INTRODUCTION:

In this topic our main target is to explore the investment in subsidiary. How we will do it?

- First we have to find out the net asset of subsidiary company on the date of acquisition.

- For this purpose we make Analysis of Profit (AOP).

Analysis of Profit (AOP)

- It is divided into 2 parts- Pre acquisition profit & post acquisition profit.

- If opening balance of P&L is missing then as per convention we assume that it was zero at the beginning and entire profit earned during the current year. Further if opening balance of any reserve is missing then we assume that it was same at the beginning too.

- Pre acquisition part after time adjustment shows the net asset on the date of acquisition.

- Post acquisition part after time adjustment shows the profits earned by subsidiary company after the date of acquisition.

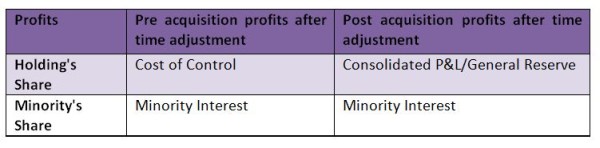

- Now we calculate Holding company’s share and minority’s share in the aforesaid pre/post acquisition profits.

Transfer of such shares:

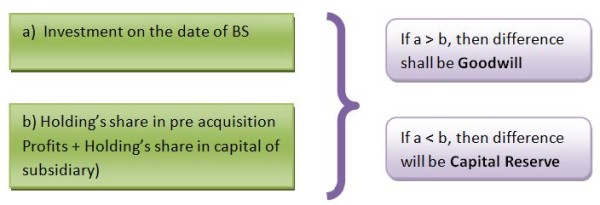

In this practice only profits are found on the date of acquisition but as we know net asset includes profits plus capital. So we have to calculate Holding and Minority’ share in the capital of subsidiary on the date of acquisition. Holding’s share shall be transferred to Cost of Control and Minority’s share shall be transferred to Minority Interest. Now comparison shall be as follows:

We have to make some adjustment in working of AOP which were discussed below:

A. Treatment of Abnormal Loss/ Profit

- First we have to eliminate the effect of abnormality accordingly it will be added or deducted. The intuition behind this is that we follow the assumption while applying the time adjustment that profits are earned evenly during the F.Y. so we have to eliminate the effect of abnormality.

- Now apply time adjustment

- After time adjustment we have to create the effect of abnormality. Accordingly in the respective period after time adjustment. (Don’t forget this step)

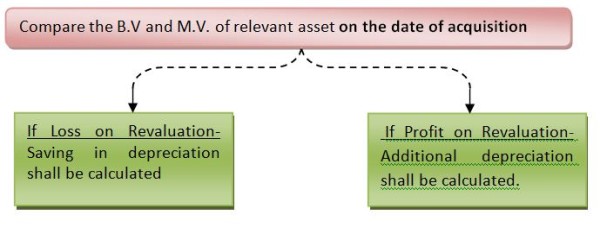

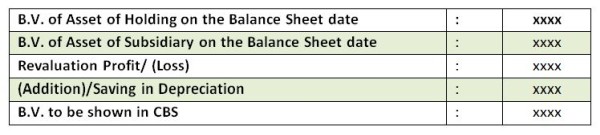

B. Treatment of Revaluation of Fixed Assets

Notes:

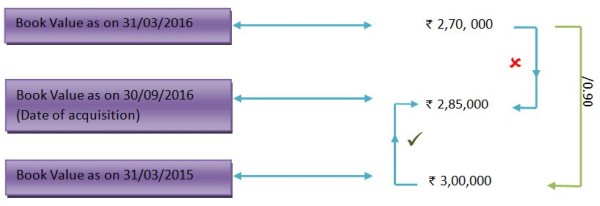

a) Calculation of B.V. on the date of acquisition: For this purpose we must calculate the B.V. at the beginning of the F.Y. retrospectively in which we acquired the shares after that we proportionately calculate depreciation up to the date of acquisition for getting B.V. on the date of acquisition. It means we can’t take a shortcut to get the book value from the Balance Sheet date to the date of acquisition. Example (assuming depreciation rate 10%).

b) Profit/Loss on revaluation shall always be adjusted in pre acquisition profits after time adjustment. (Because only Revaluation of Subsidiary company on the date of acquisition is relevant). Why after the time adjustment? - Because these are pre defined as pre acquisition.

- Additional/ saving in depreciation shall always be adjusted in post acquisition profits because such depreciation shall always be effective after the revaluation and as earlier it is said that the revaluation is used to be adjusted in pre acquisition profits.

