies including zero rated supplies - which will be credited in ECL.

In case of supply of services as per Sch- 2 para 5 clause b, ITC = 0

T3= T- T1- T2 (Common Credit) which will be credited in ECL

Tm = T3/60.

Tr= Aggregate of Tm of all the capital goods

Common credit relates to exempt goods (Te) = Tr x Exempt/ Total Turnover in the state.

** In case of supply of services as per Sch- 2 para 5 clause b,

Credit on Exempt supplies = C2 x E/F (E= Carpet area of Apartment {exempt from tax + not exempt from tax, but booked after OC}, F= Aggregate Carpet area).

Te shall be adjusted in every month and add in the output tax liability.

Te should be computed for each tax (CGST, SGST, IGST).

CAclubindia

CAclubindia