The investment climate has dried up in many parts of the global economy. The slowdown in the European economy has placed brakes of long term on the investments capital. Chinese economy is placing more cautious steps to control the flow of investments capital. In other words their previous stimulus package has already created unmanageable asset bubble which is being keenly awaited to burst. Indian economy got hanged itself with its traditional rope of delay in reform policies. We have made a habit now about making delayed in execution of every activity. This might be one of the reasons behind why Indian economy is still being acclaimed as an emerging economy and not a developed economy.

Widening CAD followed with a significant drop in savings rate has created a two problem for the Indian economic growth. Drop in savings rate results to an alarm of increasing savings which further creates a problem of significant drop in consumption due to skepticism in economic prospect of India. As more than half of the population is dependent on salaried income, much of the skepticism exists among these people.

FDI investment has slowed down compared to the previous financial years. Well delayed project execution, increasing cost of projects, delay in regulatory approvals has expunged the investment cycle of India. India’s share of global FDI fell to 2.1% in 2011 from the peak of 3.0% in 2009.

Which Sectors Are Seeing Slowdown in FDI?

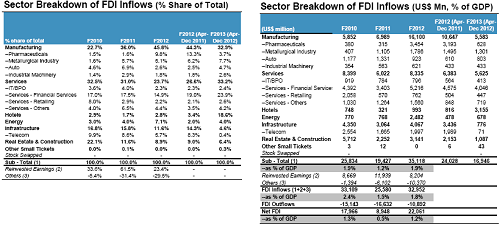

The decline in FDI has taken place across all the key sectors in the economy including manufacturing, real estate & construction, and services. Inflows into the services sector have declined by 12% YTD F2013 (Apr to Dec-12).

In the service sector we find that overall FDI has declined from its peak in F2007, it remains a considerable contributor to overall FDI flows, accounting for 25% of total inflows.

Investment in Information Technology and BPO (declined by 27% YoY) and financial services (declined by 14%YoY), contributing much of the decline of investments in service sector.

FDI flows to the manufacturing sector have fallen 48%YoY YTD. In particular, FDI inflows into the pharmaceutical sector have plunged 80% YoY so far in F2013.

Sub-segments such as automobiles continue to attract manufacturing investment, while FDI inflows into metallurgical industries and industrial machinery have posted YoY declines YTD.

One of the most interesting parts to accentuate is that a FDI investment has surged in two industries which were found to be viable for investments by domestic investments. FDI inflows to hotels have surged 286% YoY in F2013 while FDI flows to the energy sector have increased by 42%YoY YTD.

The biggest fear of mine is that we are focusing too much on domestic or non FDI investments to spur up. Reliance on non-FDI capital flows to fund the current account deficit is exposing it to potential funding risks whenever there is even a short period of risk aversion in global financial markets. Over the past three years, out of total capital inflows of US$181 billion, about 70% have been non-FDI. Hence in one word it can be said that we have already exhausted the non FDI capital and now in order to climb down from the rising CAD we need FDI. Since India is currently entering into the phase of funding risk.

Among these challenging domestic macro environment, India had been slipping in the rankings in the World Economic Forum Global Competitiveness Index. In 2012-13, India is ranked in 59th position, down 10 notches from its position in 2009-10. Similarly, India is ranked poorly as a place of doing business, coming in 132nd (out of 185 economies ranked) in the World Bank’s 2013 “Doing Business” report. This suggests that the business environment in India has become less competitive and India has become less attractive as an investment destination.

In my research I find that the slowdown phase and drop in consumption demand is going to increasing since political uncertainty followed with 2014 elections creates a atmosphere of skepticism which further granulates into pull back in the compensation and job prospects of the salaried class of employees.

The propaganda of drop in savings rate is an alarm to increase the same and drop the consumption demand which was acting as an catalyst to save the Indian economy from a bigger plunge.

Indraneel Sen Gupta.

Master in Economics/MBA in International Business/ICAI(Final)

CAclubindia

CAclubindia