- Both (Additional/saving in depreciation & Profit/Loss on revaluation) shall also be adjusted in CBS in following manner:

C. Treatment of Bonus

1. Reduce the Profits

- Always be from pre acquisition profit as per SEBI guidelines.(Unless the question specify)

- After time adjustment. (Because we are reducing bonus from pre acquisition profits so first we will have to calculate pre acquisition profits which can be get only after time adjustment).

- But if question says that subsidiary company has made any entry for Bonus then first we have to add it in the post acquisition profits before time adjustment.

2. Increase the share capital: It has 2 effects

- Shown in Cost of control (Holding’s share in bonus capital).

- Shown in Minority Interest (Minority’s share in bonus capital).

Notes:

- The receiver (i.e. Holding Co.) doesn’t make any entry because bonus effects only increase in shares not increase in investment amount.

- Since Bonus doesn’t make changes in Net asset (Because Increase in capital & decrease in reserve surplus with the same amount), still our institute wants us to adjust the bonus in question as we already know that for calculation on cost of control we use latest data. (It means that if we will ignore the bonus the cost of control shall be same when we take effect of bonus).

- Bonus can also make changes in the holding ratio. So while calculating holding ratio always add the bonus share in denominator (total shares before bonus) as well as in nominator (holding shares before bonus).

D. Treatment of Dividend

1. On the Holding Company’s(Receiver) stand point of view:

If the dividend received from the profits which have been earned before our acquisition of shares then such dividend shall be credited in the investment account. The logic behind this is that for these profits I have already paid the cost and now when it is received by me it can’t be said my income as it is recovery of my investment vice versa.

Example: Mr. A purchased shares on 01/04/2011 and Mr. B purchased shares on 01/04/2013. The company paid dividend for F.Y.2011-12 on 31/03/2014.

In the above example Mr. A will credit the dividend received into P&L account because it is from post acquisition profits. And Mr. B will credit the dividend received into Investment account because it is from Pre acquisition profits for which he has already paid the cost while purchasing the shares.

In the questions we always assumed that the holding company’s accountant is mad and he always makes wrong entry for the dividend which has received from the pre acquisition profits unless clearly mentioned. So we have to rectify such mistake by passing a journal entry:

Note: Please note that pre acquisition dividend must be received by holding company unless don’t make the above entry. For this purpose only do one thing: compare date of distribution and date of acquisition.

Now question is how we will guess that the particular dividend is from pre acquisition or post acquisition profits? The answer is that when it comes to interim (the word itself says in the term) dividend it is always distributed in current year out of current year profits. It is always prorate it means for example interim dividend is distributed on 31/12/2016. This is for F.Y. 2016-17 and for 9 months. Now we have to see when we acquired the shares? Accordingly the 9 month’s dividend shall be distributed in pre or post.

On the other hand the final dividend (which belongs to last year) is paid in current year and always out of the previous year profits.

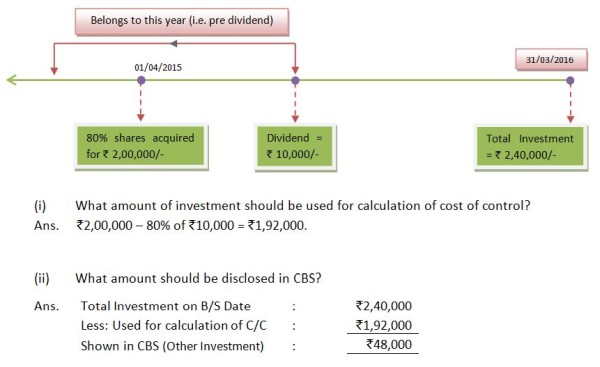

If pre dividend is correctly recorded by Holding company + Investment on B/S date includes other investments, then holding company’s share in pre dividend shall be reduced in the investment (which is given in the information part of the question not in the BS) while processing cost of capital. Example as below:

2. On the Subsidiary Company’s(Distributer) stand point of view :

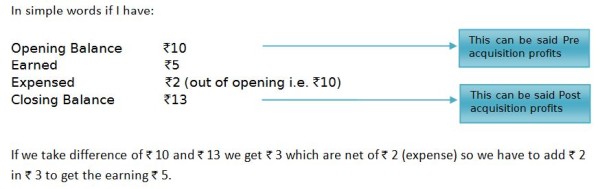

While processing AOP we calculate post acquisition profits (i.e. difference of pre acquisition profits and total profits), the figure which we get net is net of all transactions. It means while getting post acquisition profits dividend is already deducted in post acquisition profits so we have to add it back to make it Net profit/PAT because we well know that time adjustment is always used to applied on Net profit(evenly accrued during the year).

