ESOP may be introduced by the companies as a tool to expand its capital base and issue further share capital to its employees. ESOP may also be used as a strategy for employees' recognition and reward.

Section - 62 (1) (b)

Employees' stock option may be allotted to employees by passing a Special Resolution by the company (Ordinary resolution in case of private company) and subject to such conditions as may be prescribed under the relevant rules.

Rule 12: Conditions prescribed for the Issue of ESOP.

(1) ESOP has been approved by passing a special resolution.

Note: Rules do not specify exemption for private companies from passing special resolution. However, provisions of Section 62 (1) (b) prescribe so. Since provisions of the Act has overriding effect over rules, the provisions of Section 62(1)(b) shall be followed. Hence, passing of resolution by simple majority (i.e. Ordinary Resolution) shall be sufficient for approving ESOP scheme in a private limited company.

Meaning of Employee:

a. a permanent employee

b. a director whether whole-time director or not but excluding independent director

c. employee as defined in a and b, of a subsidiary company in or outside India, or of a holding company

But does not include:

a. a promoter

b. person belonging to promoter group

c. director holding more than 10% of equity shares (individually or through any relative/body corporate)

This exclusion shall not apply to start up companies as defined by DIPP via notification no. GSR 180(E) dated 17th Feb, 2016 upto 5 years from the date of its incorporation.

(2) Disclosure in explanatory statement to the notice for calling of general meeting.

a. Total no. of stock options to be granted.

b. Identification of employees entitled to participate in the scheme.

c. Appraisal Process

d. The requirement of vesting and period of vesting

e. Maximum period within which the options shall be vested

f. Exercise price or formula for arriving at the same.

g. Exercise period and process of exercise

h. Lock-in period, if any

i. Maximum no. of options to be granted per employee and in aggregate

j. Method of valuation of options.

k. Conditions on which options may be lapsed.

l. Time period for exercise of options in case of termination/resignation of employee.

m. Statement of compliance with the applicable accounting standards

(3) The company shall be free to determine exercise price in conformity with the applicable accounting standards.

(4) Separate resolution is required to be passed in case of-

a. Grant of options to employees of subsidiary or holding company.

b. Grant of options to identified employees > or = 1% of issued capital of the company at the time of grant of options (excluding outstanding warrants/conversions.)

(5) (a) The company may vary the terms of scheme not exercised yet by the employees by passing special resolution provided such variation is not prejudicial to the interest of option holders.

(b) Notice of passing of special resolution of such variation shall disclose full variation, rational thereof, details of beneficial employees.

(6) (a) Minimum period of 1 year between grant of option and vesting of option.

In case of merger, the said period shall be adjusted against the period during which the options were held by the employees in merging company.

(b) The company may provide for any lock-in period for shares issued pursuant to scheme of ESOP.

(c) The employee shall not have any right of dividend, right to vote or any other shareholder right until issue of shares on exercise of such options.

(7) Any advance amount given by the employees at the time of grant of options

(a) may be forfeited, if option is not exercised with the exercise period,

(b) may be refunded, if options are not vested due to non-fulfillment of conditions of vesting of options.

(8) (a) The options granted shall not be transferrable.

(b) The options granted shall not be pledged, hypothecated, mortgaged or otherwise encumbered.

(c) Subject to (d), no other person than the employee shall be entitled to exercise the option.

(d) In the event of death, all the granted option till date shall vest in the legal heir/nominee of the deceased employee.

(e) In case of permanent incapacitation, all the options granted to him till the day of such incapacitation, shall vest in him on that date.

(f) In the event of termination/resignation, options which are not vested in him shall expire.

However, vested options may be exercised by the employee as per terms of the scheme.

(9) Disclosure in Directors' Report:

(a) options granted;

(b) options vested;

(c) options exercised;

(d) the total number of shares arising as a result of exercise of option;

(e) options lapsed;

(f) the exercise price;

(g) variation of terms of options;

(h) money realized by exercise of options;

(i) total number of options in force;

(j) employee wise details of options granted to:-

(i) key managerial personnel;

(ii) any other employee who receives a grant of options in any one year of option amounting to five percent or more of options granted during that year.

(iii) identified employees who were granted option, during any one year, equal to or exceeding one percent of the issued capital (excluding outstanding warrants and conversions) of the company at the time of grant;

(10) The company shall maintain a Register of ESOP in SH-6 at the registered office of the company and shall be authenticated by company secretary of the company or any other officer authorized in this behalf.

(11) If company is listed, SEBI Regulations on the ESOP has to be complied with.

METHODS FOR IMPLEMENTING ESOP

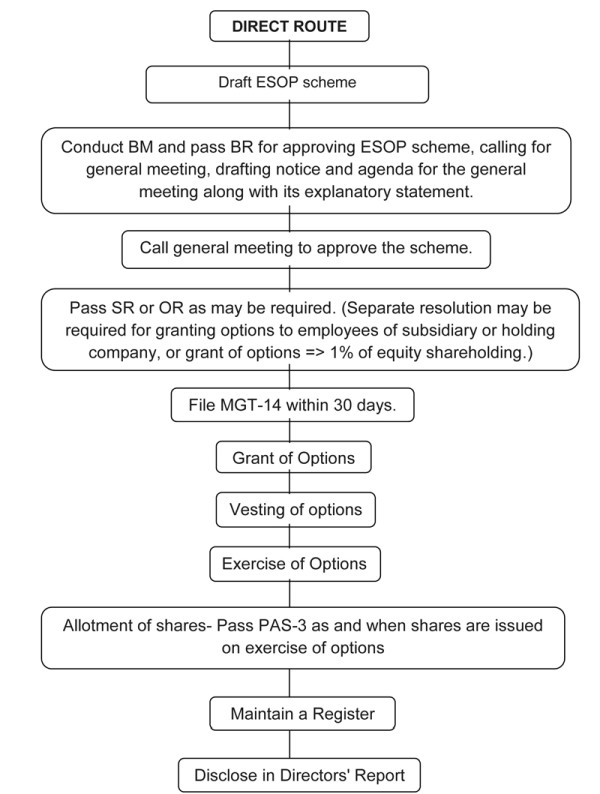

ESOP Though Direct Route:

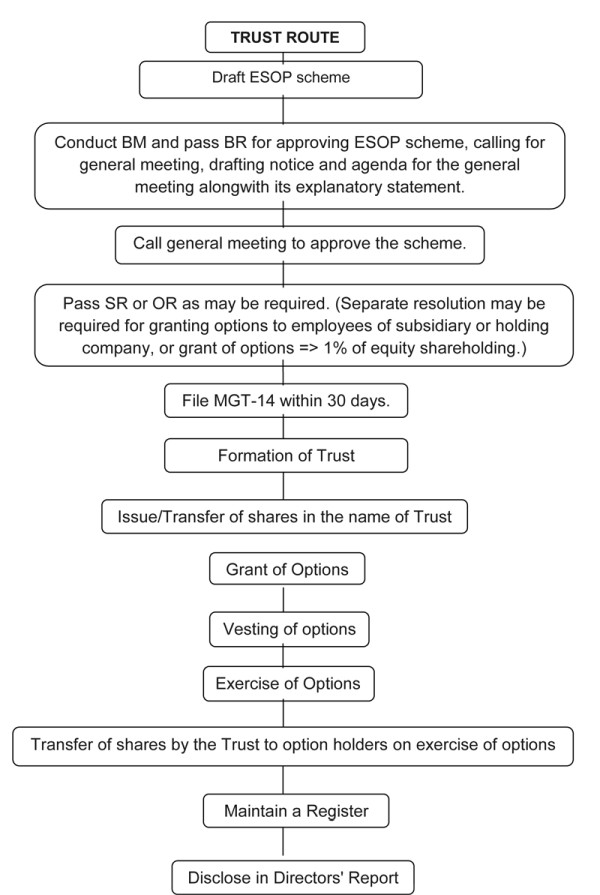

ESOP Through Trust Route:

Trust Route is the second method of issuing shares pursuant to an ESOP scheme. In this method, a Trust is specifically created and registered for the purpose of implementing ESOP Plan. A company drafts a scheme and gets it approved from the members of the company. Simultaneously, a Trust is formed and registered to act as an intermediary between the company and employees. As and when options are exercised by the option holders, Trust is responsible for issuing shares to employees.

In this structure, trust is formed and funded by the company itself. The capital of the trust and further funding requirements are fulfilled by the company by way of loan. The funds are then utilized by the trust to acquire shares either by subscribing to the issue of shares by the co. or from the secondary market. Generally, it is observed that shares are transferred by the promoters of the company.

Further, as and when options are exercised by the employees, shares are transferred to them in conformity of the ESOP Scheme.

IMPORTANT DEFINITIONS:

- Exercise Price: 'Exercise Price” means the price payable by the Optioneholder for exercising the Option granted to him/her under the ESOP Plan

- Exercise Period: Exercise Period means the period after vesting within which the Optioneholder should exercise his/her right to apply for the Shares against the Options vested in him/her in pursuance of the ESOP Plan.

- Option: Option means a stock option granted pursuant to the ESOP Plan, comprising of a right but not an obligation granted to an Employee under the ESOP Plan to apply for and be allotted shares of the company at a pre-determined Exercise Price.

- Grant of Option: Grant means issue of the Options to employees to purchase the shares of the company under the ESOP Plan.

- Vesting Period: Vesting period means the period elapsed between the date of Grant and the date of Vesting of the Option granted to the Employee

- Vesting of Options: Vesting means the process by which the Optioneholder is given the right to apply for shares of the company against the Options granted to him in pursuance of the ESOP Plan.

SIMPLIFIED PROCEDURE FOR ISSUING ESOP:

1. The very first step is to draft the ESOP scheme. Contents of scheme shall include:

- Objective of the plan

- Definitions of technical terms

- Determination of Exercise Price

- Identification of eligible employees

- Number of options to be granted

- Vesting Period

- Exercise Period

- Treatment in case of termination/resignation of employees etc.

2. Conduct Board Meeting for considering and approving scheme for further placing the same before members of the company in general meeting.

3. Conduct General Meeting and pass necessary resolutions.

4. File MGT-14 with ROC.

5. Issue grant letters for offering options to the identified employees stating details of the offer, requirement of vesting and further course of action in this regard.

6. Since there is statutory requirement of minimum gap of 1 year between grant and vesting of options, after completion of the vesting period, identified employees shall become eligible to apply for the exercise of options.

7. Subject to fulfillment of requirements of vesting, option holders may apply for issue of shares.

8. Thereafter, pursuant to ESOP scheme, shares shall be issued to option holders and respective returns shall be filed with ROC.

Note: In case of issue of ESOP through Trust Rout, Trust shall be formed and become functions simultaneously with the ESOP Scheme.

The author can also be reached at harnotiapriyanka@gmail.com

DISCLAIMER: THE ENTIRE CONTENTS OF THIS DOCUMENT HAVE BEEN PREPARED ON THE BASIS OF RELEVANT PROVISIONS. THE INFORMATION STATED ABOVE IS NOT A PROFESSIONAL ADVICE OR LEGAL OPINION. IN NO EVENT I SHALL BE LIABLE FOR ANY DIRECT, INDIRECT, SPECIAL OR INCIDENTAL DAMAGE RESULTING FROM THE USE OF THE INFORMATION.

CAclubindia

CAclubindia