In other words the difference we get i.e. Post acquisition profit is net of all transaction. If we say there is 2 transactions i.e. credit balance of P&L and debit balance of dividend paid, we get credit balance of P&L net of dividend.

If we take difference of Rs.10 and Rs.13 we get Rs.3 which are net of Rs.2 (expense) so we have to add Rs.2 in Rs.3 to get the earning Rs.5.

Hence we can say subsidiary company doesn’t make mistake for dividend but while processing AOP the dividend mathematically deducted from the wrong place so we have to rectify it.

Some other issues to be noted in dividend and bonus:

- Final dividend is always being distributed on the capital’s closing balance of the last year.

- Interim dividend is always being distributed on the capital’s balance at the point of distribution.

- As we well known now that for considering the pre dividend or post dividend, the date of distribution is not important but even the source from which dividend is distributed is important.

- In case of bonus, 3 things to be carefully calculated:

- Its own adjustment (Discussed earlier)

- Holding ratio (Denominator and nominator both should be same i.e. with/ without bonus)

- Amount of dividend (In case the dividend is before the bonus always aware whether the balance of capital which we are using to calculate the dividend amount is including bonus or not). This issue will be only in case where the dividend is given in % term and we have to calculate the amount of dividend.

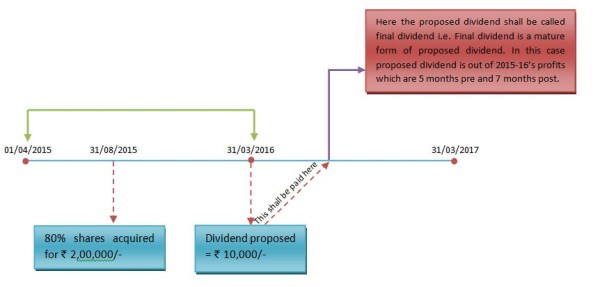

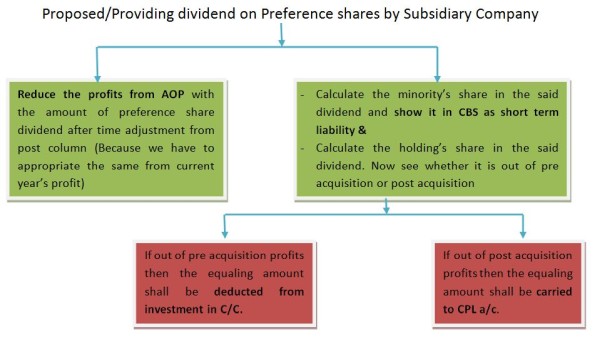

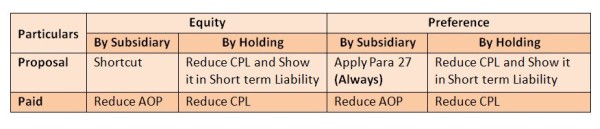

E. Treatment of Proposed dividend

- Proposed dividend is a growing form of final dividend. It means proposed dividend whenever is payable (As per companies Act within 30 days) it is called final dividend.

- Accordingly proposed dividend is always be appropriated out of the current year profits and for considering whether it is pre or post check the current year position.

- Now if the subsidiary company proposes equity dividend there will be no treatment except one journal entry with the amount equal to Minority’s share in proposed dividend:

Intuition behind this single entry: As we well know that for proposed dividend we have to reduce profits & create a short term provision for proposed dividend. But such short term liability is not 100% liability of subsidiary as a whole because we are consolidating the accounts. Hence holding’s share in proposed dividend can’t be said liability. Therefore we have to consider only minority’s share in proposed dividend and don’t deduct anything in AOP.

In case subsidiary company has already proposed dividend then we have to add it back in post acquisition profits before time adjustment to get PAT and then pass the above journal entry further we need not to do anything.

4. In another case if holding company proposes dividend than CPL shall be reduced and a short term liability of proposed dividend shall be created in CBS with the amount of proposed dividend as such dividend is 100% outsider liability.

Note:

- In case subsidiary company also have preference share capital then we shall always provide (as we know preference dividend is not proposed because its rate is fixed) the preference dividend for subsidiary company for the current year (which shall be paid next year) whether it is said in question or not. (As required by Para 27 of AS-21).

- Please note that the treatment of dividend paid of equity and preference share shall be same as discussed earlier but proposal treatment is different.

- If subsidiary company has preference share capital and equity dividend is paid then it always assumed that preference dividend would have also been paid and accordingly it shall be adjusted.

Summary of Dividend Adjustment:

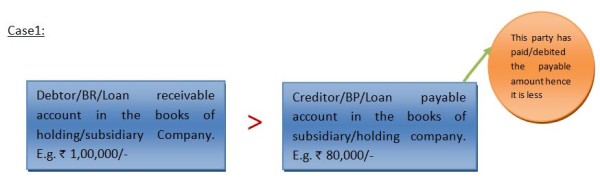

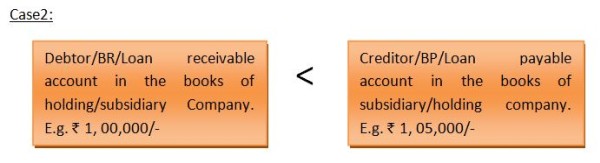

F.Treatment of Intra group transactions

It means that one party or account is standing in both books i.e. in the books of holding company as well as in the books of subsidiary company. Now there may be only 2 cases:

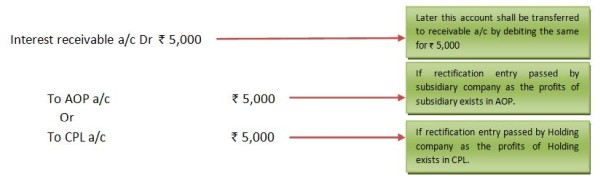

It shows that someone is claiming that I have to receive more than someone’s payable. This is possible where, the party (whose liability to pay) has remit the amount by cheque/cash but the receivable party has not received yet. So we have to pass the following adjustment entry:

This can be possible only in case of error. For example Subsidiary/Holding Company has forgotten to pass the entry of interest receivable hence the balance in receivable account is less than payable account. Now we have to pass the rectification (here it is omission) entry as below:

The effect of the above entry shall be that the receivable account shall become equal to payable account now we can eliminate both contra accounts by passing the entry below:

Note: In case rectification entry is passed by subsidiary company than we well known that it should carried to AOP. Now the question is where in AOP? The answer is:

Case 3:

Investment in debentures by Holding company in Subsidiary is also treated as Intra Company debt /receivables. But if such investment has been purchased less than or more than the face value then such profit/ loss shall be accordingly adjusted.

Example: H Ltd having investment in 10% debenture (100 No’s & Face Value 100/-) for ` 9,800/- in S ltd. and S Ltd showing Liability of Rs.10,000/-.

Here H Ltd shall show profit of Rs.200/- in its CPL and contra shall be with amount to the tune of Rs.9,800/- in the books of H ltd and Rs.10,000 in the books of S Ltd.

Intuition behind this is that H ltd shall get the amount of Rs.10,000/- on redemption investing Rs.9,800/- so Rs.200/- should be the income of H ltd.

On the stand point of Subsidiary Company the profit/Loss shall be shown in AOP according to the date of acquisition of debenture (Because as we invest in debenture at that movement we have earned the profit/Loss) after time adjustment (because we have to increase the C.Y. profit) in post column.

G. Treatment of intra group Bills and their contingent liability

1. Intra Group Bills: Contra shall be by the bills which are still held by the receivable party. It means the bills remains after deducting the bills which are discounted, are subject to contra/eliminated.

Example: Holding company has B/R amount Rs.10,000/- out of Rs.4,000/- belongs to Subsidiary company. It means subsidiary company has B/P Rs.4,000/-. Now if holding company discounts or endorsed the bill amount to Rs.1,500/- the remaining bills Rs.2,500/- (Rs.4,000 - Rs.1,500) are subject to contra i.e. these are the bills still held in the group.

Note: The word “held” itself says that we have to focus only the party who has bills receivables because this party is the receiver of the bills and possess right to discount the bills.

2. Intra Group Contingent liability: The contingent liability which is within the group shall be eliminated/contra. In my above example the discounted bills of ` 1,500/- is contingent liability which also relates to group shall be eliminated/Contra.

H. Treatment of intra group sales of assets

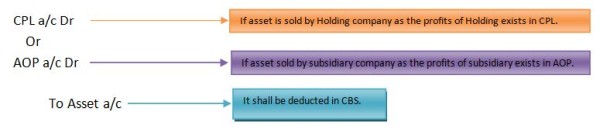

1. We have to reduce the profit portion from the asset transferred which still held by the group party may be Holding Company or Subsidiary Company.

2. The profit on such asset shall be reduced from the profits of whom party who have earned it. For example if holding sales asset to subsidiary company it means Holding company has earned profits hence the profits of holding company shall be reduced in CPL and vice versa.

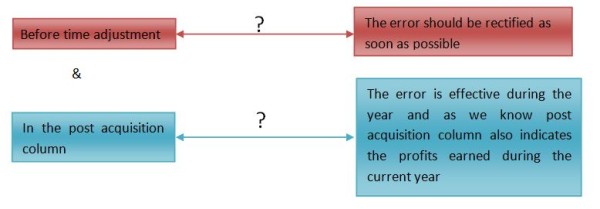

3. If the profits of subsidiary company is to be reduced (opposite of above case) then profits shall be reduced from AOP. Now the question arises where from AOP? The answer is according to date of transaction after the time adjustment i.e. if transaction falls in pre period the pre acquisition profits shall be reduced and vice versa. But in lack of information we assume that it is from Post acquisition as the intuition is that the stock is transferred to group relates to earliest period i.e. current period.

4. The relevant entry with the portion of profit is as below:

5. Amount of adjustment (As discussed earlier): Amount of profit on such asset which still held with the group party. It is called UP (Unrealized Profits)

Example: Holding company sold goods to its subsidiary company for ` 10,000/- and made profit on cost @25%. Now 60% stock is still held by subsidiary. Comment

The stock (From CBS) and profit (From CPL as earned by holding company) shall be reduced byRs.1200/- i.e. 25/125 of 60% of Rs.10,000/-.

6.If asset are sold in groups on the credit basis then the contra shall be done only if question clearly says because it is not a genuine approach to assume that if the stock is held with group party then there must be inter group debtor/creditor. Hence we always assume inter group sales are only made in cash not on credit basis.

7. Only the balance of unrealized profit (i.e. Net of depreciation) on assets should be eliminated.

Example: At the Beginning of the year H Ltd sold an asset to S ltd for Rs.10000/- earning a profit of 25% on Cost. S Ltd charged depreciation on it @10% p.a. What will be the amount of U.P to be elemineted?

Here the amount of UP = (10000*25/125) – 10% of (10000*25/125) = Rs.1800/- . Intuition behind this is that we would have been eliminated the profit of Rs.2000/- but out of this profit Rs.200 has already been eliminated as depreciation so the balance amount of Rs.1800 shall be eliminated.

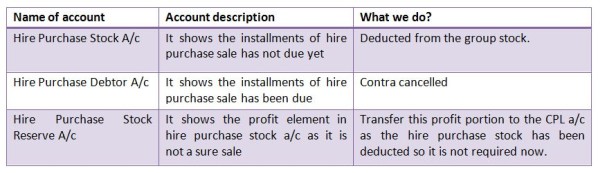

I. Hire purchase effect elimination :

When any asset is sold by holding to subsidiary on hire purchase basis then the holding company shall make the below entry:

Now whenever the right of recovery shall be established (i.e. the instalment shall be due) the holding company shall pass the below entry:

So the entire stuff to be done in the question is shown in the table below:

Now we well know that the debtor on the hire purchase sale is divided into two parts one is HP debtor and the other is HP Stock. On the other hand it is an asset for the purchaser which also includes the profit element. So at last we have to also deduct the profit element from the group fixed asset.

Now for the calculation of profit element the % of profit will be same as the stock reserve was % of HP Stock (i.e. Installment not due).

Note: If the question doesn’t say clearly that for how many ` the fixed asset is sold on hire purchase basis then the purchase price shall be assumed total of HP Debtor and HP stock and thereafter the profit shall be calculated accordingly.

DIFFERENT SITUATION UNDER CONSOLIDATION:

A. Multiple Acquisition

When shares of subsidiary company are acquired by holding company on different dates. Points to be considered:

- Solve it like different questions and make AOP for each acquisition.

- Calculate M.I. (With final %) in the last AOP.

- While rectifying pre dividend in C/C, % of dividend shall be taken according to % of shares acquired on different date

Example: 30% acquisition on 01/04/2015 & this AOP holding pre dividend of Rs.20,000/-. And 40% acquisition on 30/06/2016 & this AOP holding pre dividend of Rs.15,000/-.So dividend rectification in C/C:(30% of Rs.20,000 + 40% of Rs.15,000) = Rs.12,000/-

4. Other adjustment shall be same in the respective AOP.

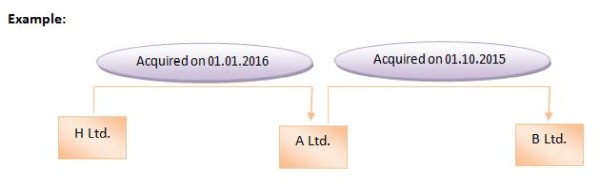

B. Chain Holding

Where a Holding company having more than one subsidiary or subsidiary having its subsidiary too.

Points to be considered:

- Start the solution with the smallest subsidiary and its previous holding.

- Make AOP of all subsidiaries.

- Carry the post acquisition profits of subsidiary to the Holding’s AOP (Which is also a subsidiary of another i.e. profits from B ltd’s AOP shall be transferred to A ltd’s AOP) after the time adjustment in Pre/Post column according to the date of acquisition.

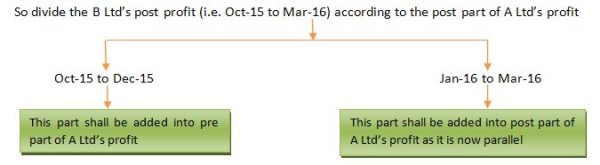

Example: In B Ltd’s AOP six months profits (Apr-15 to Sept-15) are pre and six months profits are post (Oct-15 to Mar-16). But in A Ltd’s AOP (Before transfer from B Ltd’s AOP) nine months profits (Apr-15 to Dec-15) are pre and three months profits are post (Jan-16 to Mar-16).

In this case we have to carry the B Ltd’s Post profits in the A Ltd’s AOP but post part of A Ltd is notparallel with post part of B Ltd.

4. Rectification of Pre Dividend: We know well reduce the CPL and reduce the investment. But some points to be considered:

- In case if B Ltd distributes dividend than A Ltd is receiver. Accordingly A Ltd shall rectify the pre dividend but A Ltd’s profit is not now the CPL but even it is A Ltd’s AOP. So A Ltd’s share in the dividend shall be reduced from the A Ltd’s AOP before the time adjustment (Because rectification shall be corrected as soon as possible) in post column (Because A Ltd has considered it as it’s C.Y.’s Income and we know post column indicates C.Y.’s profit so deduct from here).

- At last deduct its share from C/C.

5.Finally share of Later Holding ( Here it is H Ltd) in Final AOP’s (Here it is A Ltd’s AOP) pre column shall be carried to C/C and post column shall be carried to CPL.

6. Minority Interest of all AOP’s shall be clubbed.

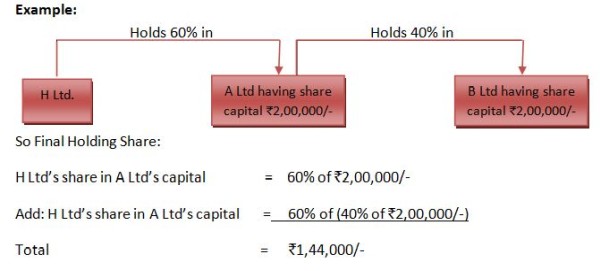

7. Share capital of all subsidiaries shall also be clubbed and divided into final holding’s share (As per example below) and minority share.

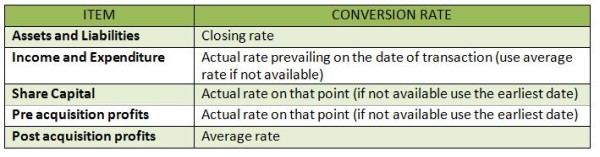

C. Foreign Subsidiary

- Prepare the AOP in foreign currency as usual. Since the dividing in the last (i.e. pre acquisition profit and post acquisition profit) is generally equal to P&L balance of subsidiary company as given in balance sheet and finally it can be treated as balance sheet item and converted accordingly.

- Convert the foreign currency Balance sheet in to ` Balance sheet. Use the conversion rate as per the following chart:

Since we are using different rates for conversion, the difference should be taken into FCTR (Foreign currency transaction reserve). Such reserve will also be considered while calculating minority interest and cost of capital.

D. Treatment of Joint Venture(JCE)

- Only JCE (Jointly controlled entity) which is formed as an entity is subject to consolidate as per AS-27.

- For being a joint venture there is not any requirement of minimum % of holding only it is required to be evidenced by contractual agreement. But if we hold more that 50% of shares then it will be treated as subsidiary unless the question is silent.

- This entity is consolidate with parent to the extent of own share (i.e. minority interest is not calculated). It is called proportionate consolidation method.

- Contra and UP adjustment also should be pro rata part only.

- Now question arises that how my balance sheet will be matched even I didn’t take M.I. in AOP? The answer is that we have left the minority’s portion in the entire balance sheet items so it will obviously matched.

E. Treatment of Joint Venture(JCO/JCA)

- In case of JCO and JCA, separate entity is not formed.

- In these case Asset, Income, Expenses and Liabilities are shown in separate financial statement as share in J.V. So the only question can be of that how the transactions are to be journalized. Only one Example will not be sufficient to elaborate how we journalize such type of transaction but the example showing below will help to understand:

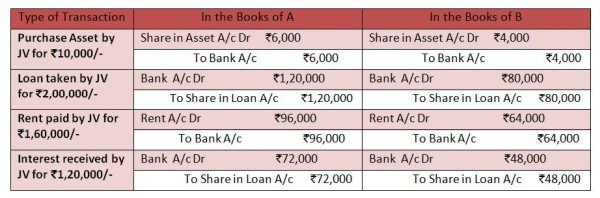

Example: Assume A and B are entered into joint venture of JCO entity in ratio of 60% and 40% respectively so the journal entry shall be as below:

3. If Joint Ventures entered into the transactions internally then it is important to think the transactions on the stand point of view of Joint Ventures (Combined). Assuming the same situation as explained in the above example if

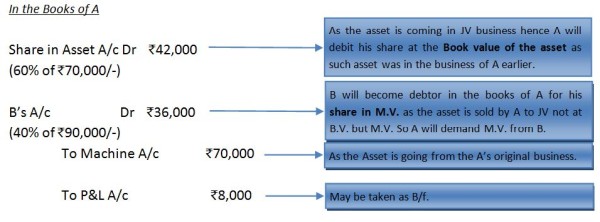

Case-1 A sold any Asset to the JV (JCO) for Rs.90,000 having Book value Rs.70,000/- on credit. The journal entry shall be:

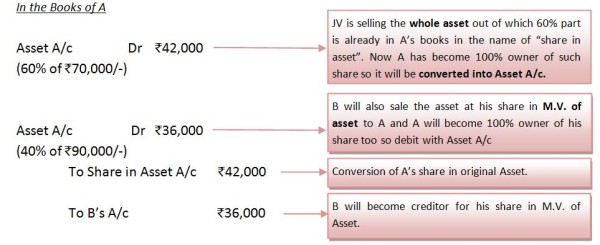

Case-2 A purchased any Asset from the JV (JCO) for Rs.90,000 having Book value Rs.70,000/- on credit. The journal entry shall be:

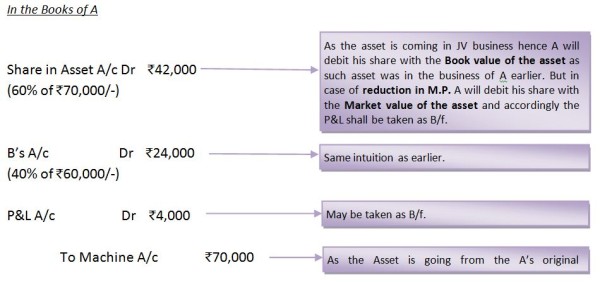

Case-3 A sold any Asset to the JV (JCO) for Rs.60,000 having Book value Rs.70,000/- on credit. The journal entry shall be assuming there is no reduction in Market price:

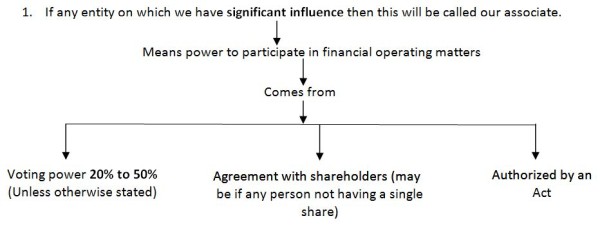

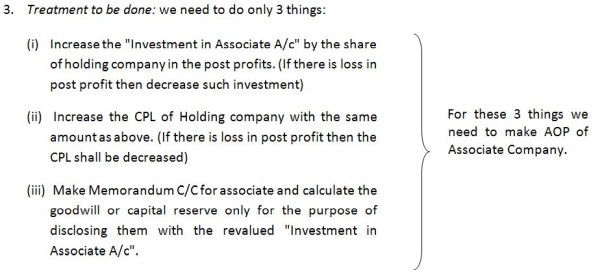

F. Treatment of Associate

4. While revaluing the “Investment in Associate A/c” if pre dividend is received from the associate company ensure the correct treatment of such pre dividend in the books of holding company. And as we well know that in the lack of information it is assumed that treatment of pre dividend is always used to be wrong in the books of holding so we need to deduct the share of holding company in pre dividend from the “Investment in Associate A/c” for getting the correct book value of the aforesaid investment account for the revaluation purpose.

5. Contra and U.P. shall also be pro rata through “Investment in Associate A/c”.

Example-1 Debtors of Parent Rs.10,000/- are due from associate and Investment in Associate is 25%. How it will be the adjustment?

Answer: For the purpose of contra we well know that we have to reduce both i.e. debtor from the books of parent and creditor from the books of associate to the tune of Rs.2,500/-. Here the creditors which are of parent company is already deducted from the aforesaid Investment account (which is Net asset of Associate on the date of acquisition +/- Goodwill/ Capital Reserve) to the tune of Rs.2,500/-.So for reducing the creditors increase the “Investment in Associate A/c” and decrease the debtor.

Example-2 H Ltd sold goods costing Rs.10,000/- to A Ltd (Associate company for 30% holding) for Rs.12,000/- and 60% goods have been sold by the A Ltd in the market. How it will be the adjustment?

Answer: Here the U.P. will be Rs.120/- [(30% of 60% of (Rs.12,000 - Rs.10,000)/-]. As the profit is made by H Ltd. so we have to reduce the profit of H Ltd i.e. CPL and reduce the stock (only profit portion) of A Ltd. from the “Investment in Associate A/c” (Since the stock is included in such account).

6. If associate company proposed the dividend and accounted for, then it is not required to be adjusted because we apply the shortcut for proposal of equity dividend (i.e. deduct from M.I. and shown into S/T provision amounted to the Minority’s share in such proposed dividend).

Since in the associate we don’t calculate M.I. there is no requirement of treatment of proposed dividend. However if we adjust it there will be no change in the answer. The reason is that such proposed dividend shall reduce the share of holding in the post profits of the associate which is to be added in the “Investment in Associate A/c” for the purpose of revaluation. Accordingly the “Investment in Associate A/c” shall be reduced (i.e. Net asset of Associate on the date of acquisition +/- Goodwill/ Capital Reserve).

If we think logically then we will found that there is also a share of holding in such proposed dividend which is like a receivable. So the share of holding in proposed dividend shall be added to “Investment in Associate A/c” and accordingly it will match from the earlier solution.

But in case the question covers associate and subsidiary simultaneously, we will have to adjust it because now the M.I. shall be calculated.

Finally the points to be noted regarding Joint ventures, Associates and subsidiaries are:

- If we have only power to compose the governing body of any company then it will also be called our subsidiary subject to the fact we have zero investment in such company. Since we have 0% shares in such company so the whole capital and profit & loss shall be transferred to the Minority Interest and rest Balance sheet of subsidiary shall be clubbed item to item with holding company.

- If any subsidiary in which the intention of investment was only for short term purpose, will not be called our subsidiary and not to be consolidated. Here the point to be noted that don’t forget to take the investment in such subsidiary in CBS.

- How to guess the nature of entity: It is necessary it read the question if there is clearly stated. In case where lack of information we take suitable assumption which is discussed by an example showing below:

Note: Further it is required to be clearly mentioned in the question whether the entity is Joint Venture.

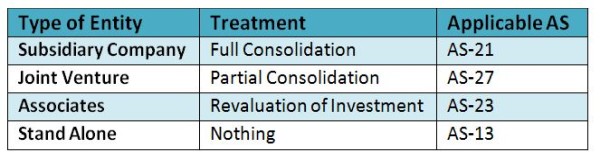

d. Treatment of various entities at a glance:

e. As we well know that for the purpose of saving time the C/C of a subsidiary and Joint venture can be prepared combined in case treatment of goodwill of each entity is not different. But read the question carefully as there may be given like the goodwill of subsidiary is to be write off and goodwill of subsidiary is to be kept unchanged, in such case we have make both C/C separately.

CAclubindia

CAclubindia